Lecture 1

Characteristics of FX Markets:

- Largest of all financial markets with average daily

turnover of over $8.5 Trillion! Spot transactions - $2

trillion; FX swaps dominate.

- short term instrument, buy and within a week period

- Banks use for liquidity

- 64% of all foreign exchange transactions involves cross-

border counterparties

- counterparty, or pushed-out risk

- Only 6% of daily spot transactions involve non-financial customers.

- US dollar involved in one-side of 85% of all trades, a slight decline from the 2019 survey; Euro is at 31%.

- Australian $AUD is the 5th most heavily traded currency

- Loosely organised in two tiers: wholesale & retail

Characteristics of Wholesale markets

- Not an organized exchange

- No fixed opening hours, centralized clearing mechanism, standardized contracts, etc.

- No equivalent of a stock market or derivative market

- Extremely deep and liquid market

- trade sizes 200-500M

- Participants in the market:

- International banks

- 100-200 banks willing to buy/sell foreign currency in their own account

- Bank customers engaged in commercial and Investment transactions, BHP, QIC, e.g.

- Non-bank dealers

- FX brokers

- Central banks

- International banks

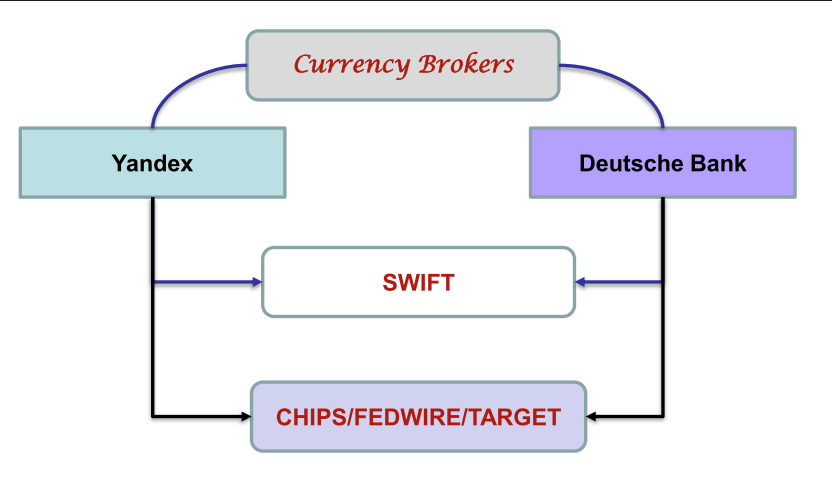

- Settlement of transactions – No real money changes hands

- The role of SWIFT

- Communication System

- Society of Worldwide International Financial Telecommunications

- Money often more through multiple banks before ending in the correct accounts

- chips, fedwire, target - organisations to transfer money

Exchange rate

-

A foreign exchange rate is the price of one currency expressed in terms of another currency.

-

A foreign exchange quotation (or quote) is a statement of willingness to buy or sell at an announced rate.

- Market makers - foreign currency dealers and brokers

- binding quotes for a few minutes

-

normally quote to four digits

-

normally settles T+2

-

have all the contributors at the bottom, with their bid/ask

Terminology

- Spot Rate: The exchange rate at which trades are executed immediately in the interbank market. About a third of all FX trading is done in this market.

- Value Date for a spot transaction is the date on which parties receive the funds they have purchased – e.g., in trades involving USD, settlement occurs two business days after the deal.

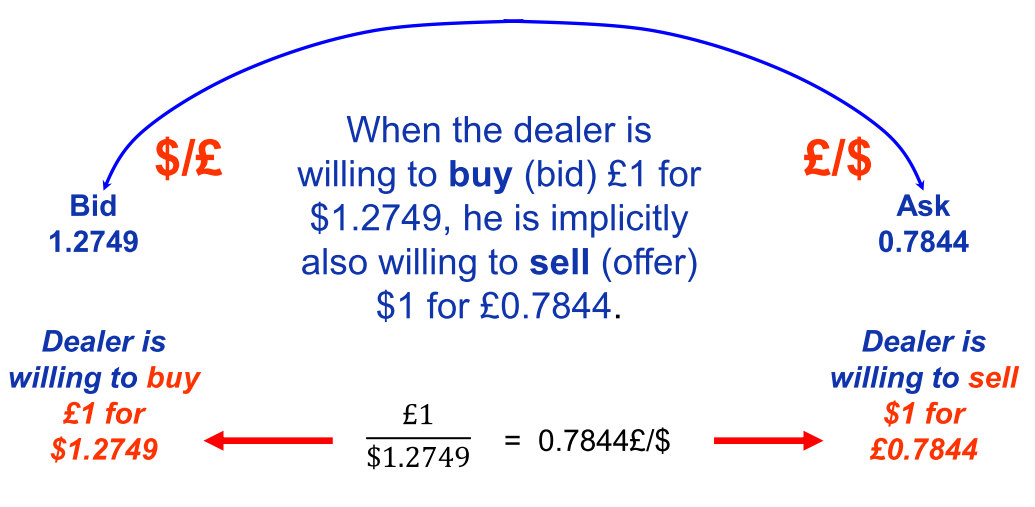

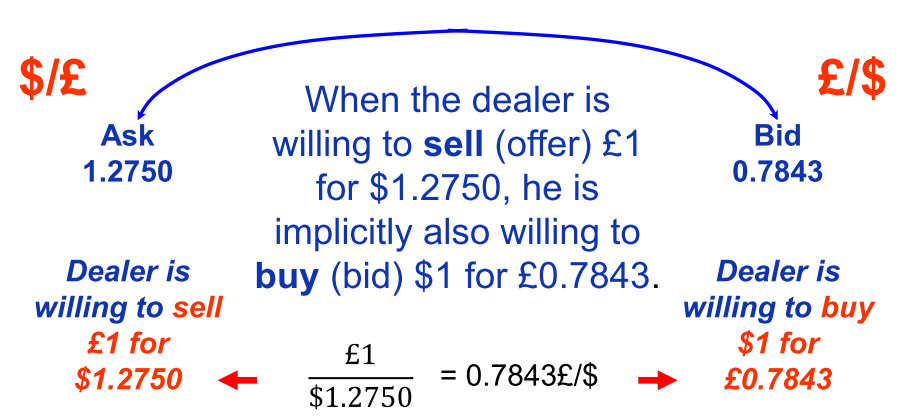

- Foreign currency dealers provide two quotes: - Bid Price: Price at which the dealer is willing to buy a currency from you (i.e., client) - Ask Price: Price at which the dealer is willing to sell a currency to you (i.e., client)

- It is always the case that the Ask Price > Bid Price. The difference is the Bid-Ask spread

- The less traded and more volatile a currency, the greater is the spread.

Bid/ask prices

USD - base currency CHF - Quote currency

- the rate at which the bank will buy USD (base currency) in exchange for CHF (gives customer swiss francs)

- the rate at which the bank will sell USD (base currency) for CHF (receives swiss francs from customer)

-

In the wholesale market, for a currency pair, there is a base currency (the first currency in the pair), and quote currency (the second). This is what Bloomberg uses.

-

Other quotations used in business include

- Direct Quote: Home currency per unit of foreign currency (FC)

- Indirect Quote: Foreign currency (FC) per unit of Home currency

- American & European terms are direct and indirect quotes relative to the US dollar (USD). The quote in the previous slide is in European terms.

-

Note that in all cases, the reciprocal of a direct quote is an indirect quote and vice-versa.

Example, AUDCHF

AUD - Base currency CHF - Quote currency If AUD is local currency, this would be an indirect quote

-

Cross-rate is an exchange rate that does NOT involve the USD

-

Explain the following quotes:

-

the amount of AUD the bank would buy from you in exchange for 1 CHF

-

the amount of AUD the bank would sell to you in exchange for 1 CHF

-

Bid and Ask prices mixed with alternative quotations methods can lead to confusion. Try to remember:

- The dealer buys the denominator (or base) currency at the BID [client buys the numerator (or quote) currency at the bid]

- The dealer sells the denominator (base) currency at the ASK [client sells the numerator (or quote) currency at the ask]

-

When all else fails, remember that the commercial client always, ALWAYS gets the worse end of the deal

Another Example

American terms (e.g. British Pound)

| Bid | Offer (ask) | |

|---|---|---|

| $/£ | 1.2749 | 1.2750 |

- Bid: Dealer buys £ for $ at the Bid, Client sells £ for $ (i.e., dealer will buy £1,000,000 for $1,274,900)

- Ask: Dealer sells £ for $ at the Ask, Client buys £ for $ (i.e., dealer will sell £1,000,000 for $1,275,000)

Inverse exchange rate

- a direct bid is the reciprocal of an indirect ask

- a direct ask is the reciprocal of an indirect bid

Bid-Ask spread

- The difference between the bid and ask prices is the bid-ask spread. It represents a “round-trip” transaction and is the cost of entering into the transaction.

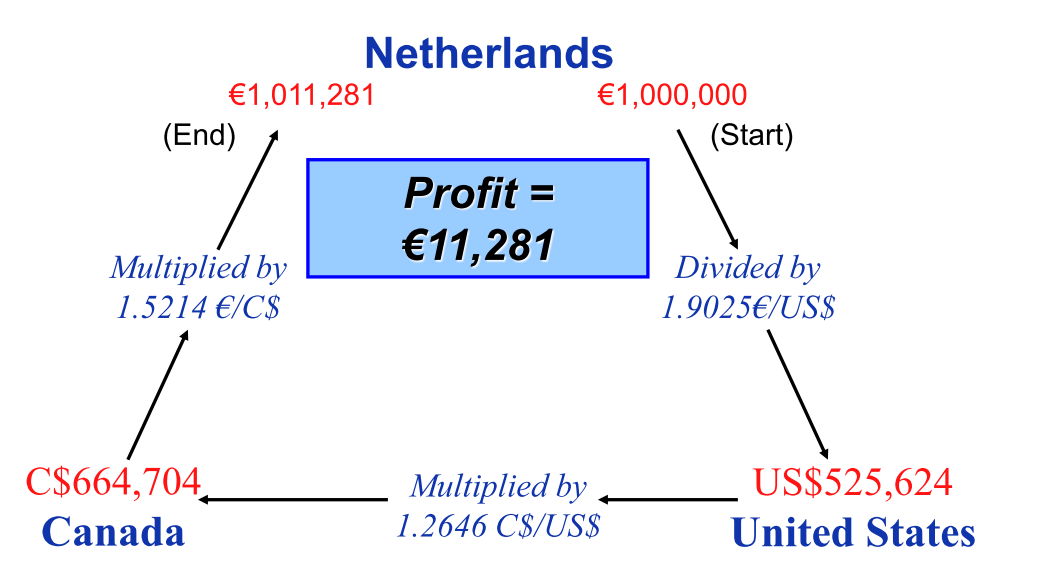

Triangular arbitrage

- Cross rates can be used to check on opportunities for intermarket arbitrage. Suppose the following exchange rates are available:

- The synthetic (manufactured) cross rate between Euros and Canadian dollars is:

Arbitrage example

Forward contracts

- Forward transactions require delivery at a future date of a specified amount of one currency for a specified amount of another currency.

- This is a rate that is agreed upon today but settled further into the future.

- Forward contracts are traded on the inter-bank market. They can be tailored for

- contract sizes

- currency

- delivery dates

Ways to quote forward rates

- There are three ways to express forward rates:

- Via points to be added or subtracted from spot rate [known as swap points]

- Outright quotes

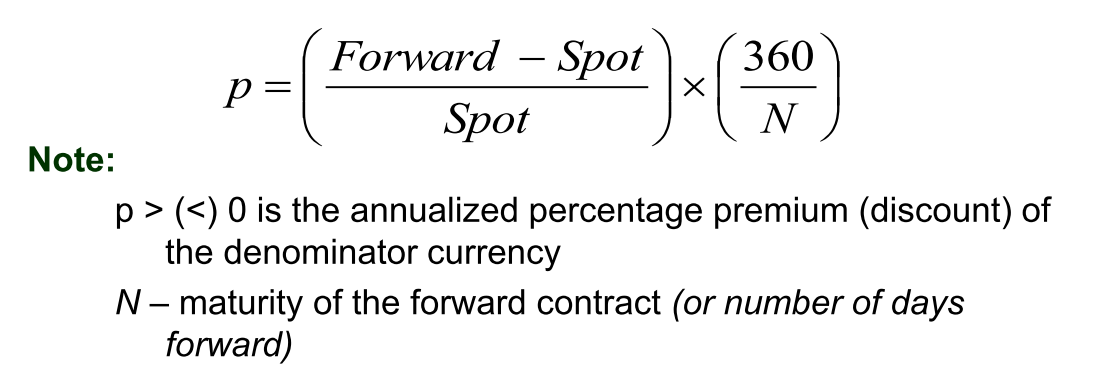

- As an annualized percentage forward premium or discount

Forward quotes: Swap rates

-

Among themselves, foreign exchange traders usually quote forward rates in terms of points, also referred to as “forward points” or “swap rates”

-

A point (pip) is the last digit of a quotation

- A point (pip) is equal to 0.0001 (1/100 th of 1%) for most currencies.

- The Japanese yen is the exception. It is quoted only to two decimal places; A point, in this case, is 1/100.

-

If F > S then the currency in the denominator (base currency) is trading at a premium

- E.g. One AUD buys more USD in the forward market than the in the spot market

- If ascending between bid/offer forward points then forward price will be higher than the current spot price

-

If F < S then the currency in the denominator (base currency) is trading at a discount*

- E.g. One AUD buys less USD in the forward market than the in the spot market

- If descending between bid/offer forward points then forward price will be lower than the current spot price

- If F = S then market is relatively flat

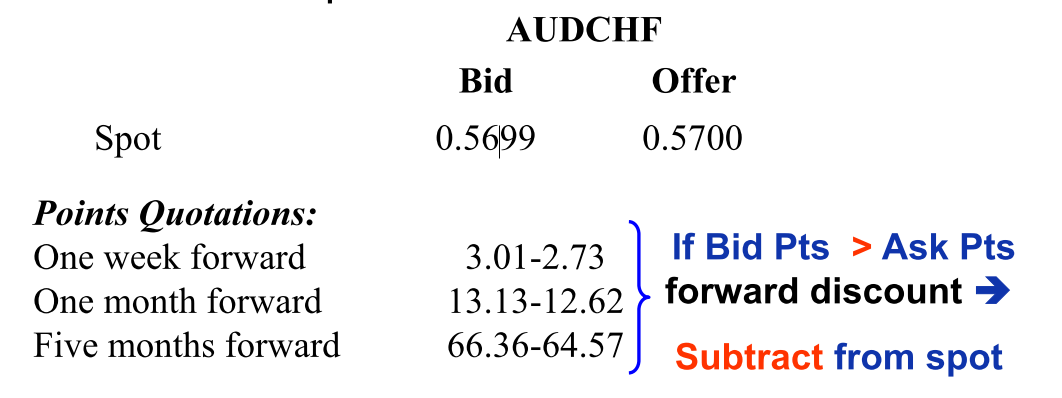

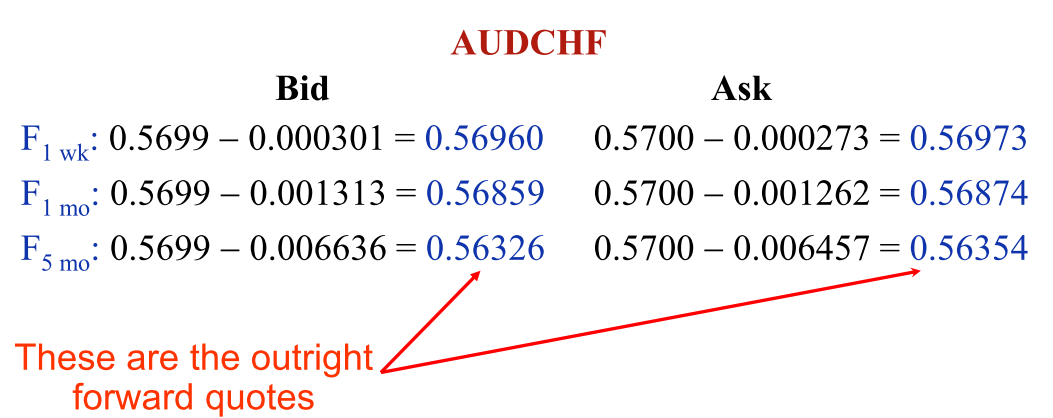

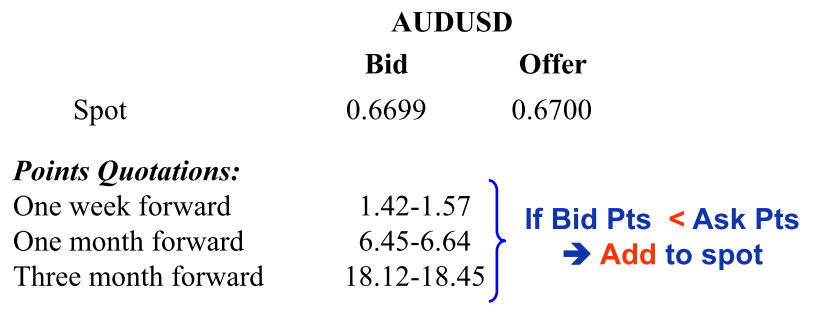

Swap rates

- A forward quotation expressed in points is not a foreign exchange rate as such.

- Rather, it is the difference between the forward rate and the spot rate.

When the Bid Points > Ask Points, you subtract the points from the spot rate to get the outright forward quote:

If the Bid Points < Ask Points, there is a forward premium, and you add the points to the spot rate to get the outright forward quote

Forward premium/Discount

- A forward premium exists when a currency purchases more of the second currency than it does previously

- This implies that the base currency appreciates

- A forward discount exists when a currency purchases less of the second currency than it does previously

- This implies that the base currency depreciates

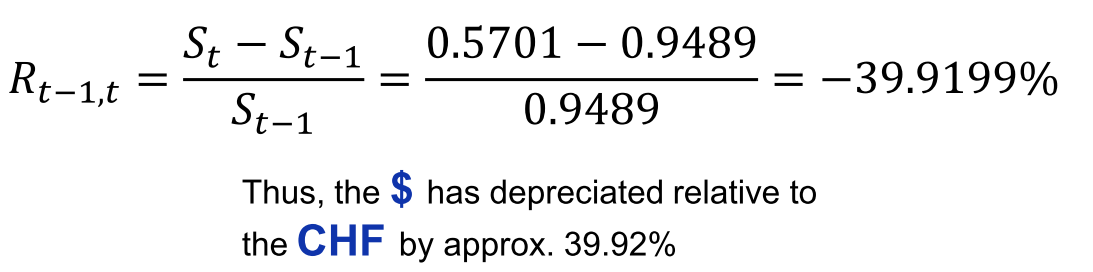

% change in exchange rates

The Australian dollar was quoted at CHF 0.9489/AUD in January 2013, while in January 2024, it was quoted at CHF 0.5701/AUD*

- At t-1 (Jan 2013): CHF 0.9489/AUD

- At t (Jan 2024): CHF 0.5701/AUD.

Thus, the appreciation/depreciation of the $, relative to the CHF from t-1 to t is: