Lecture 11: International Tax Issues

- The twin objectives/principles of taxation are:

- Tax neutrality

- Tax equity

- The different taxes MNCs pay

- Foreign Tax Credits

- Transfer Pricing

- Corporate Inversions

Sometimes the tax rules will allow you to take a credit in another country

International Taxation

- Ways in which profits of foreign entities of domestic (Australian) firms can be treated for tax purposes

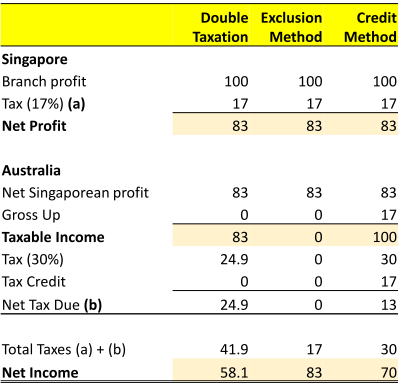

Australian country operating in other parts of the world (e.g. singapore)

- Double taxation:

- may pay both Singapore and Australian tax (41.9%)

- Exclusion (capital import neutrality) method says there should be no tax penalty competing with a Singaporean currency

- Exclude the foreign income from local taxes

- pay no additional taxes on that

Credit method

- Overall tax rate should be the same as if it was based in Australia

- What would be the taxes it pays

- Most you will pay is the tax rate in Australia

Tax Neutrality

- A tax scheme is tax neutral if it meets three criteria:

- Capital import neutrality (exclusion method): the tax burden on an MNC subsidiary should be the same regardless of where in the world the MNC in incorporated.

- Capital export neutrality (credit method): the tax scheme does not incentivize citizens to move their money abroad.

- National neutrality: taxable income is taxed in the same manner by the taxpayer’s national tax authorities regardless of where in the world it is earned.

Capital export neutrality:

Ensure the overall tax the country is paying is not above corporate tax rate in home currency

Don't want countries to act in such a way to move currency out of the country

Tax Equity

- Tax equity means that regardless of the country in which an MNC affiliate earns taxable income, the same tax rate and tax due date should apply.

- The principal of tax equity is difficult to apply; the organizational form of the MNC can affect the timing of the tax liability.

Nationality Principle

- Use the nationality to claim tax jursidiction

- US firms (regardless of where they earn their income) Have to pay tax locally

- E.g. Microsoft still has to pay U.S. tax

Types of Taxation

- (Corporate) Income tax

- An income tax is a direct tax, or a tax that is paid directly by the taxpayer upon whom it is levied.

- Withholding tax

- Tax on passive income like dividends, interest, royalties

- Tax treaty between Australia & US means, American investors are subject to 10% withholding tax on dividends they receive. This tax would be rebated as a tax credit in their home jurisdiction (i.e., the US).

- Value-added tax/Goods & Services Tax

- An indirect tax

Corporations pay corporate tax

Direct, one of the way countries raise revenue Withholding tax

Tax on passive income earning income on another country

Sometimes withholding taxes are waived if there are bilateral agreements between countries

- E.g. Tax treaty rebate between US and Aus

Value-added tax

- E.g. GST, imposed on values created at stages of production

- indirect tax, not on direct income

- transfer tax, buy/sell shares

- death taxes, wealth taxes, inheritance tax

Corporate tax rate around the world

Reduce the corporate tax rate to something lower?

Australian Corporate Tax Rate

- The corporate tax rate is 30 percent. The corporate income tax rate applies to both resident and non-resident companies. A resident company is liable to corporate income tax on its worldwide income and capital gains. A non-resident company is liable to corporate income tax on its Australian-source income only, and on capital gains from the disposal of an asset that is taxable Australian real property (TARP). Broadly, TARP will include Australian real property and certain indirect interests in Australian real property. The Australian tax system provides taxation relief against international double taxation by granting foreign tax offsets in some circumstances and in others, by exempting the foreign income from Australian tax. The corporate income tax rate applies to income earned during the period from 1 July to 30 June of the following year.

- Indirect tax There has been no changes to the GST rate of 10 percent since it was introduced.

Also provides relief against international double taxation

- Exclusion method and credit method will apply depending on where you are earning your income.

- Dividend imputation credits are worthless for foreign investors

- tax rules can have an effect

Withholding Tax

- Withholding taxes are withheld from the payments a corporation makes to the taxpayer.

- The taxes are levied on passive income earned by an individual or corporation of one country within the tax jurisdiction of another country.

- Passive income includes income from dividends and interest, royalties, patents, or copyrights.

- In Australia, the tax on dividends is 15% (may depend on tax treaty), on royalties/patents/copyright it is 5%

- A withholding tax is an indirect tax.\

Loyalties, patents, copyrights

- will attract a withholding tax

no incentive to file tax returns

Value-Added Tax

- A value-added tax (e.g. GST in Australia) is an indirect national tax levied on the value added in production of a good or service.

- It is an indirect tax.

- In terms of incentives, GST/VAT differs from corporate taxes

- An income tax has the incentive effect of discouraging work.

- A GST/VAT has the incentive effect of discouraging consumption (thereby encouraging saving.)

- GST is easier to administer. It is 10% in Australia.

What is the purpose of imposing the tax?

- too higher tax - will money flow out of the country?

- GST - easier to administer - 10% in most countries

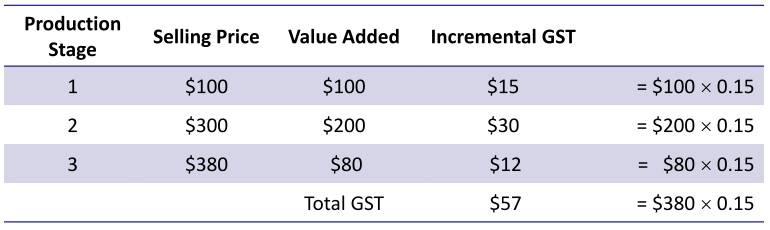

Value-added tax calculation

- Assume the tax rate is 15%. Suppose that stage one is the sale of raw materials to the manufacturer, stage two is the sale of finished goods to the retailer, and stage three is the sale of inventory from the retailer to the consumer.

Added at each 'value add' cycle

- lucrative tax for countries,

National Tax Environments

- Worldwide taxation

- Residents of a country are taxed on their worldwide income, no matter in which country it was earned.

- Territorial taxation

- Residents of a country are taxed based on where the taxable event occurred.

- Foreign tax credits

- Allocation of Debt (or Earnings Stripping)

Territorial Taxation system

- Australia has a taxable income, pay only on the income you have earned here

- not notionally on countries outside Australia

- Microsoft does have to pay taxes for entities physically in Australia

What roles does debt play in the debt scheme in place?

- Allocate debt across subsidiaries to minimise

- What is it about debt that aligns with tax policies?

- Interest tax shield - borrow money with high tax rates, shield income from taxes in high tax environments

- Allocation of debt becomes a country with high tax rates

- Earning stripping - set a capitalisation rate for each country (D/V cannot exceed in a particular country)

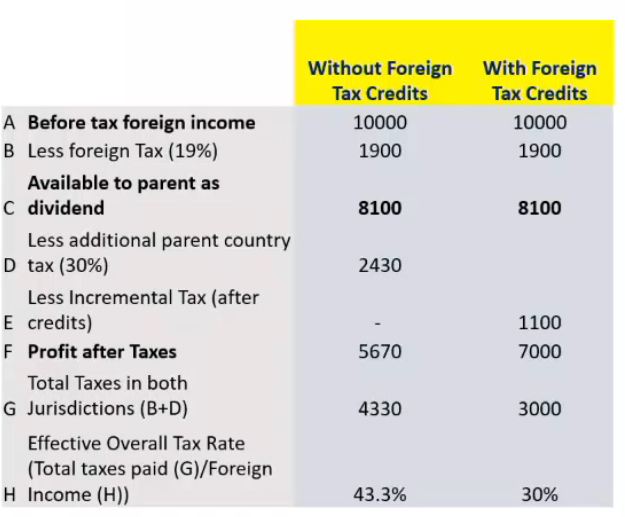

Foreign Tax Credits

- Allow taxpayers to recover somewhat from double taxation.

- It’s a direct reduction of taxes that would otherwise be due and payable.

- Direct foreign tax credits are computed for direct taxes paid on active foreign-source income of a foreign branch of a U.S. MNC or on withholding taxes withheld from passive income.

- Indirect foreign tax credits are for income taxes deemed paid by the subsidiary.

Reduction of taxes that would otherwise be payable

- Example in lecture - use foreign tax credits

Indirect foreign tax credits

- get some recognition that subsidiary also paid taxes

FTC Example

- Assume that an Australian firm has a subsidiary in the UK. UK (Australian) corporate tax rate is 19%

Branch vs Subsidiary Income

- An overseas affiliate of a MNC can be organized as a branch or a subsidiary.

- A foreign branch is not an independently incorporated firm separate from the parent.

- Branch income passes directly through to the parent’s income statements.

- A foreign subsidiary is an affiliate organization of the MNC that is independently incorporated.

- Income may not be taxed in the U.S. until it is repatriated, under certain circumstances.

Won't pay taxes until you repatriate you income back home

- play games with incorporation

Transfer Pricing

- Having foreign affiliates offers transfer price tax arbitrage strategies.

- The transfer price is the accounting value assigned

to a good or service as it is transferred from one

affiliate to another.

- See Lecture 8 example (worksheet “Payments to Parent”)

- It is a method of transferring funds out of the foreign

subsidiary

- If one country has high taxes, don’t recognize income there—have those affiliates pay high transfer prices.

- If one country has low taxes, recognize income there— have those affiliates pay low transfer prices.

Pricing of goods and services which is transferred to a subsidiary

- How much does a subsidiary charge from one affiliate to another?

- increase the price I charge to subsidiary, can reduce the tax charged in the foreign locale

- How much does the subsidiary charge to the parent company

- Pay of transferring funds out of a subsidiary

Operating in a low tax environment, want to maximise income in a low tax environment

- charge subsidiary for the goods and services it sells

- The pricing of goods, services and technology transferred enter directly into the cost of goods sold component of the subsidiary’s income statement.

- The price should be one that a willing seller would charge a willing unrelated buyer.

- Managers should address several issues

- Fund positioning effect

- Income tax effect (see example in next slide)

- Managerial incentives

- The effect of joint ventures

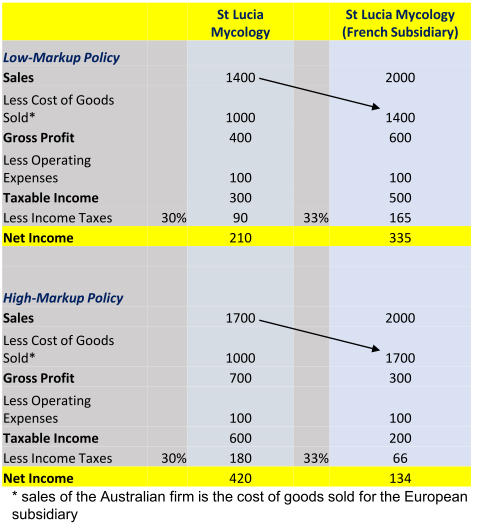

High tax rates, increase the cost of goods sold

- company looks like it's performing poorly

- what impact does this have on their compensation package?

- St Lucia is operating in France, a relatively high tax country, and in Australia. Tax in France (Australia) is 33% (30%).

increase the sales revenue (price selling to FC)

- France has higher tax rate, don't want ot show income in France

- Reduces taxable income in France, lower income in French company

- Mechanically follow this, boosts income of the Aus parent company

- High taxes, what should the markup policy be?

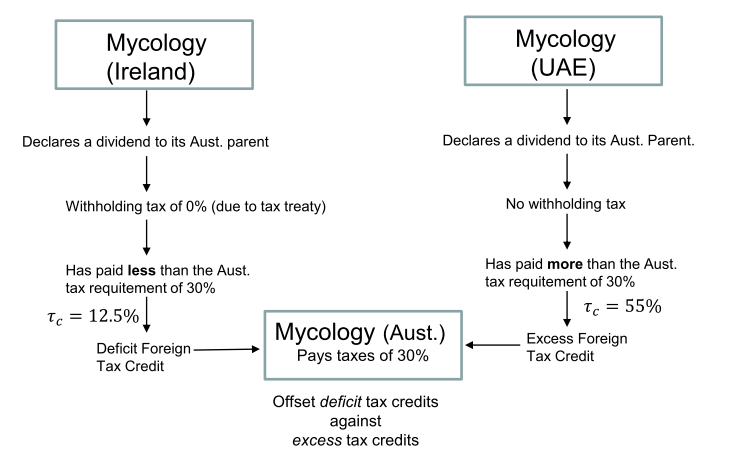

Cross crediting

- The ability of cross-credit is valuable

- It involves offsetting foreign tax credits with foreign tax deficits in the same period

Allow you to offset tax credits against tax deficits

- One country have credits, another country I have deficits

E.g. Aus Company has two subsidiaries

- Irish country has dividend, deficit foreign tax credit

- UAE has Excess foreign tax credit

- Can use UAE excess to write off deficit from Ireland

Tax Havens

- Tax havens are countries with low corporate income tax rates and low withholding tax rates on passive income.

- Tax havens were once useful as locations for an MNC to establish a shell company.

- Most countries are clamping down on it use

- In the US, the Tax Reform Act of 1986 greatly diminished the need for and ability of U.S. corporations to profit from the use of tax havens.

- Setup a subsidiary in that tax haven, direct income to the tax haven which

- Countries clamping down, need to have majority operations there

Corporate Inversion

- A Corporate inversion is the changing of a country’s

country of incorporation.

- By reincorporating in a lower-tax jurisdiction firms reduce their global tax liabilities.

- All it is is a new corporate home.

- Rules have been put in place to prevent naked

inversions. They allow for inversions when

- Substantial business presence

- Merger with a larger foreign firm

- Merger with a smaller foreign firm

A new corporate home

- Obama administration, acquisitions were done purely for shifting the corporate home from high tax country to a low tax one

- Argument made to IRS that there is a substantial change to how the country will operate

International Tax

- Taxes matter

- The three basic types of taxation are income tax, withholding tax, and value-added tax.

- Nations often tax the worldwide income of resident taxpayers and also the income of foreign taxpayers doing business within their territorial boundaries.

- If countries simultaneously apply both methods, double taxation will result unless a mechanism is established to prevent it. Foreign tax credit eliminates double taxation.

- Transfer pricing is a means to reposition funds within a MNC and a possible technique for reducing tax liabilities.

Taxing advantage of taxes is not unethical or illegal

- Want to minimise after tax cash flows

- Need to think about all the tax shields that are available

- R&D, non-debt tax shield, used to minimise taxable income

- Foreign tax credits, maximise income over all countries