Lecture 2

International Monetary System

- The international Monetary System is a set of rules that governs international payments

- Historical Overview of exchange rate mechanisms

- Classical Gold Standard: 1875 – 1914

- Fixed exchange rate system. Every single country would decide what the value of their currency was worth compared to gold.

- Worked for a long period of time - exchange rates were fairly stable

- Not too much gold discovery, but around 1911 huge amounts fo gold discovery and gold inflation became a problem

- Bretton Woods System: 1945 – 1972

- Floating Exchange Rate Regime: 1973 – Present

- market flows determine the value of one currency to another

- European Monetary Union: 1979 – Present

- European currencies pegged their value against the deutsche currency

- late 90's got rid of various European currencies

- Classical Gold Standard: 1875 – 1914

- The system, or regime, is classified as either a fixed, floating, or managed exchange rate regime

- The rate at which the currency is fixed, or pegged, is frequently referred to as its par value

- fixed against another currency

- If the government doesn’t interfere in the valuation of its currency, the currency is classified as floating or flexible

- market value will determine what a currency is compared to a floating currency

- The rate at which the currency is fixed, or pegged, is frequently referred to as its par value

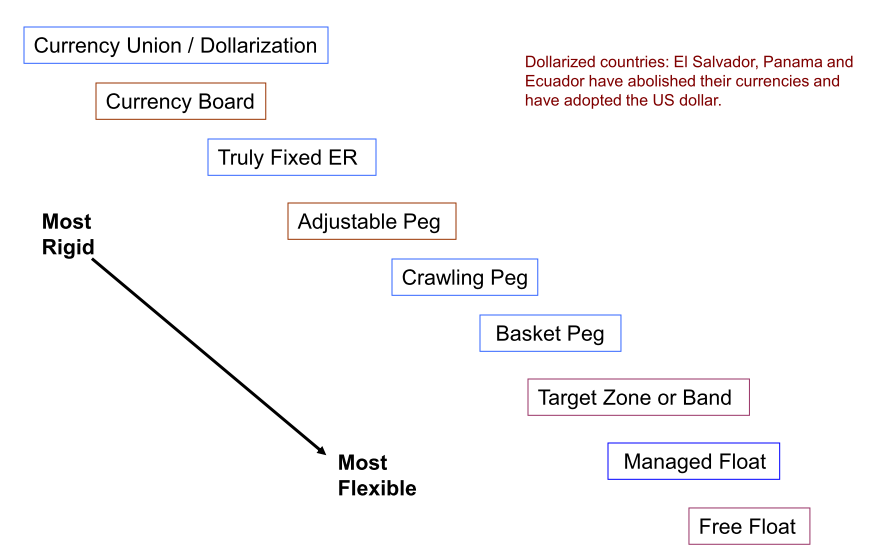

Fixed ER:

- every dollar from one currency has to be matched relative to a second currency Adjustable peg

- change your currency relative to another currency but allow the opportunity to change the peg Free floating system

- fully flexible

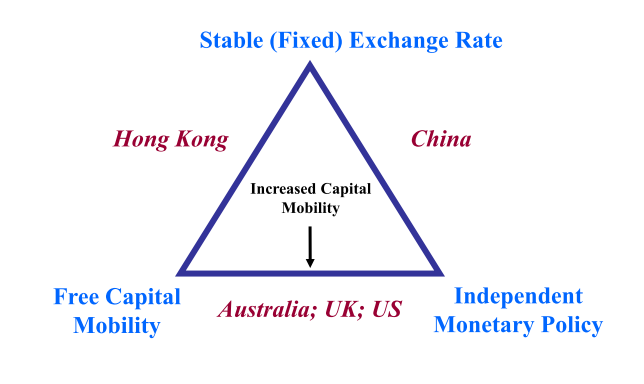

Currency Board: Hong Kong

- Central bank of hong Kong stands to buy any Forex to maintain their price

- defend their par value

Since 1982, Hong Kong dollar has remained a very stable exchange rate

Fixed exchange rate system

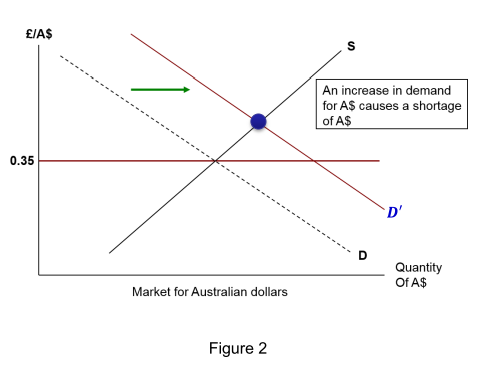

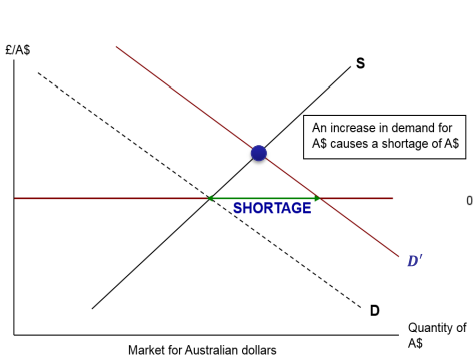

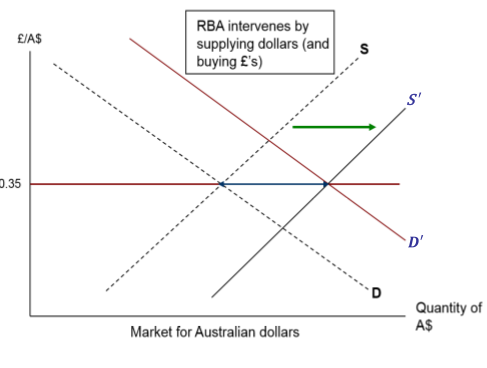

| £0.35/$ is referred to as the “par value” i.e., AUD is fixed relative to GBP (anchor currency) at £0.35/$. | Fig 2: The exchange rate is "undervalued” at the par value of £0.35/$. |

|---|---|

|

|

|

|

- Calculating risk, use the standard devation of returns

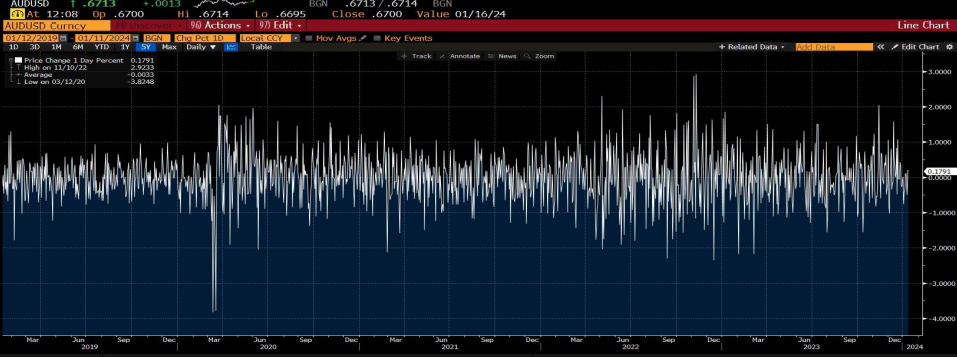

The floating Exchange rate (post 1973)

- Under the floating rate system, the exchange rate is determined entirely by forces of supply and demand

- The system that prevailed was not quite “freely floating”

- Central banks had the obligation to intervene to prevent “disorderly conditions”

- A lot of rules in place, rules of capital movements

- Capital controls were abolished and access to the US capital market was allowed

- Monetary and macro-economic policies were independent to that of US

- Have independent monetary policies

| 5 year window | % window |

|---|---|

|

|

Advantages of a Fixed ER

- Reduce transaction costs and exchange rate risk which can discourage trade and investment

- Provide a credible nominal anchor for monetary policy (importing credibility)

- Transparency of the Regime

Advantages of a Float

- Ability to pursue an independent monetary policy

- Ability to use monetary policy to respond to recessionary effects on the economy

Attributes of the "ideal currency

- Exchange rate stability

- Full financial integration (free flow of capital)

- No capital or investment controls. Move money easily

- Monetary independence (of domestic policies)

The impossible Trinity

A country must give up one of the three goals:

- Exchange rate stability

- Full financial integration (free flow of capital)

- Monetary independence (of domestic policies)

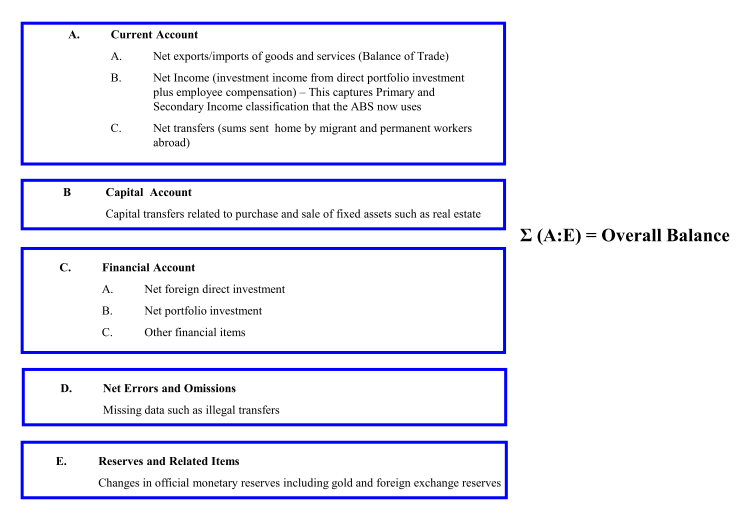

The Balance of Payments (BOP)

- The BOP is a statistical record of the flow of all of the payments between the residents of a country and the rest of the world in a given year.

- Multinational businesses use various BOP measures to gauge the growth and health of specific types of trade or financial transactions by country and regions of the world against the home country

- Monetary and fiscal policy must take the BOP into account at the national level - the BOP gives indications of the demand and supply of a country’s currency.

- statistical record of the inflows and outflows of cash from the country (where and what was it used for)

- Used to gauge the health of the country

- Government spending relative to its revenue, etc.

For example, an overall BOP deficit indicates that a country is borrowing from overseas and running down its net asset position.

A country running a CA surplus is accumulating claims on foreigners and building up a positive net foreign asset position.

Fundamentals of BOP Accounting

- Transactions are recorded on the basis of double entry bookkeeping – by definition it has to balance

- Every “source” must have a “use”

- BOP is a statement of flows, thus like a cash flow statement, not a balance sheet.

- Every economic transaction recorded as a credit brings about an equal and offsetting debit entry

Accounting principles

- Any transaction resulting in a payment to foreigners is entered in the BOP accounts as a debit and is given a negative sign.

- Any transaction resulting in a receipt from foreigners is entered as a credit and given a positive sign.

- To reiterate, every international transaction automatically enters the BOP twice, once as a credit and once as a debit

- If you buy something from a foreigner, you have to pay for it, and the foreigner has to either spend or store your payment.

- Examples of these paired transactions will be covered in the tutorial.

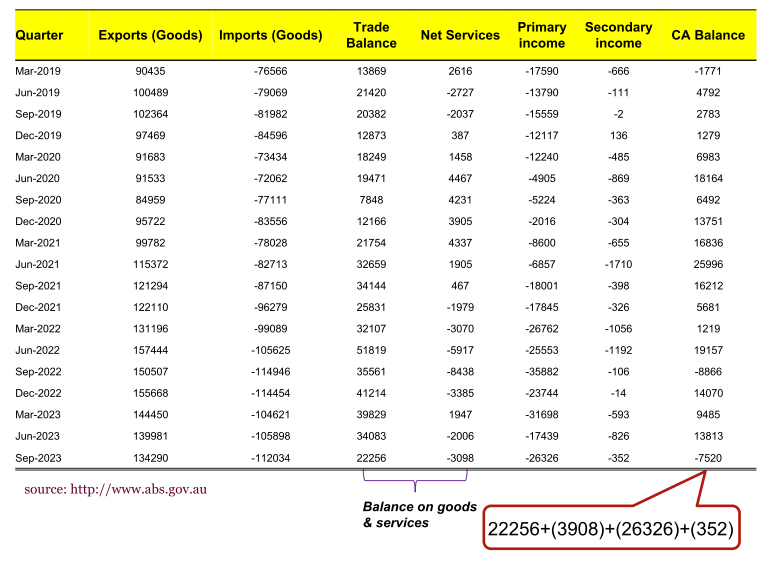

Current account

- It is record of a country’s trade in goods and services and of unilateral transfers.

- It is divided into several sub-categories:

- Merchandise Trade: physical goods like beef, cars etc.

- Services: tourism, education, shipping and finance etc.

- Any service provided by trips and tourism

- Primary Income (“investment income”): interest income, dividends etc.

- Secondary Income (“unilateral transfers”): Foreign aid, pensions to retired people abroad, wages repatriated etc.

- The sum of the sub-categories = CA balance

Note: a country must finance its current account deficit either by borrowing from foreigners or by drawing down on its previously accumulated foreign wealth, a current account deficit represents a reduction in the country’s net foreign wealth

CA = Exports (x) - Imports (M)

- Current Account Deficit:

- Current Account Surplus:

Current Account Balance = Change in Net Foreign Wealth/Assets

Implication: A country with a CA deficit must be increasing its net foreign debts by the amount of the deficit

- borrow from the rest of the world to be able to consume

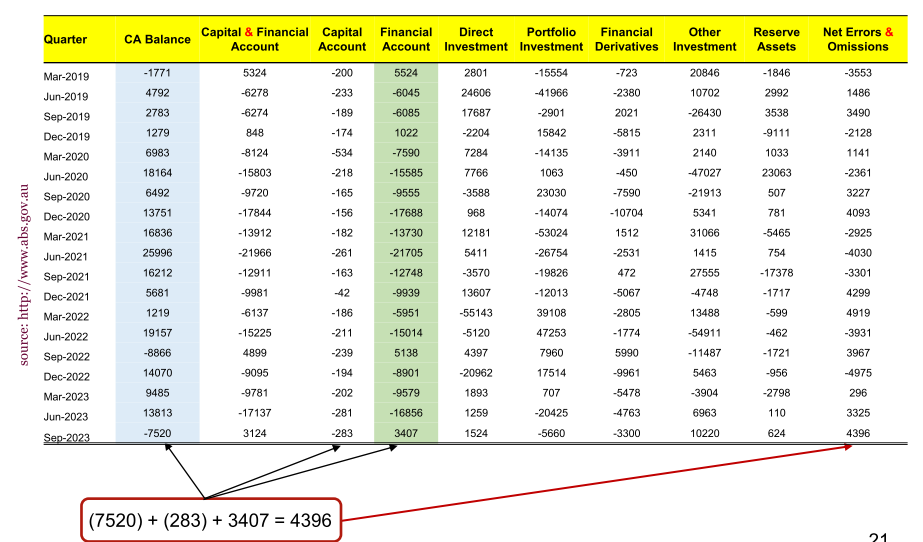

The Financial Account

- It includes all short- and long-term financial transactions pertaining to both international trade and flows associated with portfolio shifts (stocks, bonds etc.)

KA = Capital Inflow (cr) – Capital outflow (dr)

- The two main categories:

- Portfolio investment

- Direct investment (takeover or acquiring a substantial portion of a foreign company, i.e., ˃ 10%)

-

Sales of assets are recorded as credits, and result in inflows to the KA account. Purchases (imports) of foreign assets are recorded as debits and lead to capital outflow.

- KA balance = Sum of portfolio investment and direct investment +

- Any returns on investment from international trades are accounted in the financial account

- Accurate to keep track of the transactions in the financial account

- reserve assets - assets held by the central bank (gold, etc)

- Errors and Omissions - difference between CA balance, Capital Account and Financial Account

- Errors and omissions also used in valuations

Other Assets

- Official Reserves: Total reserves held by official monetary authorities within a country (RBA in Australia).

- These reserves are typically comprised of major currencies that are used in international trade and financial transactions, gold and reserve accounts (SDRs) held at the IMF.

- Important account for fixed-rate regime countries (i.e., HK).

- For floating rate regime countries, such as the U.S. and Australia, official reserves are relatively unimportant.

- Net Errors and Omissions: Account is used to account for statistical errors and/or untraceable monies within a country

- the only way you can run a deficit if is someone is willing to fund it - funded by the central bank

Balance of Payments

Assuming change in official reserves and errors are approximately zero:

Current Account = (-) Financial Account

This will hold approximately for floating rate countries.

Summary

- The two major sub-accounts of the BOP, the Current and Capital/Financial Account, summarize the current tradeflows and international capital flows of a country.

- The Current and Capital/Financial Account are typically inverse on balance, one in surplus while the other experiences deficit.

- Although most nations strive for Current Account surpluses, it is not clear that a zero balance or a surplus on the Current Account is necessarily desirable.

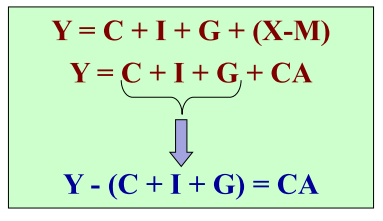

Linking CA to national income

- gauge the health of an economy

- CA balance relative to the GDP

Forms:

- Y = National Income

- = Domestic Residents Spending / Absorption

- CA = excess of spending over income earned (Income – Spending)

- CA Deficit → → Borrowing from Abroad to finance domestic spending

- CA Surplus → → Lending Abroad

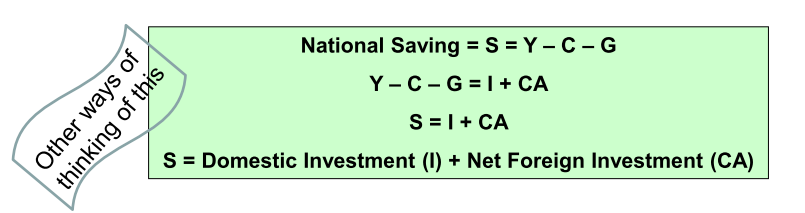

Savings, Investment & the CA

- Macro identities for a country:

- National Income = Consumption + Savings

- National Spending = Consumption + Investment

Conversely:

-

If National Investment < National Saving, then Net foreign investment > 0

- Implication: If a country’s spending exceeds its income, domestic savings is not enough to fund domestic investment, the country will need to import capital. This deficit of capital will come from overseas and will be reflected as a financial account surplus for that country.

- The link between the financial and current account:

-

National Income – National spending = Exports – Imports

-

Savings – Investment = Exports – Imports

-

Government budget deficits and current account deficits:

- National spending (NS) = Household (HH) spending + Private investment (PI) + Govt. spending

- What households spend, what investment companies spend and what government spends

- HH spending = National Income – Private Savings – Taxes

- So,

- National spending (NS) = Household (HH) spending + Private investment (PI) + Govt. spending

National spending = [NI – PS – T] + PI + Govt. Spending

NI – NS = (PS – PI) + (Taxes – Govt. spending)

= Savings surplus + Govt. surplus

= Exports – Imports (i.e., CA balance)

- Current account deficit implies private savings + govt. budget is in deficit

Are we consuming more debt because we are funding postive NPV projects or are me consuming more debt because residents are taking on more debt?

Implications

- A current account deficit means a country is not saving enough to finance its domestic investment + government budget deficit

- A current account deficit represents a collective national decision to consume and invest more than the nation is producing.

Are CA deficits Sustainable?

- A growing economy can expect to run a current account deficit

- Countries that have large investment opportunities can run large current account deficits. Sometimes it makes sense to borrow abroad temporarily.

- The absolute level of both savings and investment are important

- A CA deficit caused by low savings (high consumption spending) is less likely to be sustainable than a CA deficit because of high investment (recall CA balance = S – I)

- This is because higher investment increases future production capacity and the ability to pay back foreign liabilities

- Composition of Investment Spending is important

- The more the investment is in traded goods, then more likely to generate trade surpluses.

- The manner in which CA deficits are financed is what matters