Lecture 3 - Parity conditions

- Managers of multinational firms, international investors,

importers and exporters, and government officials must

deal with these fundamental issues:

- Are changes in exchange rates predictable?

- How are exchange rates related to interest rates?

- What, at least theoretically, is the “proper” exchange rate?

- given the interest rate and inflation at a point in time

- Our approach to answering these questions and more is to describe the economic fundamentals of international finance, known as parity conditions.

- Use back on the envelope conditions to find where the exchange rate should be heading

Parity conditions

- Parity Conditions provide an intuitive explanation of the movement of prices and interest rates in different markets in relation to exchange rates.

- Parity conditions rely on ARBITRAGE to hold.

- if under or overvalues, execute trade to create arbitrage profit

- The derivation of these conditions requires the assumption of Perfect Capital Markets (PCM).

- no transaction costs

- no taxes

- complete certainty

- If we enter into a transaction, certain that is the price will be held at that price

Purchasing Power Parity

- PPP is based on the notion of arbitrage across goods markets and the basic building block of PPP is given by the Law of One Price (LOP)

- LOP states that the price of an identical good should be the same in all markets (assuming no transactions costs).

- Otherwise, one could make profits by buying the good in the cheap market and reselling it in the expensive market.

- Basic Idea: A can of coke should cost the same in Australia as it does in London when expressed in a common currency (either in AUD or GBP).

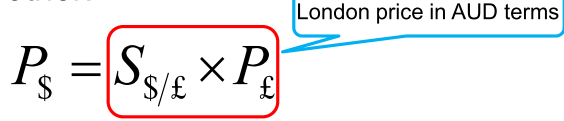

The law of one price

- States that a while product’s price may be stated in

different currency terms, but the price of the product in a

common currency should remain the same.

- Comparison of prices would only require conversion from one currency to the other:

S: exchange rate $/pound

Conversely, the exchange rate could be deduced from the relative local product prices:

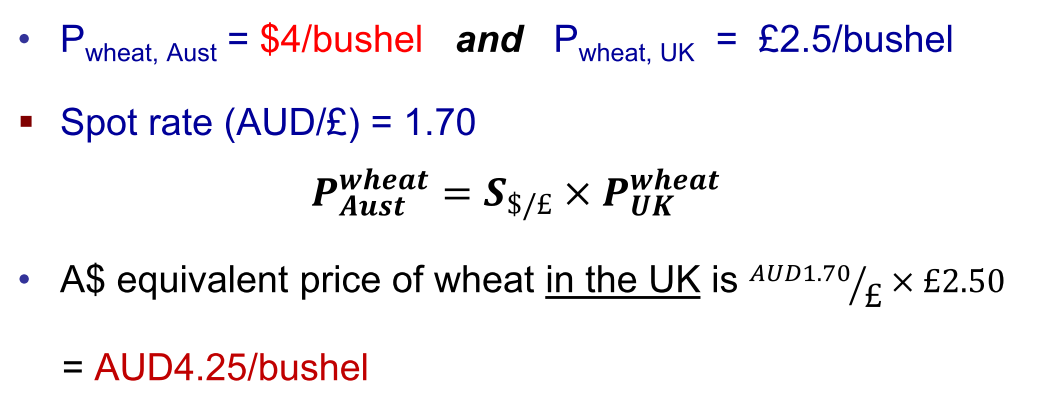

- Implication: The demand for Australian wheat will increase forcing up its price. The price of UK wheat will drop.

- Other costs, such as shipping, taxes, etc. are not incorporate into this difference

- Has to be substantially large to exploit this opportunity

- Only applied to traded goods - not services such as hair cuts, cleaning etc.

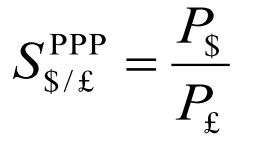

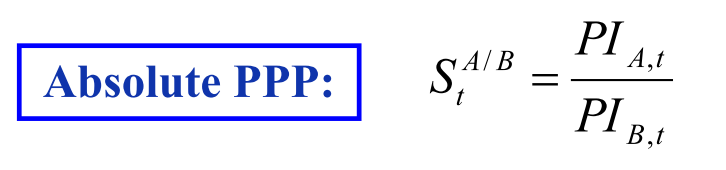

Absolute PPP

- A less extreme form of the Law of One Price is the ABSOLUTE PPP which says that the price of a basket of goods would be the same in each market.

- The PPP exchange rate between the two countries would then be: PI: Price-Index basket of goods at time

- The price of those two basket of goods have to be the same

- are the price indices of the two countries (e.g. consumer price index) at time t

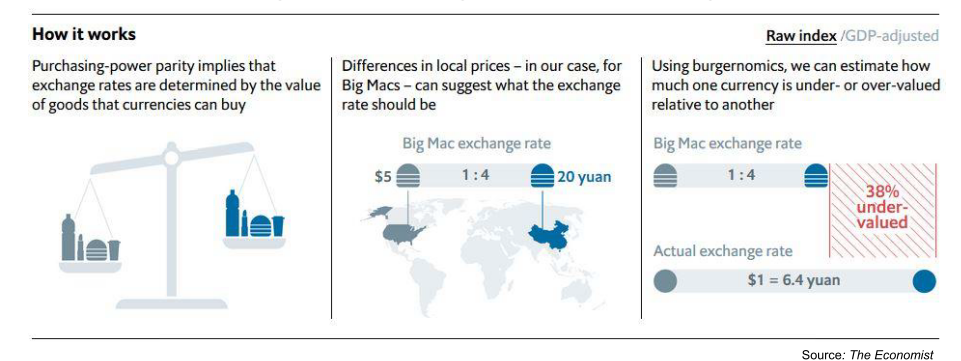

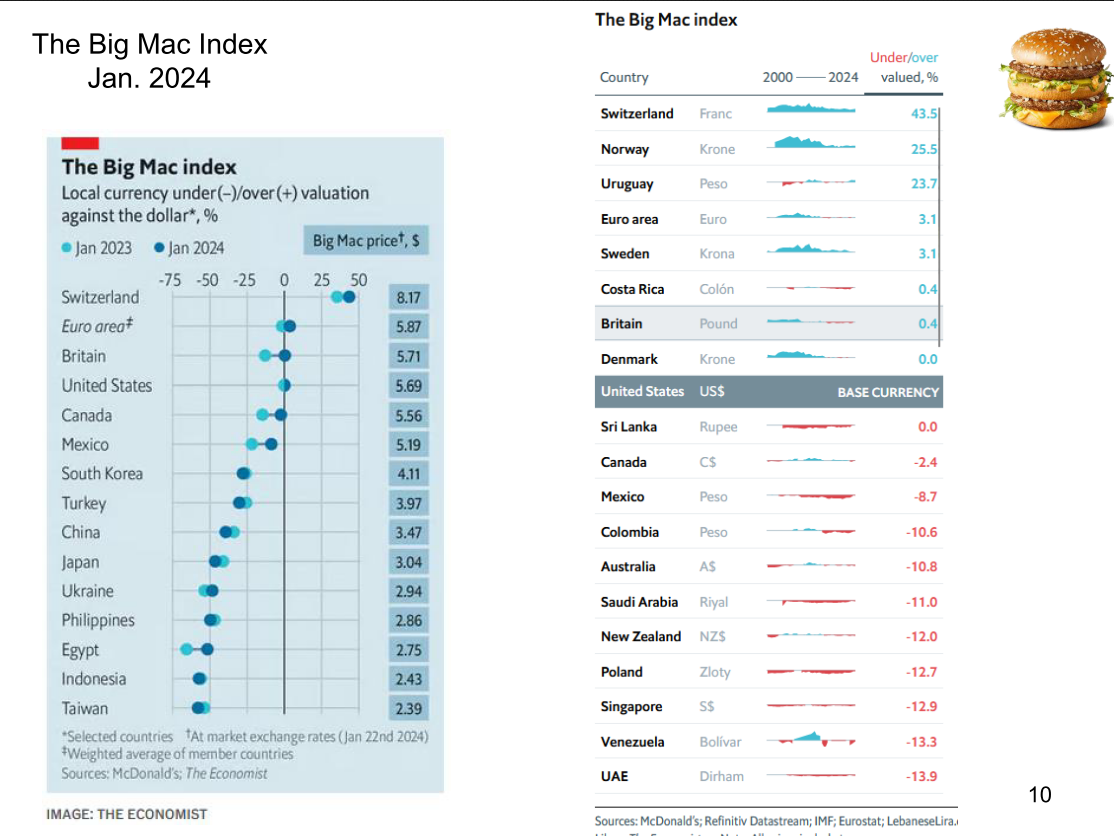

- The Big Mac Index is an example of this variant of PPP.

- the economist puts out every three months

The Big Mac Index

- most famous test of the Law of One Price is The Economist magazine’s Big Mac Hamburger standard.

-

The Big Mac can be viewed as a standardized bundle of goods that are individually traded, so we would expect it will only hold approximately.

-

calcuate whether it it over or undervalued relative to the US dollar

- Theoretically can buy a big MAC in a country where it is undervalued and sell it in a country where it is overvalued

- Also include things like rent, labour, in the calculation of big Mac burger

How well does it work?

- Violations of Absolute PPP occur in the short run, but it tends to hold in the long run (several years).

- Describes a long-run phenomenon due to the fast speed adjustment in exchange rates relative to the “sticky” nature of goods prices.

- Over short horizons, exchange rates are too volatile, and goods prices are too sticky, for this theory to work well in the short-term.

- Can't re-negotiate a long term deal, e.g.

- Over short horizons, exchange rates are too volatile, and goods prices are too sticky, for this theory to work well in the short-term.

- The presence of imperfections such as taxes, transaction costs, import tariffs and quotas.

- Basket of commodities might be different for different countries. Also, it will not hold if the price indices do NOT have the same weights across countries.

- composition of the basket of goods. Assumes the goods across two countries have to be the same. Composition of goods vary between countries

- The inclusion of non-tradeable goods and services in price indices.

- Describes a long-run phenomenon due to the fast speed adjustment in exchange rates relative to the “sticky” nature of goods prices.

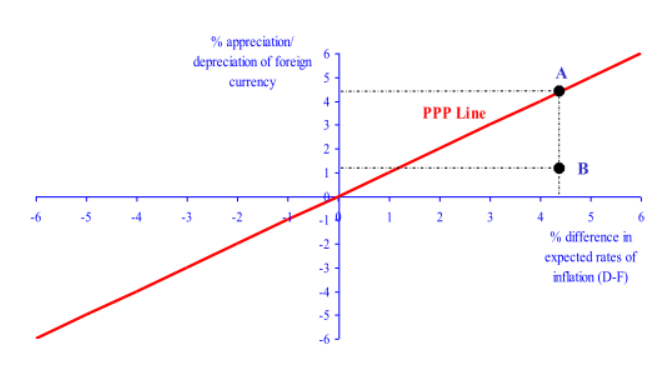

Relative PPP

- Relative PPP claims that exchange rate movements should exactly offset any inflation differential between two countries:

- compare inflation between two countries and predict the exchange rate

- Country with the higher inflation rate should decline against the country with the lower inflation rate

: the inflation rate of country A, B

Relative PPP:

Exchange rate differential = inflation rate differential

Approximate inflation rate differential

Relative PPP

Given inflation rates of 1.9% and 3% in Australia and the UK respectively, what is the prediction of PPP with regards to $A/GBP exchange rate?

- General implication of relative PPP is that countries with high rates of inflation will see their currencies depreciate against those with low rates of inflation

Applications of relative PPP

- Forecasting future spot exchange rates.

- Calculating appreciation in “real” exchange rates. This will provide a measure of how expensive a country’s goods have become (relative to another country’s).

- More expensive relative to another country creates challenges - more competition, etc.

Forecasting Future Spot rates

- Suppose the ¥/$ spot exchange rate and expected inflation for Japan and Australia are:

- What is the expected ¥/$ exchange rate if relative PPP holds?

The Real Exchange Rate

- The real exchange rate measures deviations from PPP.

- That is, changes in the spot exchange rate that do not reflect differences in inflation rates between the two currencies in question.

Real Exchange Rate

Real Exchange Rate

- Appreciation in the real exchange rate measures deviations from PPP.

- When E = 1, the denominator currency is valued correctly. The competitiveness of this country is unaltered.

- When E < 1, the denominator currency is undervalued. Products from the other country seem expensive relative to the base year. That is, the competitiveness of the denominator country improves.

- When E > 1, the denominator currency is overvalued. Products from the other country seem cheap relative to the base year. That is, the competitiveness of the denominator country deteriorates.

Interest Rate Parity

- Interest rate parity (IRP) is an arbitrage condition that provides the linkage between the foreign exchange markets and the international money markets.

AND

percentage forward premium = interest rate differential

-

How does the market arrive at the bid forward exchange rates?

- need current spot exchange rate, plus interest MM interest rate

- subtract 1 from both sides, you have the percentage forward differential - way of presenting the forward rates

- RHS - inflation differential

-

In general, the currency trading at a forward premium (discount) is the one from the country with the lower (higher) interest rate.

Example

- Suppose Gattinara Corp. has funds that it can place in the money market for 3 months. The options are

- Invest in Australia

- Invest in foreign currency denominated securities

- The returns on an Australian investment is given by

- The return on foreign investment is given by

- Gattinara Corp will be indifferent between the two investment opportunities if

- Basic idea: Two alternative ways to transform from currency A at time 0 to currency B at time 1 should earn the same return.

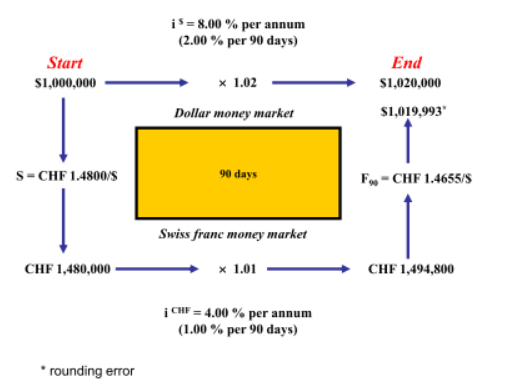

- Thus, an AUS investor with $1 million to invest should be indifferent between holding dollar-denominated securities for 90 days earning 8.00% per annum and holding Swiss franc-denominated securities of similar risk and maturity earning 4.00% per annum, when “cover” against currency risk is obtained with a forward contract.

- percentage forward premium should be equal to the interest rate differential

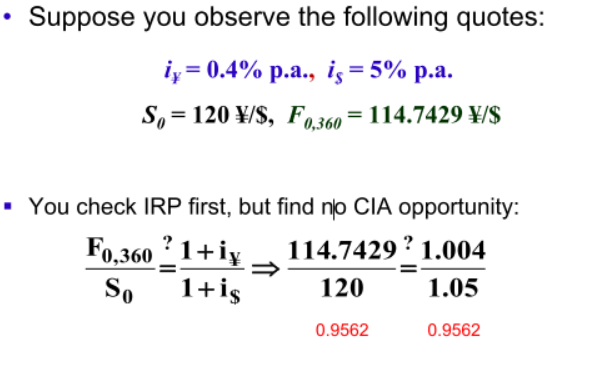

Example

- Suppose the 3-month money market rate is 8% p.a. (2% for 3-months) in the U.S. and 4%p.a. (1% for 3-months) in Switzerland, and the spot exchange rate is CHF1.48/$.

- The 3-month forward rate must be CHF1.4655/$ to prevent arbitrage opportunities (i.e., interest rate parity must hold).

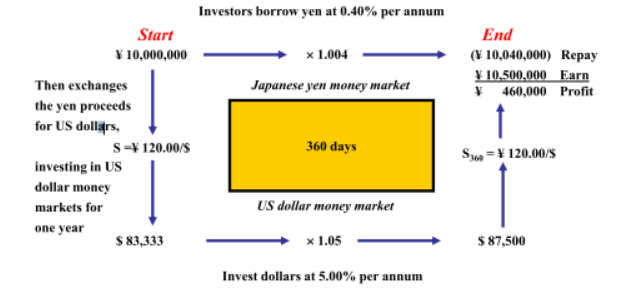

Why Parity Holds?

- This must hold by arbitrage. Otherwise, riskless profits

could be made. This is known as covered interest

arbitrage (CIA) and occurs whenever IRP does NOT hold. CIA can involve the following steps:

- Borrow the domestic currency;

- Exchange the domestic currency for the foreign currency in the spot market;

- Invest the foreign currency in an interest-bearing instrument; and then

- Sign a forward contract to “lock in” a future exchange rate at which to convert the foreign currency proceeds back to the domestic currency.

Example 2

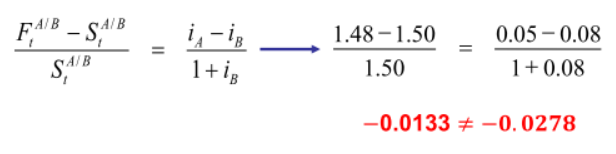

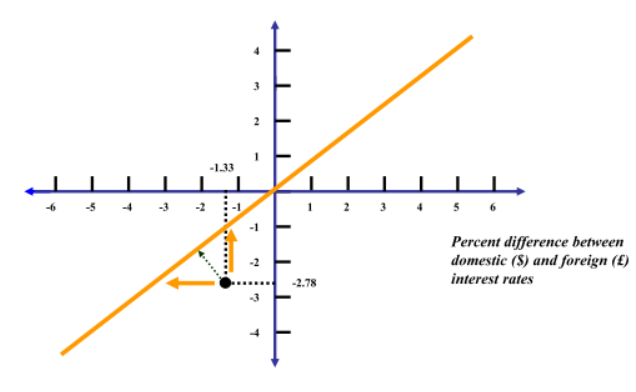

- The annual interest rate in the AUS and UK are 5% and 8% respectively. The current spot rate is $1.50/£ and the 1 year forward rate is $1.48/£. Can arbitrage profits be made?

Covered Interest Arbitrage

- Covered interest arbitrage (CIA) should continue until interest rate parity is re-established, because the arbitrageurs are able to earn risk-free profits by repeating the cycle.

- But their actions nudge the foreign exchange and money markets back toward equilibrium:

- Purchase of Pounds in the spot market and sale of pounds in the forward market narrow the premium on forward pounds.

- The demand for pound-denominated securities causes the pound interest rates to fall, while the higher level of borrowing in Australia causes dollar interest rates to rise.

- forward rates will changes, and interest rate will; push back to the parity condition

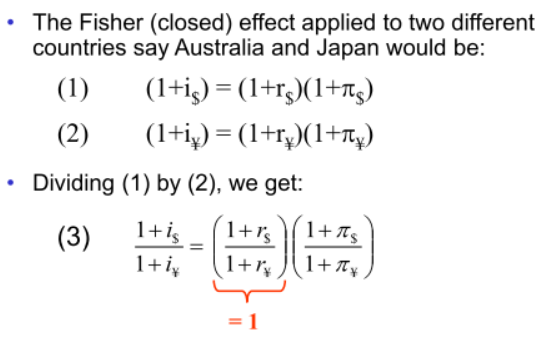

The Fisher Effect

- The Fisher effect (also called Fisher-closed) postulated by Irving Fisher states:

- inflation

- real interest rate

- nominal interest rate

This relation is often presented as a linear approximation stating that the nominal interest rate (i) is equal to a real interest rate (r) plus expected inflation ()

- Applied to two different countries, like the Australia and Japan, the Fisher Effect would be stated as:

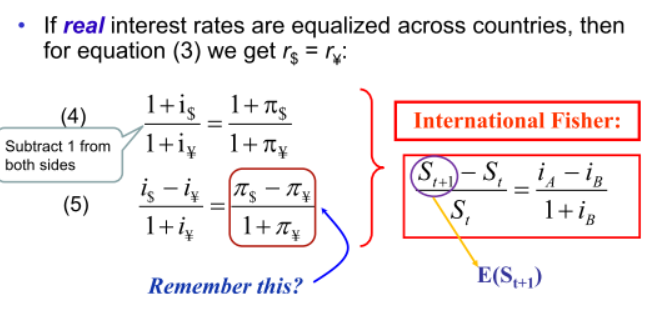

The International Fisher Effect

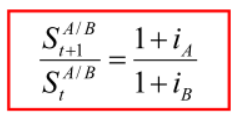

- The International Fisher Effect (also called Fisher-open or Uncovered Interest rate parity condition) states that the spot exchange rate should change to adjust for differences in nominal interest rates between two countries:

- Expected future spot rate

- assume the real interest rate should be the same between two countries

- want to forecast the exchange rate, look at the interest rates

- IRP forward rates, spot rates and interest rates

Uncovered Interest Rate Parity

- Suppose you forecast the spot rate next year to remain unchanged at 120 ¥/$

- Even though you cannot make a risk-less profit through CIA, given your estimation of the future spot rate, you can enter into an uncovered interest “arbitrage”

- In an uncovered position, rather than locking in a forward rate today, you take your chances and hope you’re right about your assessment of the future spot rate

- Predicted spot rate of ¥/$ is higher than the relative interest rates, therefore borrow yen

Forward Exchange Expectations

- The Forward Rate as an Unbiased Predictor of the Future Spot Rate

- Some forecasters believe that for the major floating currencies, foreign exchange markets are “efficient” and forward exchange rates are unbiased predictors of future exchange rates.

- The forward exchange hypothesis states that the forward exchange rate, quoted at time t for delivery at time t+1, is equal to the expected value of the spot exchange rate at time t+1.

- The Forward rate is said to be an unbiased predictor. Unbiased prediction means that the forward rate will, on average, overestimate and underestimate the actual future spot rate in equal frequency and degree. It implies that the expected forecast error is zero.

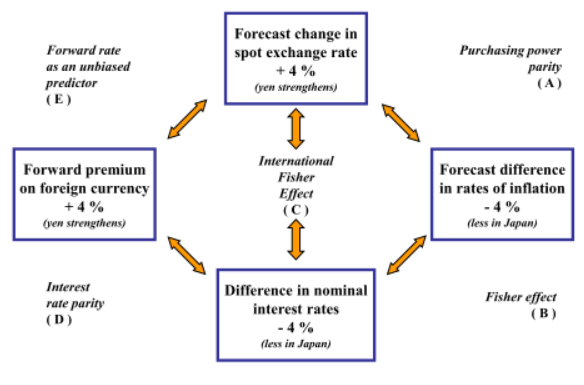

All parities example

- Suppose expected inflation in Japan is 1% and expected inflation in the U.S. is 5%. The current spot exchange rate is ¥104.00/$ and the one-year forward rate is ¥100.00/$.

- See that all of our parity conditions predict that the ¥ will appreciate 4% relative to the $ over the next year.