Lecture 6: Hedging Economic Exposure

Types of Exchange Rate Exposure: A Revisit

- Transaction Exposure – A short-term exposure that is due to transactions having to be settled in a foreign currency (see Lecture 5)

- Translation Exposure – arises due to the need to consolidate financial statements of foreign operations into home currency

- Economic/Operating Exposure – the impact of currency fluctuations on a firm’s future cash flows.

Unanticipated risks in exchanges

- Take a long term or short term view

- short term; transaction exposure; firms have contractual payments and receivables

- payment will vary depending on the exchange rate

- when you do the conversion in the future, could be receiving less in the future

- Use financial hedging techniques to limit the risk Do not cover translation exposure in this course

Economic/operating exposure

- impact of currency fluctuations

- revenues - costs

- need to determine the impacts exchange rates will have on revenues and costs

- economic value is discounted sum of future cash flows

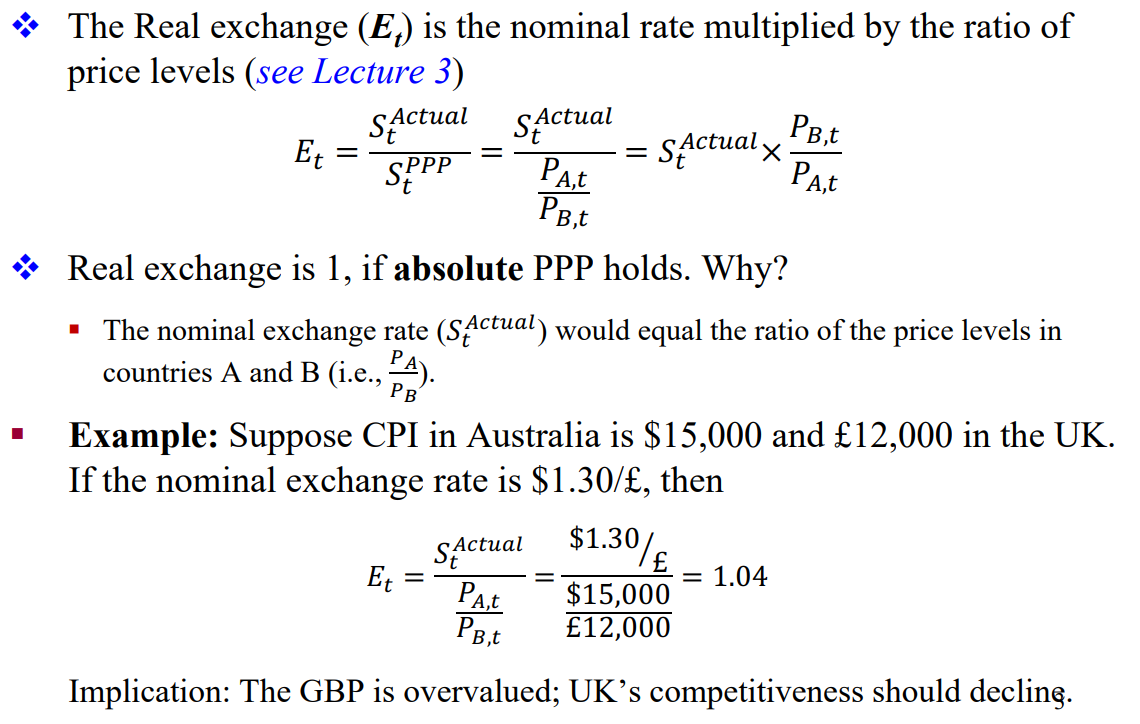

Real exchange Rate Recap:

- basket of goods have to be identical

- real exchange rate - ratio of two price currencies

- 1.04 implication, denominator is overvalued, british pay too much for goods and should decline over time

- in a common currency, law of one price should hold

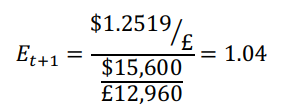

Change in real exchange rate

- Suppose inflation in Australia (UK) over the next year is 4% (8%). Also, the nominal exchange rate changes in line with Relative PPP predictions.

- The £ weakens by 3.7%

- What is the new Real Exchange Rate?

- New price levels are $15,600 (=15,000×1.04) and £12,960 (= £12,960×1.08) in Australia and the UK respectively

- Notice, the real exchange rate has not changed. This is because relative PPP holds. This keeps deviations from absolute PPP constant.

changed relative to PPP

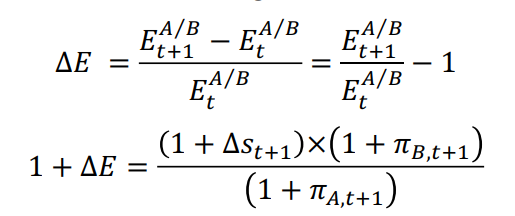

Real exchange rate change

- Real exchange rate, E, can change over time. This is given as

How much has the exchange rate changes from period to period

- derived later slides

- If the % change in E is positive, we have real appreciation of B.

- If the % change in E is negative, we have real depreciation of B.

- What drives real appreciations and

depreciations?

- This is where things get complicated.

- any one of the three variables in the denominator and numerator

Real exchange rates and Profitability

- Real Exchange Rates affect real profitability which is the nominal profits divided by the price level.

- Why is real profitability important?

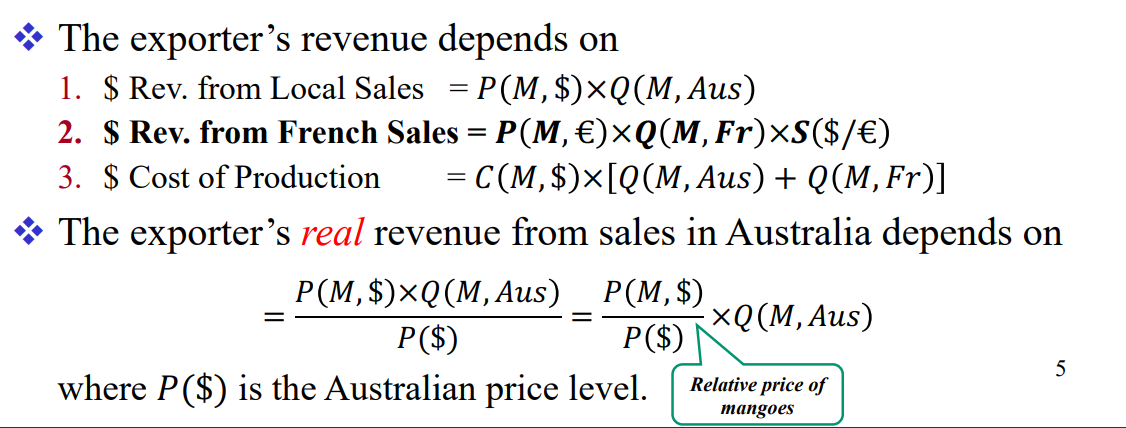

- Consider the case of an Australian exporter of mangoes (M). His costs are incurred in AUD. His nominal profit is given as:

- we care about how much money we can consume

- real interest rates

- relative price of mangoes - how much you can increase the price of mangoes, relative to the interest rate

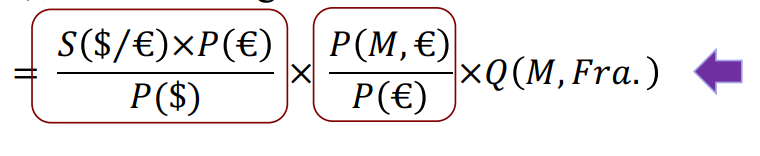

Real Exchange Rates & Profitability (II)

- Real costs for the exporter is given by:

- The real export revenue from sales to France is:

Multiply & divide this real export revenue by the French price level, P(€), and re-arrange

- relative price of mangoes in france

- how much you can change the price relative to the inflation price in france

- The exporter’s real export revenue depends on three factors

- The real exchange rate;

- The relative price of mangoes in France; and

- The quantity of mangoes sold in France

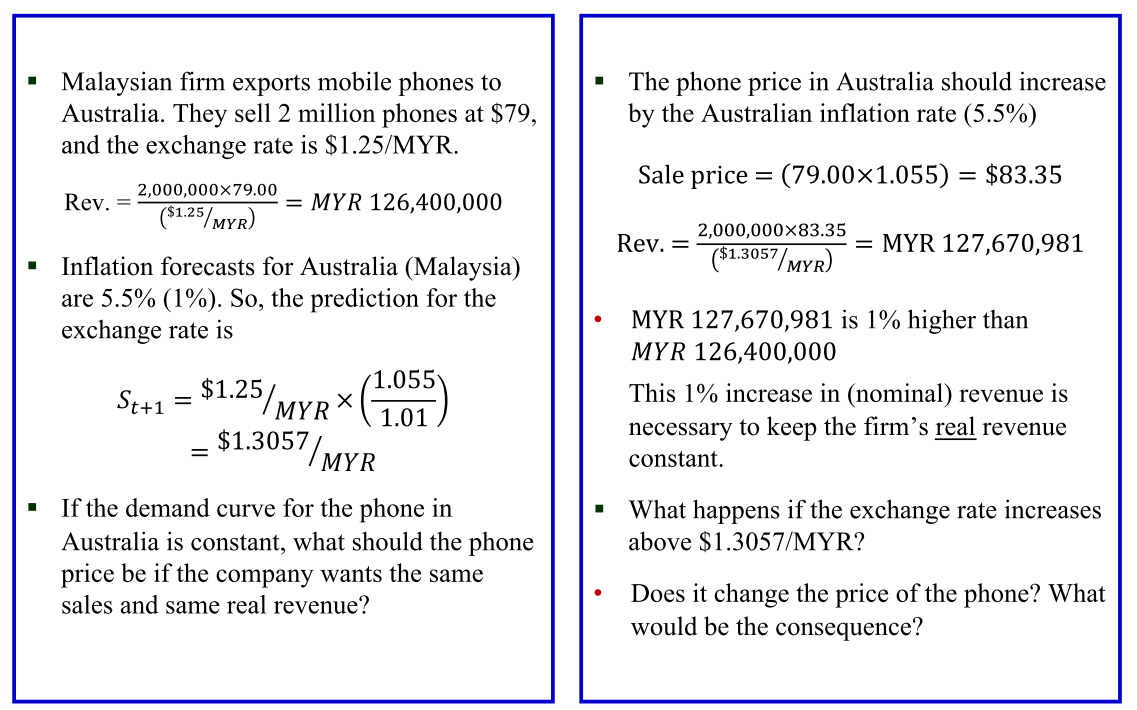

if 1 is constant, will maintain revenue from period to period

- How managers respond to changes in the real exchange rate by altering relative prices is known as exchange rate pass-through.

- Once the relative price is set, the demand curve will determine sales volume

- real revenue kept constant

- has to increase by 1%

how do you respond if the exchange rate increases or decreases down the track?

- how price-sensitive the demand if for changing prices

The Source of Economic Exposure

- Economic exposure arises when the value of the firm is affected by

changes in the Real exchange rate. Exchange rates affect the value of

the firm through their impact on

- Revenues;

- Costs; and

- Competitive position

- It is the extent of sensitivity of the Value of a firm to an unexpected exchange to real exchange rates.

- Note that if a change in the exchange rate merely reflects differential rates of inflation between countries, then relative prices would not change, and the value of the firm would be unaffected

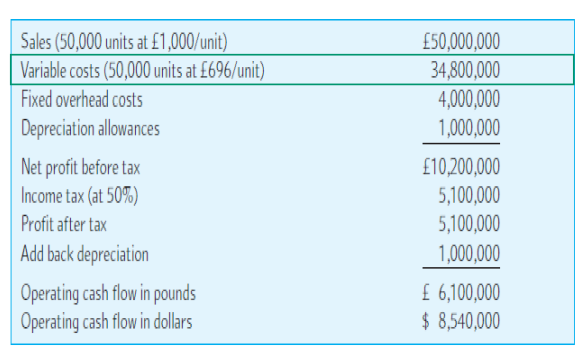

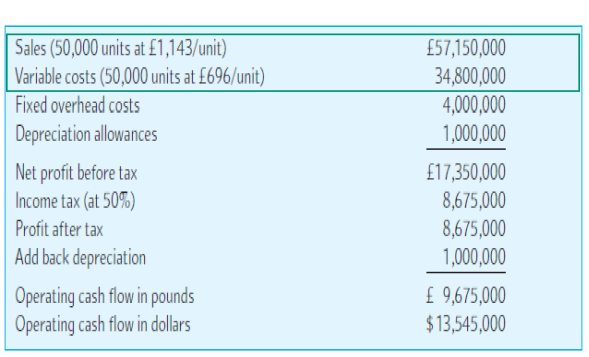

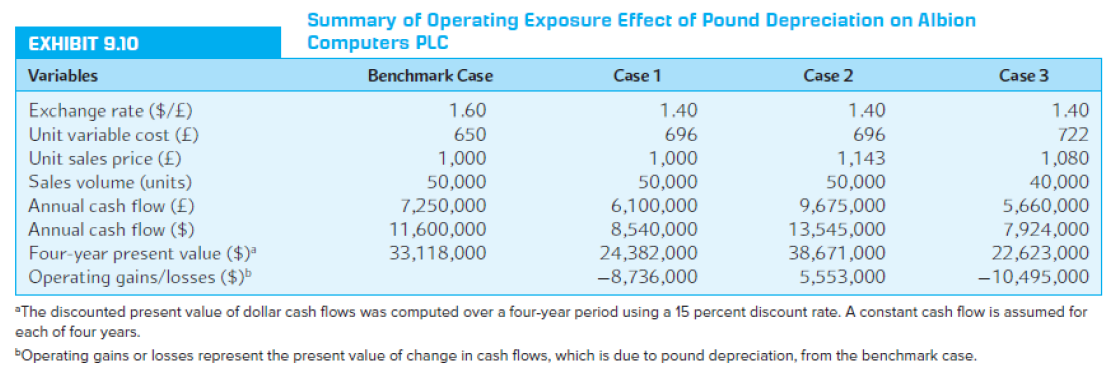

An Example

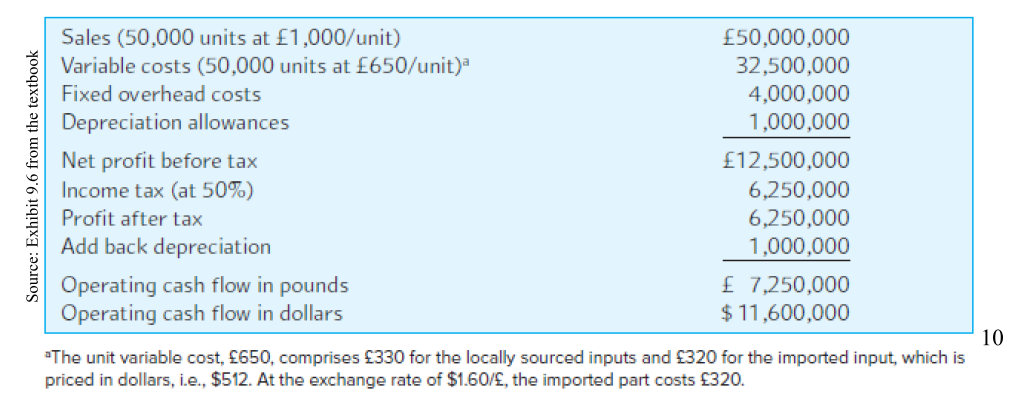

- Albion Computers, a US firm, has a British subsidiary that

manufactures and sells PCs in the UK.

- Main input is Intel processors, priced in dollars ($512/unit).

- All other costs are in British pounds (Fixed cost = £4M and Variable cost = £320/unit).

- = $1.60/£

- Expects to sell 50,000 PCs this year at £1,000 each.

- Tax rate = 50%

| Case 1 | Case 2 | Case 3 |

|---|---|---|

|

|

|

| Assumes only the price of imported input changes. (Albion does not pass-through any of this higher cost. Thus, profit margins fall.) As the £ depreciates ($1.40/ £), the input cost of imported Intel chips increases resulting in lower £ profits, and the £ operating cash flows are worth fewer $s. | Assumes price of imported input AND selling price increase. Assumes Albion will sell the same number of units after passing on all (and then some) of the higher cost. Thus, assumes demand is highly inelastic. | Assumes selling price and local costs increase by 8% (local inflation rate). Also assumes demand is elastic. Sales fall by 10,000 units at the higher selling price. Input costs have gone up, unit sales have fallen, and the £ operating cash flows are worth fewer $s. |

- How sensitive is the demand curve?

- Case 1: Demand elastic. To maintain market share, absorb all cost increases (no pass-through). Profit margins fall.

- Case 2: Demand inelastic, pass-through all cost increases, maintain/improve margins.

- Case 3: Demand elastic, absorb some of cost increase, lose both market share and profit margins.

A Real-World Example: Honda Motors

-

Honda used to manufacture all its automobiles in Japan and ship them to the U.S.

-

U.S. demand declined with yen appreciation

-

In January 1993, exchange rate was about 125 ¥/ range

- ~$11,602

-

NY Times says that Japanese manufacturers would have to “take stern measures to reduce their costs and improve their efficiency.”

-

June 1993 dollar fell to about 110 ¥/$

- ~$11,364

-

End of summer of 1993, 100 ¥/$

- ~$12,500

-

In July 1993, Japanese auto exports were 14% below previous year’s level.

-

The New York Times reported Japanese manufacturers were shifting production to U.S.

-

Honda posted a 55% drop in pre-tax profit for quarter ending June 30, 1993.

-

Honda has built manufacturing plants in the U.S. to produce automobiles for sale there.

-

What are the benefits?

competition, where you source parts, etc. all change operating costs

Impact of Economic Exposure

- A strong dollar can make imports look cheap to Australian purchasers.

- Can bring new competition for Australian producers.

- Exchange rates can affect the price a firm pays for inputs imported from foreign countries.

- Raise prices (lower demand) or earn lower profits?

- Exchange rates can affect the foreign demand for a firm’s product.

- Weak dollar can make Australian exports attractive.

- Increase in foreign demand can also increase Australian prices if production doesn’t adjust fast enough.

- If AUD strengthens against other currencies, US, Euro etc, will bring in competition from other countries

- may not be affected by exchange rate exposure, could definitely be affected by operating exposure

- Honda's costs are in yen and USD.

- exchange rates can affect the price of inputs in foreign countries, i.e. USD parts for Honda

Recognising Economic Exposure

- Where is the company selling? [domestic v. foreign]

- Who are the key competitors? [domestic v. foreign]

- How sensitive is demand to price?

- Where is the company producing? [domestic v. foreign]

- Where are the company’s inputs coming from? [domestic v. foreign]

- How are the company’s inputs or outputs priced? [world price v. domestic market]

- if inelastic, then you could increase the price without a huge impact to demand

- Car companies introduce luxury car brands, inelastic prices

Impact of Exposure can be DIRECT or INDIRECT

| Particulars | HC Strengthens | HC weakens |

|---|---|---|

| Direct Exposure | ||

| Sales abroad | Unfavourable | Favourable |

| Source abroad | Favourable | Unfavourable |

| Profits abroad | Unfavourable | Favourable |

| Indirect Exposure | ||

| Competitor sources abroad | Unfavourable | Favourable |

| Supplier sources abroad | Favourable | Unfavourable |

- suppliers sourced from abroad - savings passed on to company

Managing Economic exposure

- Use of Marketing Strategies

- Market Selection

- Pricing Strategy/Product strategy

-

Can I increase the relative prices of my goods? (relative to inflation)

-

Product strategy, have a luxury line which is less price sensitive, e.g.

- Promotional Strategy

-

Market abroad when AUD declined

- Pricing-to-Market

-

target the market based on what the market can afford

- Use of Production Management

- Input mix

- Plant Location & Shifting production among plants

- Raising Productivity (i.e., lowering costs)

- Financial Hedging techniques may also be used, but …

- Example is Porsche’s use of derivative contracts

Can you shift my inputs to another country to take advantage of higher value?

- shifting suppliers may be difficult, may have signed long term contracts

Plant location

- shift production where it is cheaper to manufacture

- have a diversified Plant location

Financial Hedging techniques

- Doesn't matter using MM techniques or hedging contracts, same outcome

- Does not work here, different exposure condition

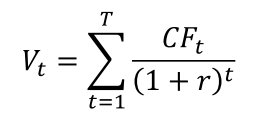

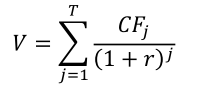

Quantifying Economic Exposure

- PV of firms profits/CFs is given as

- It measures the marginal impact on firm value by an unexpected change in the

(AUD/FC) real exchange rate.

- This can also be written as

- Audits/Scenario Analysis: Qualitative examination of the separate elements of a firm’s operating cash flow and anticipating its sensitivity to real exchange rate changes.

- Regression Analysis:

where, 𝑟4! and 𝑟5! are the return on the market index and return the % change in the exchange rate (change is the AUD per unit of foreign currency) resp.

does not look at cash flows, but rather exchange rate changes

- Whether the beta is significant or not

Natural Hedges

- Ford shifting production to Asia

- Toyota has insulated itself to some extent against dollar fluctuations

- It builds 60% of the cars sold in North America in North America

- Michelin, the world’s largest tire maker, has 40% of its annual sales in

North America.

- Most of the imported raw materials used by Michelin are also priced in dollars