Lecture 7: Cost of Capital & Political Risk

-

Cost of capital can be defined as the MINIMUM rate of return a firm has to pay in order to entice investors to buy and hold its securities.

- Given by WACC – weighted average of the financing costs

-

Question: Should the cost of capital of foreign projects be higher or lower than that of domestic investment?

-

If all capital markets are fully integrated, securities of comparable expected return and risk should have the same required rate of return in each national market after adjusting for foreign exchange and political risks.

In asset pricing terms, two identical assets must have the same return on terms of HC

E.g. BHP

Quoted in US and AUD depending on the market

- Require rate of return has to be the same because the assets are identical

Implications:

- Cost of Equity Capital : use CAPM

- risk free rate, premium and beta

- A national capital market is segmented if the required rate of return on securities in that market differs from that for securities of comparable expected return traded on other national securities markets (e.g., New York and London).

Most countries have restrictions on who can buy and hold currency

- If you are going to investing in those stocks, how do you calculate the Cost of Capital (appropriate discount rate)

Causes of Segmentation

- Market segmentation is a financial market imperfection caused by government constraints and investor perceptions.

- The most important imperfections are:

- Information Barriers – Lack of transparency & information disclosure

- Market illiquidity

- Transaction Costs

- Regulatory Barriers/Capital Controls

- Foreign Exchange Risk

- Country Risk (and Political Risk)

Tends to be time variant

- periods segmented and integrated

Developing countries

- Are in integrated markets

- How to estimate the CC

Frictions:

- market segmentation is a financial market imperfection; taxes, information barriers, weak enforcement standards

- Some are quantifiable. Personnel management, etc. are not

- judiciary that is highly biased. These decisions have an effect on investment prospects

- Rules on who can buy/hold

Information Production is no Accident

- US Disclosure Laws :Securities Act of 1933, Reporting Act of 1934

- Mandate quarterly and annual filings of all public firms

- The rules are well-understood standards (GAAP) that are audited and certified

- The rules are enforced with rigor by the US government (SEC)

- Information production results from a deliberate effort to establish:

- Laws

- Institutions – In common law countries, we take this for granted. However, in many countries the view is that the “secrecy” of corporate information is more important than the dissemination of information to the investor.

Important that

- laws are changed in a very timely manner key act in 1933, need at least 5 years of financials for publicly listed companies

- every three months have to file a 10Q

Announcements on ASX:

- Red texts means pricing impact

Conference calls live

- When release quarterly earnings, can listen to managers company-wide

Regulation fair disclosure:

- Have to relay information to all parties within 24 hours

Accounting Disclosure Index

Market liquidity

- Market Liquidity is the degree to which a firm can issue a new security without depressing the existing market price, as well as the degree to which a change in price of its securities elicits a substantial order flow.

- A firm can tap capital market for only some limited amount in short run before suppliers of capital balk at providing further funds.

- In the multinational case, a firm can improve market liquidity:

- By raising funds in the Euromarkets (money, bond, and equity)

- By directed security issues in individual national capital markets, and

- By tapping local capital markets through foreign affiliates.

Multinational effect is slightly different

- e.g BHP in segmented market, most investors already own BHP stock

- If BHP want to raise another 10M funds, might be difficult to raise funds as investors have enough in their portfolios

- Investors will purchase if the price is low enough

- best strategy would be to tap into other markets - listing on foreign markets, issuing bonds in foreign markets, etc.

Share turnover

- trading volume / average shares outstanding

- Some stocks are more illquid than others - as a company you want to be operating in liquid markets

- want to enter and exit the stock freely - liquidity measures the ease of purchasing in a particular market

- illiquid stock - berkshire hathaway

Transaction Costs

- How much does it cost to buy or sell securities?

- Why is this important to know?

- Transactions costs can wipe out trading profits, so ignoring them lead to incorrect asset allocation strategies.

- Price impact in emerging markets, a.k.a. “hot money”, can destabilize markets.

- Large costs in foreign markets can lead firms to list their stock in the U.S. or other developed markets, further hindering domestic market development.

- How large are transaction costs globally?

- Difficult to estimate, but there is some research on this.

Market impact on investors decisions to buy, hold or sell.

- Bid-ask spread of small stock a lot greater than large companies like BHP

- High transaction costs means unattractive to invest in market

E.g. 50,00 shares of BHP

- as order hits market, price can potentially change.

- market impact, price change when submitting an order

Equity Trading Costs

How do we quantify transaction costs?

- Difficult to quantify, survey market participants on market transaction costs

Why worry about Transaction Costs?

- Study by Domowitz, Glen & Madhavan (2001)

- Very Important to Returns: The equally-weighted portfolio of all countries has one-way trading costs of 71.3 bps * .

- If this portfolio is turned over every six months, annual costs of 2×2×71.3 = 285 bps are incurred.

- By contrast, the average annual portfolio return (pre-cost) is 12.28%.

- Trading costs constitute 23 percent of raw returns in this scenario!

Consider an equally-weighted portfolio

- one-way trading costs from all stocks in the index, cost 71.3 bps.

- If I turned this portfolio twice in a year, it would cost ~285bps

As an investor, need to minimise investment costs as much as possible

- going to impact on investors, need to be in a country where transaction costs are low

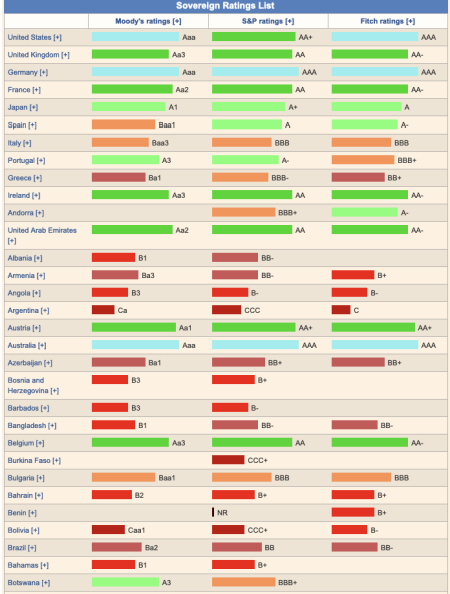

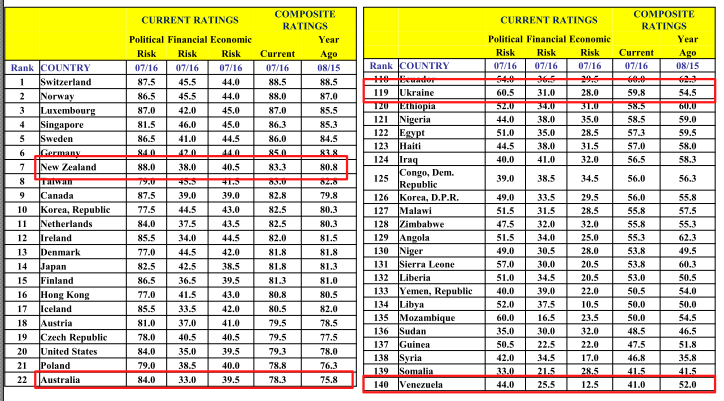

Measuring Country Risk

- Difficult to define and therefore to measure

- Incorporates political stability and economic measures, capital flight, a country’s resource base and privatization measures, sovereign rating etc. Long run economic health is a good indicator.

Australian company like country road

- costs can be affected by recessions, e.g. in Vietnam

- Can effect companies differently

- importer vs exporter, recession can eat into revenues

How do we measure country risk? Two aspects

- ability to pay: economic factors in the country

- willingness to pay: economic leanings of political party

Crude test - Soverign ratings

Use sovereign ratings to calculate COC

Taxes

-

Governments can alter the rules that were in place when the MNCs made their investment.

- E.g., Increase in QLD coal royalty rates in June 2022.

-

Differential taxation rates for foreign investors (e.g., dividend withholding tax in many countries). E.g., Dividend withholding taxes on non-resident investors in Australia is

- 10% for interest payments

- 30% for unfranked dividends & royalty payments.

Risks that investors face

- Withholding tax on dividends; franked dividends Does the presence of a scheme have an impact on the Cost of Capital

What about capital controls?

- Various foreign exchange controls are often imposed, especially in Emerging Markets.

- Some countries have special classes of shares for foreigners (e.g., China, Mexico, Philippines)

- Some allow only “authorized foreign investors” to trade in their markets (e.g., India, Taiwan).

- Different classes of shares and their pricing: shares for foreign investors may sell at a discount or premium to domestic shares.

- Repatriation restrictions (e.g., Chile, Malaysia) and the prevention of conversion from local currency into foreign currency.

Can't raise as much capital on Positive NPV Cost of issuing shares and go public - 80% of earnings is lost in transaction costs

lose positive NPV projects

Lack of liquidity, poor accounting regulations

Countries tend to impose profits earned abroad back into home countries

- Foreign countries repatriate profits going into own countries

- In times of currency attacks (recessions) costs tend to bite

- E.g. to maintain fixed exchange rate, increase repatriation restrictions

- Switzerland - in 1980s have two different types of shares, one for local and foreigners

- China has Alien and non-alien shares

- India, have to be a qualified investor

- Has an impact on the prices investors are willing to pay

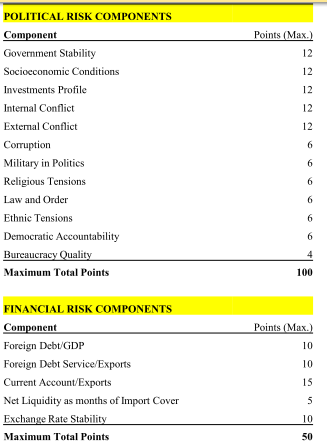

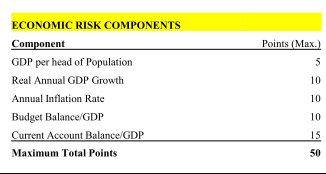

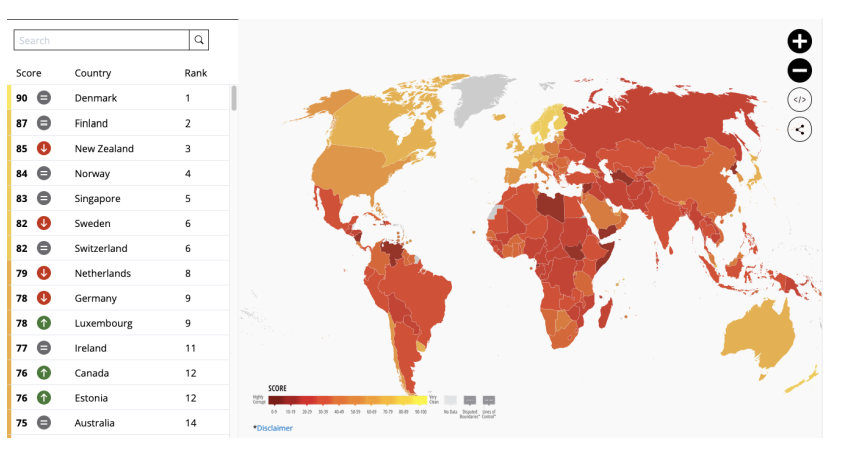

ICRG Country Risk Components

- International country risk guide

- Religious tensions, law and order, corruption

- Quality of the bureaucracy

- able to pay off foreign debts;

- Corruption

Measuring Country Risk

- Data comes out every financial month

- Ukraine 2016, one of the most corrupt countries, still risky to invest in now

Corruption

- Illegitimate payments and favors outside the rule of law

- Corruption occurs to some extent in all countries, but large differences across countries exist

"There is no end in sight to the misuse of power by those in public office - and corruption levels are perceived to be as high as ever in both the developed and developing worlds" - Peter Eigen, Chairman of Transparency International, speaking at the launch of the Corruption Perceptions Index.

Political Risk

Political Risk

- Political Risk can be described the influence of non-business events on the value of the firm.

- It is more than Expropriation. Can also be

- currency or trade controls

- changes in tax or labour laws

- changes in ownership policies

- Political problems etc.

- Political Risk can be decomposed into:

- Macro Risk which affects all firms

- Expropriation (See slide on Russian Oligarchs; Argentina)

- Ethnic Strife (Balkans, Rwanda, Russia/Ukraine etc.)

- Micro Risk which affects specific firms or industries

- Macro Risk which affects all firms

Expropriation - within its rights to seize the assets of other

- seizing of assets of russian oligarchs when they invaded ukraine

Resource company - political risk is much higher than manufacturing in a foreign country

- South Africa, Chile

- political risk tends not to manifest normally, obvious in recessions

- Expropriation is defined as official government seizure of private property.

- It is recognized by international law as the right of any sovereign state, provided the expropriated owners are given:

- prompt compensation

- at fair market value

- in convertible currencies.

- It is recognized by international law as the right of any sovereign state, provided the expropriated owners are given:

- Problems with Expropriation Conditions:

- Promptness is usually delayed by extensive negotiations and appeals

- Fair market value is in the eyes of the beholder

- Compensation in convertible currencies is usually difficult.

Suffering due to actions, probably cannot pay in local companies

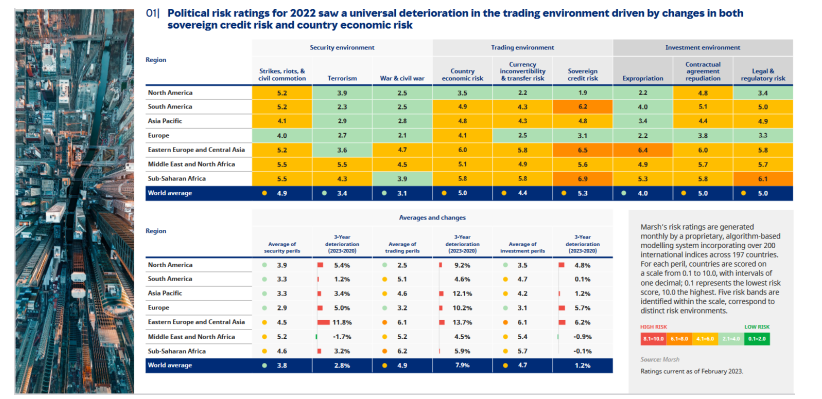

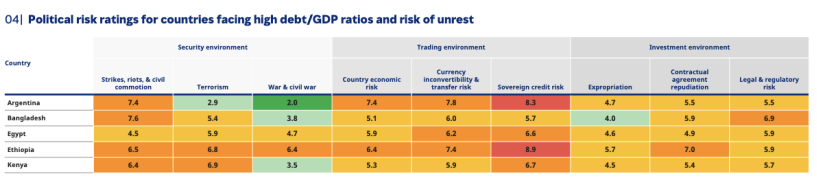

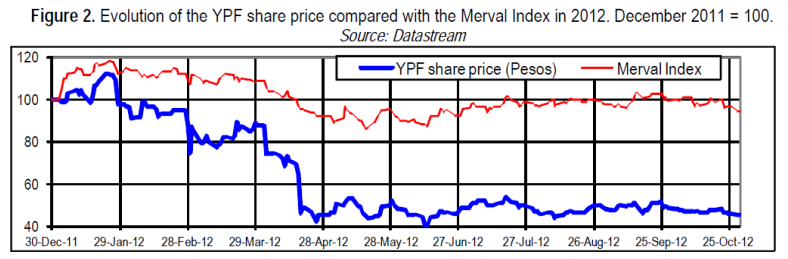

Political Risk 2022-2023

Argentina’s expropriation of Repsol’s YPF stake anticipated by country risk experts

- The push to re-nationalize YPF represents one of the more dramatic shocks to confront foreign investors.

- In the comedy of economic errors that has blighted Argentina under president Cristina Fernández de Kirchner’s administration, Monday’s push to re-nationalize YPF, the country’s biggest oil company – expelling Spain’s Repsol as majority shareholder – represents one of the more dramatic shocks that has confronted foreign investors in recent years…

Hedging Political Risk

- Take conservative approach:

- Adjust NPV for political risk.

- Political risk may be diversifiable to some extent.

- Don’t put all your eggs in one basket.

- Minimize exposure to political risk:

- Joint Venture

- Consortium of international companies

- Use local debt

- Purchase insurance:

- Private insurance (Lloyd’s of London, AIG)

- Government export credit agencies (OPIC in the US and EFIC in Australia)

Adopt a join venture If you wish to participate in operations in China, you are require to take on with a partner

- Take on a loan, local investors connected with government can make process smoother

Why Should We Care About Barriers?

- If investment barriers are severe in a country, it will lead to that country’s capital market being segmented (i.e., not integrated with the global capital market)

- This will affect investors because it restricts their opportunities to diversify.

- This will affect firms because it will keep their cost of capital higher relative to an integrated market.

- The issues with integration are:

- How to quantify it?

- Is it time-varying?

What these types of barriers are to have with the underlying firm

- Times are not so well, tensions are rising

- What impact is this likely to have on companies?

Estimating the Cost of Capital

- The Weighted Average Cost of Capital/Discount Rate/Hurdle

Rate

- The opportunity cost of investing capital in projects of similar risk and duration

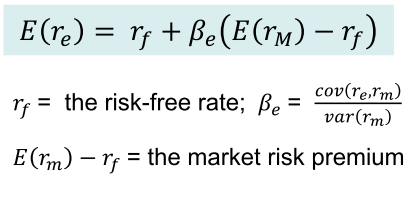

- The Cost of Equity given by the CAPM

- The predictions of CAPM:

- All investors hold the same portfolio of assets (i.e., market portfolio);

- Risk premium on the market depends on the average risk aversion ( 𝐴 ) of all market participants i.e.

- Risk premium for the individual security is a function of its covariance with the market portfolio

- To estimate the CAPM:

- We need data on returns on equity, return on the market portfolio and interest rate on risk-free asset

- Obtain an estimate of

- Determine the market risk premium

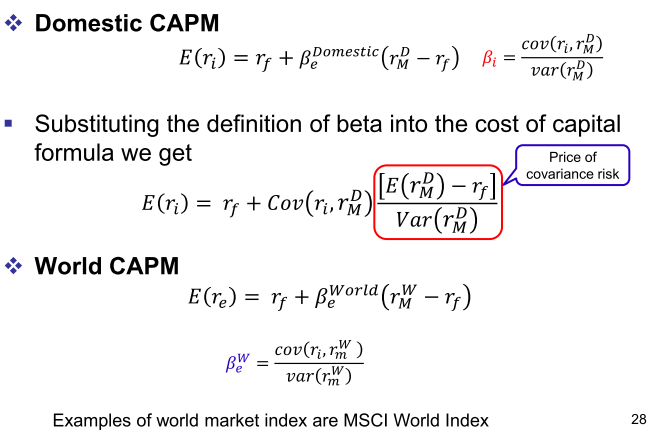

Operating on integrated market

- international portfolio

Estimates of beta on equity

- If segmented; estimate beta relative to domestic market

- If integrated, estimate beta relative to world index

CAPM - various models

Domestic:

- Estimate market risk premium relative to local market index

- estimate beta relative to local market portfolio

Applying the CAPM

- From the capital raising firms’ point of view, the cost of

capital should be lower due to globalization. Why?

- As investors become better diversified, they require a smaller risk premium for capital.

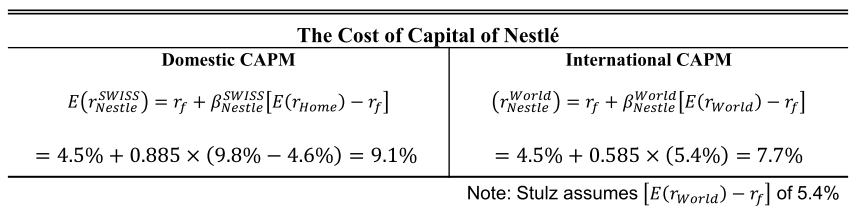

- Stulz (1995) determines the cost of (equity) capital for Nestlé.*

- Which market portfolio? The options are the Swiss Market Index or the World Market Index

Integration:

- Go from segmented to integrated market

- Can diversify in local market

- Unable to diversify in local economy

- Can share that risk with local investors,

Beta estimated with world market index

- As an investor, want to work in an integrated market

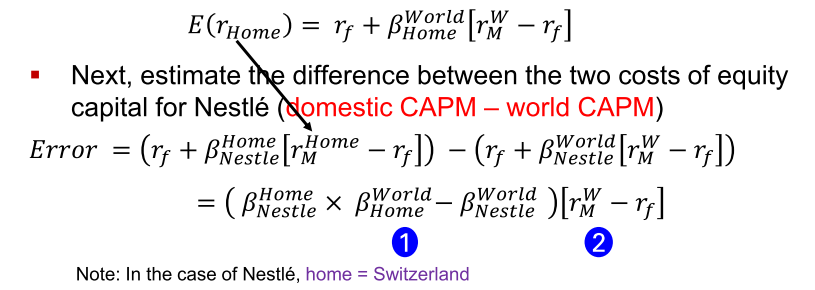

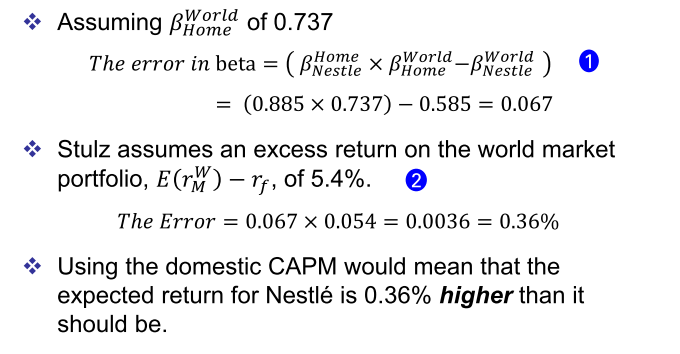

Getting the Benchmark Wrong

- Suppose the “true” cost of capital is estimated relative to the “world” market index: 7.7%

- Instead, I use the “domestic” cost of capital to estimate Nestlé’s cost of capital: 9.1%

- How large is the error likely to be?

- First, estimate expected return of the home market (i.e., Swiss market) on the World market portfolio.

- Next, estimate the difference between the two costs of equity capital for Nestlé (domestic CAPM – world CAPM)