Lecture 8: International Capital Budgeting

Issues

- How do we decide whether a firm should proceed with foreign project(s)?

- In what way international capital budgeting differ from the domestic setting?

- What role does the exchange rate play?

- What are the complications with estimating the cost of capital for a foreign project?

How much cash flows is going to add to the underlying cash flows of the firm?

- What is the appropriate discount rate

- Apply Capital budgeting techniques, IRR, NPV etc.

- Have to take into account complications, COC, and tax related issues and political risk, etc.

Net present Value

- The NPV is the present value of future cash flows discounted at an appropriate rate minus the initial net cash outlay for the project.

- In mathematical terms, the formula for net present value is:

- Projects with a positive NPV should be accepted; negative NPV projects should be rejected.

- The discount rate is the expected rate of return on projects of similar risk.

Rules of thumb to use what approach

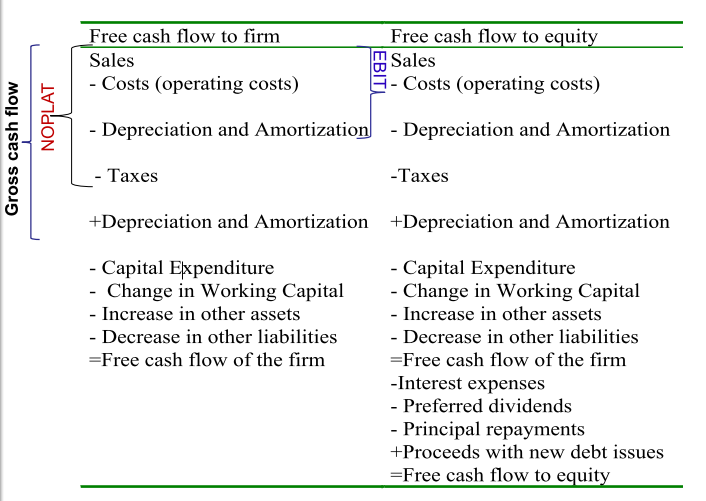

Free Cash Flow Definitions

Figure out the incremental cash flows of the business

- How much would taking a particular project add to the company

Two ways of looking at FCF

- To the business

- To Equity (equity holders)

FCF firm

- FCF to firm can be paid out to all claimants of the firm. Can be used in NPV of the firm

FCF Equity

- Preferred shareholders receive dividends before ordinary shareholders

- Discount with cost of Equity capital

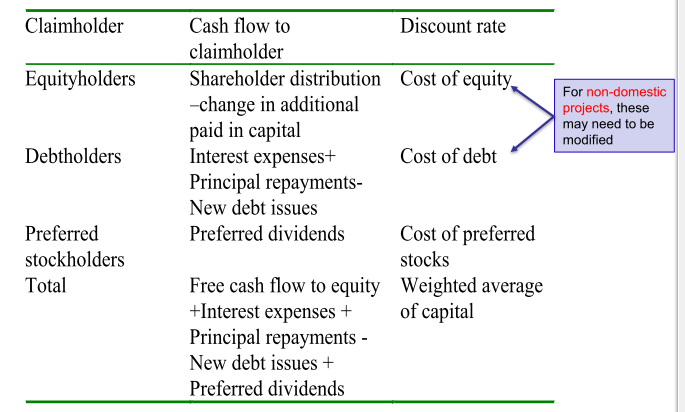

Cash flows to Claimholders

Issue:

- Use COC, you have domestic and non-domestic projects, How do you adjust the COC

Adjusted Present Value

- An alternative valuation method is

- It is a series of present value calculations

As a standalone decision, is this a good project

- Set aside all other complications that arise

- Taking on debt, can be used as a tax shield - MM Proposition 2

Other imperfections

- other frictions that exist when borrowing money, cannot make principle payments. Assets of the company can be seized, and the costs must be subtracted out

- Information symmetry, agency problems

Stage 1: Project is 100% Equity Financed

Cash-flows: Need Free Cash Flows.

- You need the rate that would be appropriate to discount

the firm’s cash flows as if the firm/project were 100%

equity financed.

- This rate, 𝑟𝐴 , is the expected return on equity if the firm

were 100% equity financed.

- To determine the return on assets ( 𝑟𝐴 ), you need to:

- Find comparables, i.e., publicly traded firms in same business.

- Estimate their expected return on equity if they were 100% equity financed by unlevering.

- This rate, 𝑟𝐴 , is the expected return on equity if the firm

were 100% equity financed.

Appropriate discount rate is the return on assets. Should be equal to the return on equity

- Find the interest rate - Find comparable firms list on the stock exchange

- From comparable firms, find their Cost of equity (determine their unlevered COC)

- Then use to determine Value of firm

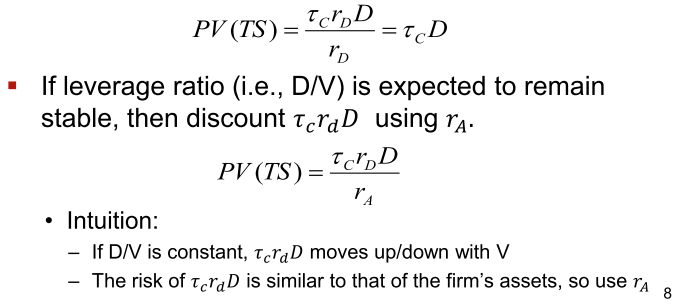

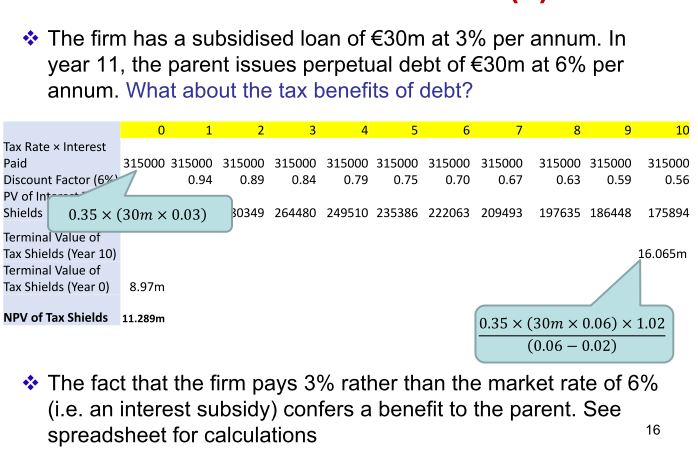

Stage 2: PV of Tax Shields

- The expected tax saving is where is the corporate tax rate

- D is the amount of borrowing is expected to remain stable

Present value of cash flows, discount by COE

Stage 3: PV of Other “Imperfections”

- PV of Distress Costs

- These arise when firms take on debt

- Direct costs of financial distress

- Indirect costs of financial distress

- They tend to be difficult to estimate

- Usually ignored.

- The Costs of Issuing Securities

- PV of Subsidised Financing

Companies in financial distress have difficulty hiring people

- Other problems covered in corporate finance

- Transactions costs involved

- Cost of issuing securities. Roughly 8% of capital raised goes to investment bank because of processing the asset

Parent vs Subsidiary Cash flows

- Whose perspective should the analysis take?

- Substantial difference between the parent vs subsidiary (project) cash flows

- Royalty payments

- Licensing agreements

- Overhead management fees

- The purchase of inputs from the parent

- The role of taxation and exchange controls

- The effect of exchange rates.

- Substantial difference between the parent vs subsidiary (project) cash flows

Investing in a project outside Australian borders

- Costs that the subsidary incurs include management fees, royalty payments, overhead management fees, etc.

- cash flows can be different for subsidiary vs parent company

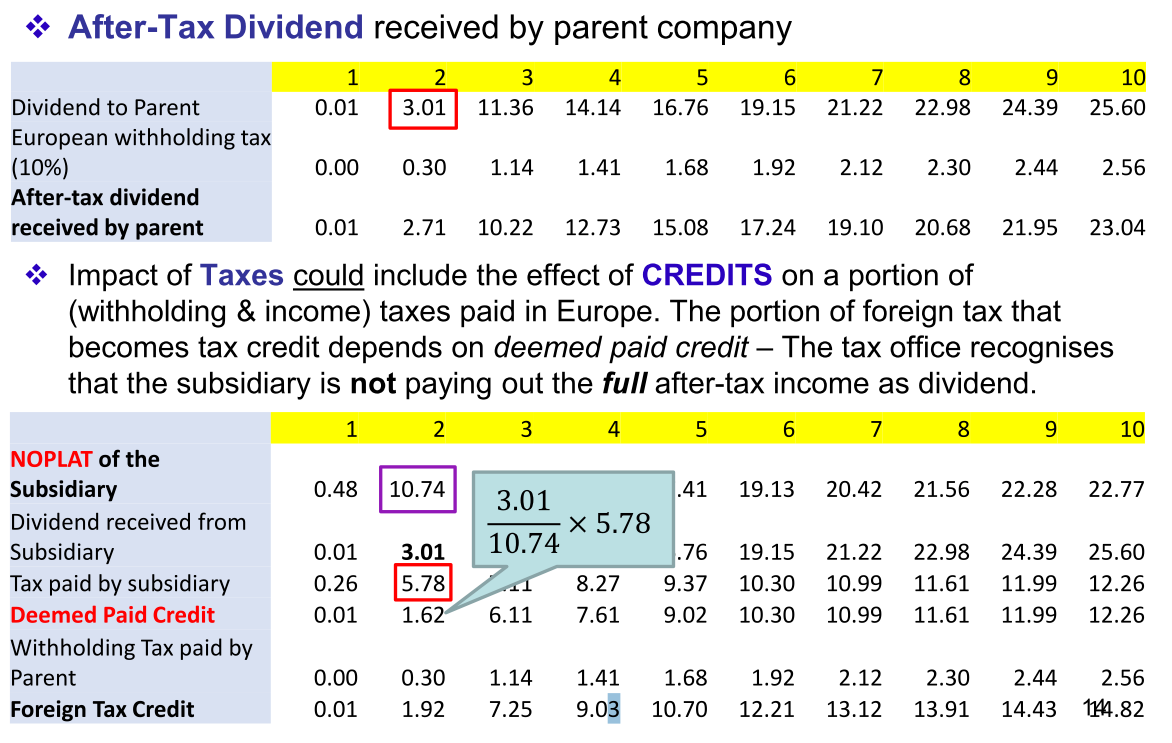

- tax is different, tax credit for parent company.

- Need to consider exchange rates in the future

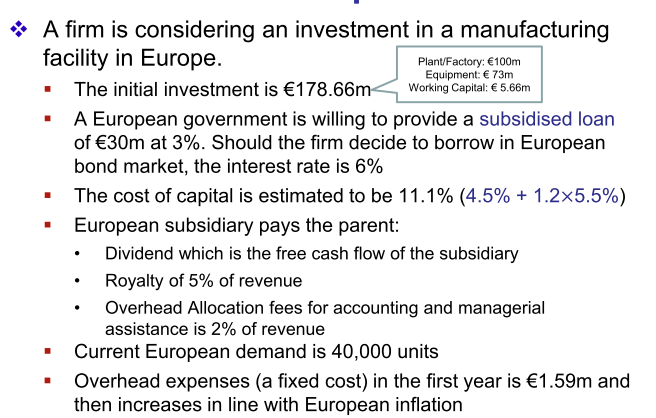

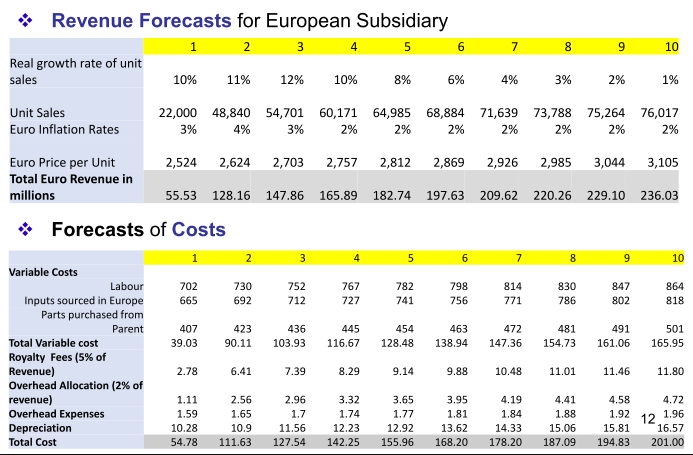

Example

Need to do from subsidiary perspective first

- 5% of revenue is a royalty

- Overhead allocation fees is 2% - cost to the subsidiary

Cash flows of a parent

Dividend to the parent

- Pay taxes in the foreign country before paying

Series of PV calculations

- Selling inputs to subsidiary, is a revenue to the parent company

If you are going to default, risk of default is going to be the market rate

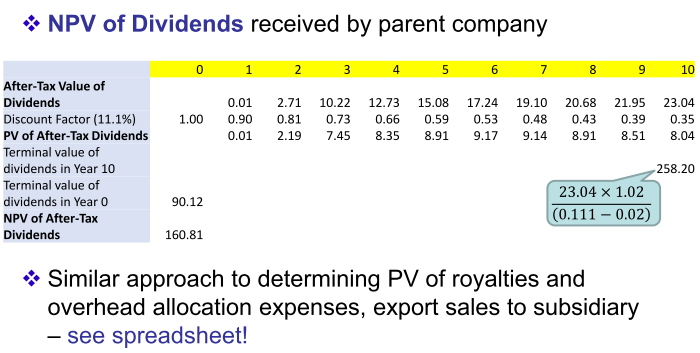

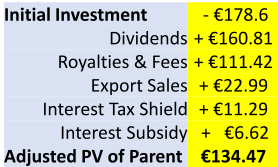

APV of Parent

- The APV from the parent company’s point-of-view is the sum of the present value of cash flows and the impact of side- effects.

- What other issues could be included?

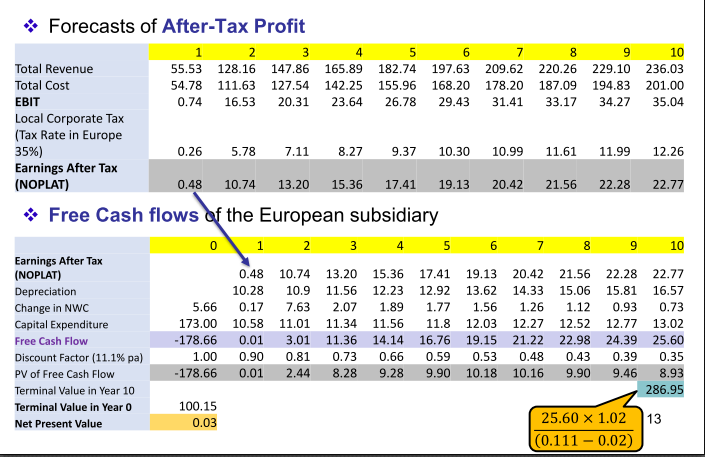

- Cannibalisation of export sales: Setting up manufacturing facilities in Europe reduces parent’s CFs. It reduces exports from parent company if it doesn’t have another market for those 40K in lost sales. This should reduce APV by the amount of the lost profit (€81.55). See worksheet.

How do you factor the cannibalisation of sales?

- needs to be taken into account

Ultimately

- need to test the NPV from both the subsidiary and parent company's perspective

- Parent company's perspective that is going to dominate

- Political risk, tax related issues, exchange rates

What about exchange rates?

-

Firms have revenues and costs in multiple currencies.

-

First Approach: Local Currency NPV

- Perform revenue and cost projections using local currency figures and then discount cash flows at the local currency cost of capital. Then convert local currency NPV to dollars (home currency) using current spot rate

- Denoted as

- This approach is useful when revenues and costs are in local currency, when investment capital is raised locally, and cash flow will be reinvested locally.

- Upside: Don’t have to forecast exchange rates.

Use this when all revenues and costs are in local currency

- not going to be repatriating funds to local currency

- Use prevailing exchange rate

- Second Approach: Period-by-Period Conversion

- Use local currency projections and convert each periods cash flow into dollars using the forward rate or exchange rate projections.

- Discount the dollar cash flows with a dollar (or home country) discount rate with adjustments for country and project risks.

- Explicit about exchange rate movements and discount rate adjustments.

- Easier to perform sensitivity analysis.

Explicitly taking into account the exchange rate movements

- Advantageous if doing sensitivity analysis, what economic exposure is going to have - don't expect parity conditions to hold in 5 years e.g.

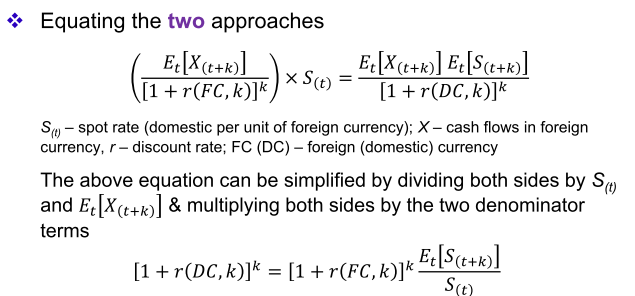

- The two approaches are the same when the discount rates satisfy International Fisher Effect.

- Keep in mind: Discount rates should be different for different time periods.

Dividing both sides by the spot exchange rate

- Multiply both sides by the denominator terms Two approaches are essentially the same

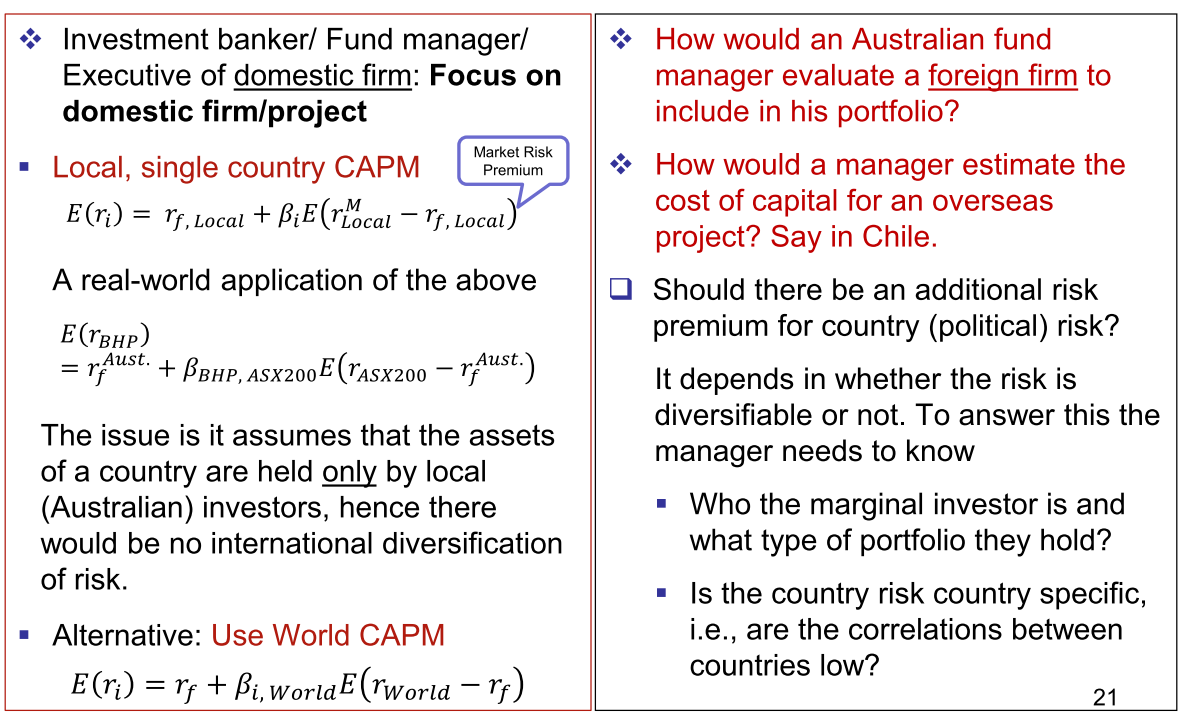

Discount Rate: Horses for Courses

Australia's market more integrated in the rest of the world

- Can build a well-diversified portfolio in Australian market

Invest in highly risky projects, risk premium goes up

- company risk - will depend on how it will add to the overall market portfolio

- How much it will cost to buy the stock, over and above the market premium

Use world CAPM for countries that are well diversified into the world market

Other issues:

- Aus company investing in overseas project

- How do you calculate the market risk premium?

- Higher royalty fees on copper, risk of appropriation (political risk) etc. How do you make adjustments to the premium?

- Is the risk of purchasing assets of the company diversified?

- If non-diversifiable, have to make adjustments to the risk premium

- Are investors marginal (trade)

- Do we need to add a country specific risk?

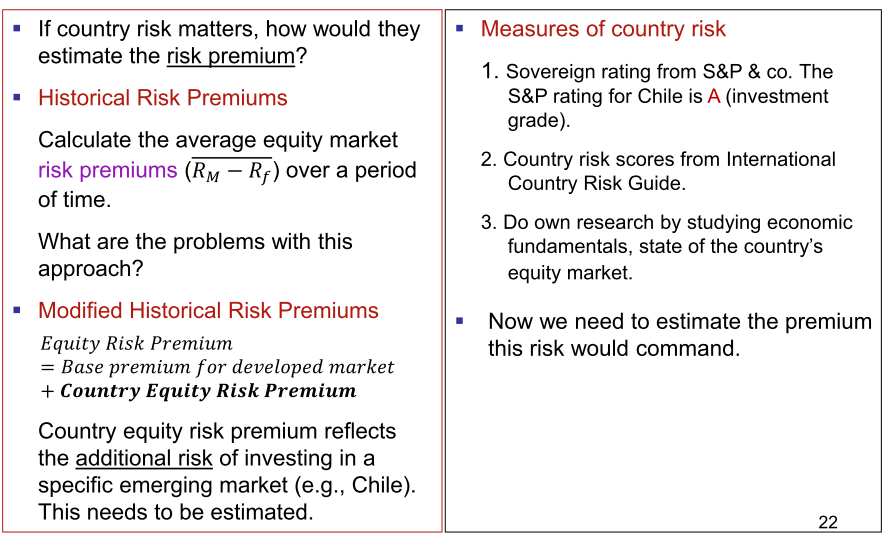

Country Risk

Determine the market risk premium

- Premium over and above the risk free rate

- Calculate the risk premium

- Investing in a project and need to make adjustments for the risk premium:

- Use a risk premium of a developed market + additional risk from the country

- Balance of payments numbers, political risk of a country, etc.

- Country ratings

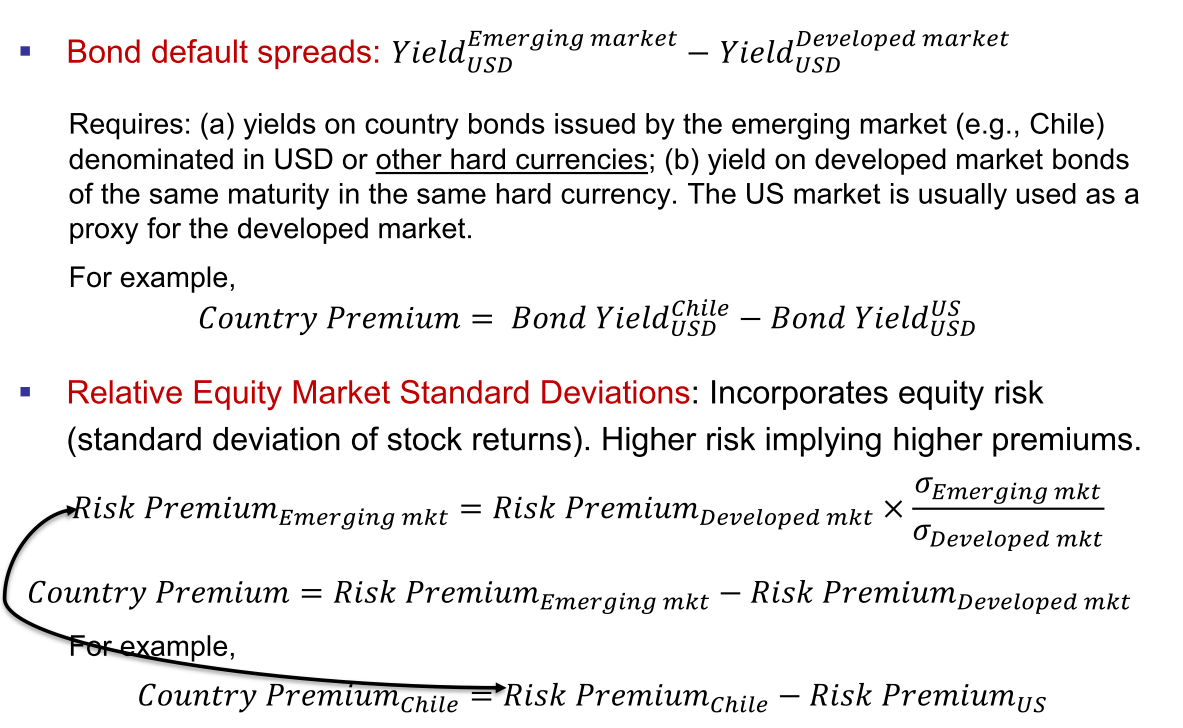

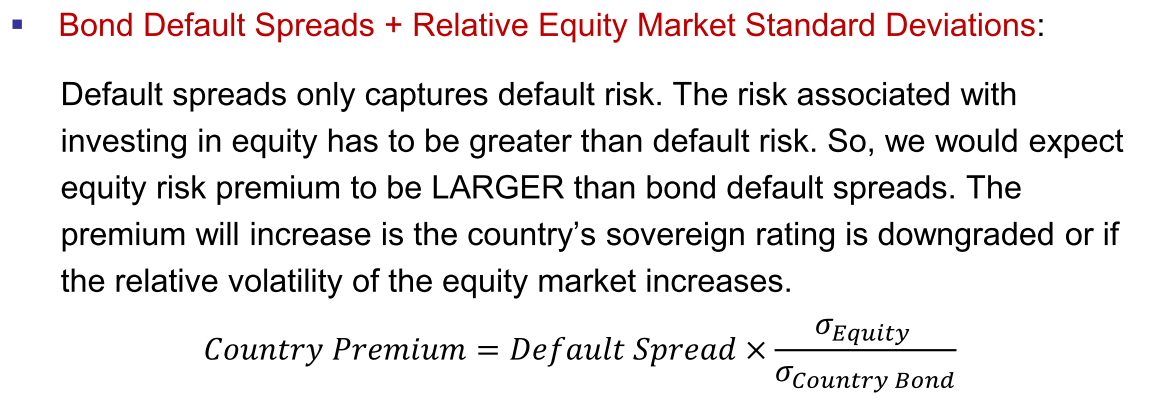

Measures of Country Risk Spreads

- Look at the yield spread between the developed country and country of emerging market.

Issue: looks at, when we are trying to determine the returns on equity instruments

Relative Equity Market Standard Deviations

- Calculate stock returns of the developed markets and incorporate standard deviations of emerging market

Really hard to get bond returns data

- Generally harder to estimate

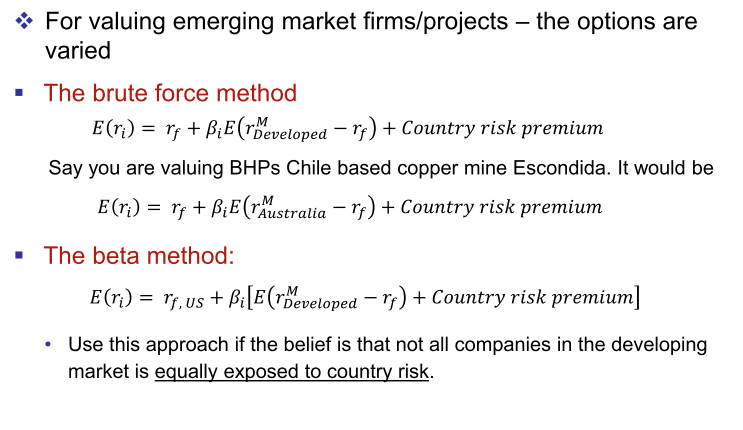

Estimating the cost of capital

Different ways of calculating the emerging market premium

- Depending on which approach, add on the country risk premium

Beta method

- Calculate the risk premium, calculate the risk premium of the developed market plus adding the risk premium

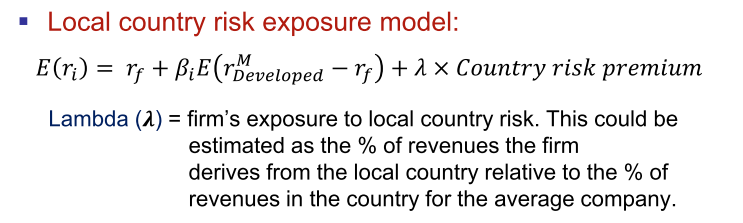

- Use this in countries with extractive industries. When there is political risk (differing exposure) then add the country risk to the beta

Estimate lambda - sales you estimate from the local currency

Takeaways

- Have to take into account cost of exchange rate

- How to calculate the discount rate in an emerging country

- depends on whether a company's risk is diversifed or not.

Not in textbook - don't observe the COC, needs to be estimated