Lecture 9 : International Corporate Governance

minimise conflicts between various stakeholders

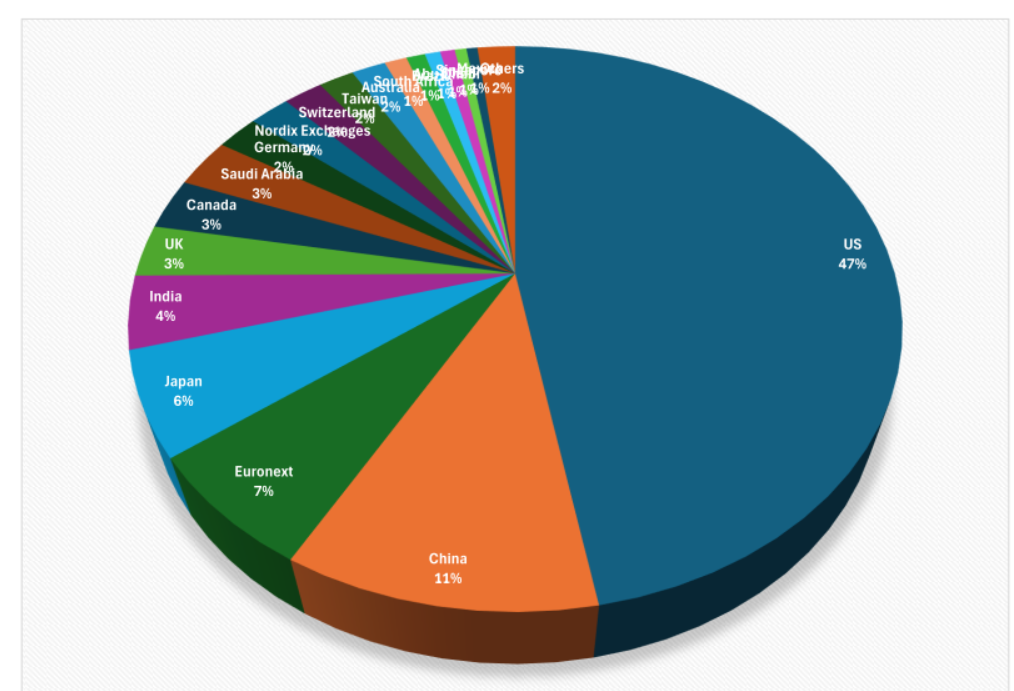

World Market Capitalisation

Why are some countries able to grow why others don't? Can corporate governance be the explanation for the growth of world market capitalisation

Some Questions

- Why do some countries have so much bigger capital markets than others?

- Why do hundreds of companies go public in the United States/Asia every year, while only a few dozen went public in Europe over a decade?

- In 2023, 56 (236) new domestic firms were listed in the US (China) via IPO; 62 (0) new foreign firms listed on US exchanges (China)

- It was around 80 domestic listing across Europe

- Why is share ownership of large companies so dispersed in the US and UK and concentrated in other markets?

Separation of Ownership and Control

- Who owns companies? Owners/Investors

- Who runs companies? Managers

- When ownership and control of corporations are

not aligned there is potential for conflicts of

interest between owners and managers.

- Are managers using company funds for the right purposes?

- Are they investing in positive NPV projects?

- Are they spending too much money on themselves?

- Are they stealing?

When there is separation between ownership and control, gives rise to range of issues

- Objective is to minimise the loss in value when separating between ownership and control

- Are executive using too much money?

- Overconfident in their abilities to turn things around

- Invest in negative NPV projects to increase size of the company and increase payout

External methods to discipline markets

- M&A - market for corporate control

Traditional Finance

- Modigliani and Miller (1958) distinguish debt and equity by the difference in the types of claims to cash flows.

- However, another defining feature of a security is the RIGHTS it brings to its owners

- What rights do shareholders (the firm’s owners) typically have?

- What rights are bondholders (the firm’s creditors) entitled to?

- What is relationship between managers and owners that make this view important?

Debt and equity holders entitled to certain cash flows

- shareholders and bondholders have various rights of business

Agency costs of debt and equity

Shareholder & Creditor Rights

- The RIGHTS attached to securities become important when managers act in their own interests, instead of in shareholders’.

- For example, the right to vote for directors on the board, or the right to repossess collateral.

- Otherwise, why would managers pay anything to shareholders or bondholders?

- And why would shareholders or bondholders provide any capital to them?

Difficult as small shareholder to get representative on the board

- If you can't get the managers do what you are interested in, then why would shareholders and bondholders invest?

Do Legal Environments Matter?

- Does being a shareholder in China or France give an investor the same privileges as being a shareholder in the United States, Australia, or Mexico?

- Would a secured creditor in Germany fair as well when the borrower defaults as one in Sri Lanka or Italy, assuming the value of the collateral is the same in all cases?

- What do you think is the role of enforcement of these rights?

Shareholder may have better protections in some countries than others

- Macroecnomic consequences to not having enough rights

- both to shareholder and debtholders

- Do you have the same kind of rights as outer countries

E.g. if you are an employee of a company that goes bankrupt, you are a creditor to the company

- You will be paid out before equityholders do.

How to protect shareholder interests?

- Elect board of directors to represent shareholders’ interests

- The use of takeover markets to remove inefficient managers

- Active and continuous monitoring by large blockholder

- Aligning managers and investor interests thru’ executive compensation

- Clearly defined fiduciary duties for CEOs; the threat of lawsuits

Add diversity; based on gender and culture

- Some companies have formal rules; Norway has 30% quota, e.g.

Ownership structure of company

- small and large shareholders, active and passive investors

- Managers can get away with acting in their own interests that it does not make sense for many investors to investigate

Rule: if anyone owns more than 5% of a company is considered a blockholder

- Vanguard, fidelity, and blackrock will own a large share of listed companies

Shareholder Protection

- Shareholder protection vary across the world.

- The role legal origin – focus of the lecture

- Dual class shares

- In July 2017, FTSE Russell and S&P announced that they will no longer admit dual-class shares to their indices

- Pyramid structures

- A controlling shareholder exercises control of one company through ownership of at least one other listed company.

- Cross-holdings

- Two or more firms hold shares in each other

- Role of controlling shareholders

Shareholder protection various between countries

legal origin - British and civil law countries

Having multiple classes of shares is generally considered bad practise

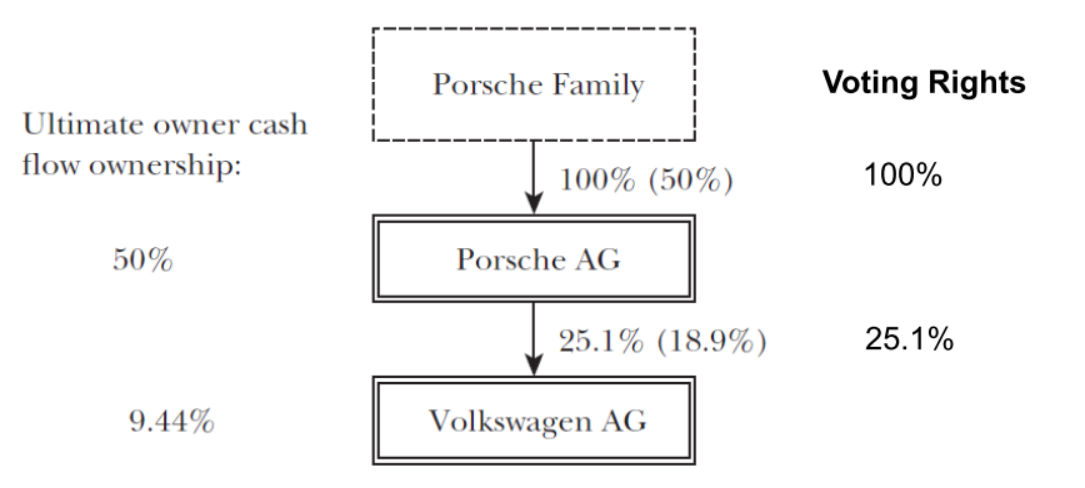

Pyramid structure

- One shareholder who controls/exercises through primary ownerships

- e.g. Porsche owning volkswagen group

Cross holding

- companies owning shares in each other, and a bank that provides capital

Class B shares, exactly the same but have 10x the voting rights

- Class C have no voting rights

- Considered bad governance

VW-Porsche Pyramid, 2006

Ownership and control is hard to disentangle. Voting rights is about how much say shareholders have.

Porsche AG - own 50% of the company but 100% of the voting rights, as all investors only own preferred shares

Computing Porsche’s ultimate voting rights in VW:

- Weakest link = minimum (25.1%, 100%) = 25.1%

- Last link = 25.1%

The “Law and Finance” view

- The Law and Finance view recognizes that the rights promised by stocks and bonds are only meaningful and secure if the legal system provides rights written into laws and a means for their enforcement.

- How could variation in investor protections

across countries explain cross-country variation

in:

- the ability of firms to raise external capital?

- the ability of firms (and the economy) to grow and prosper?

What rights exist in a country?

- Ultimately change how well a country can raise external capital

How do laws vary across countries?

- For this we need to measure the laws protecting security

holders as well as the quality of their enforcement.

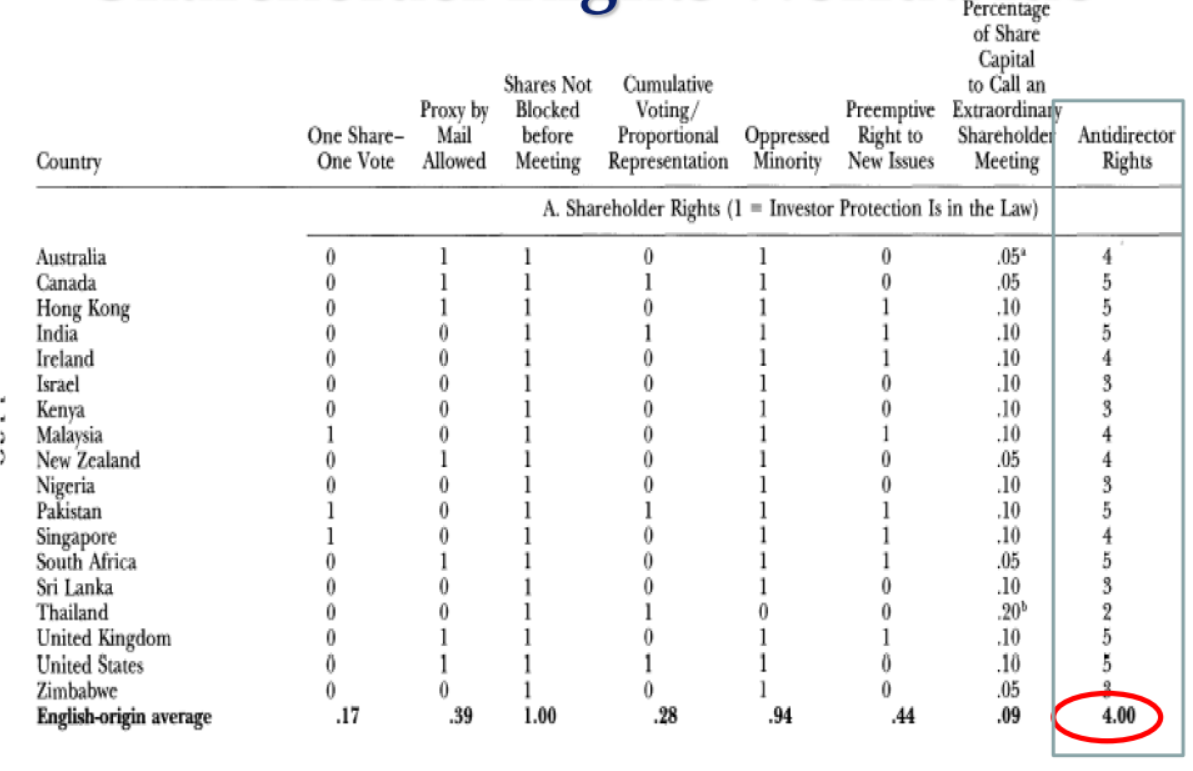

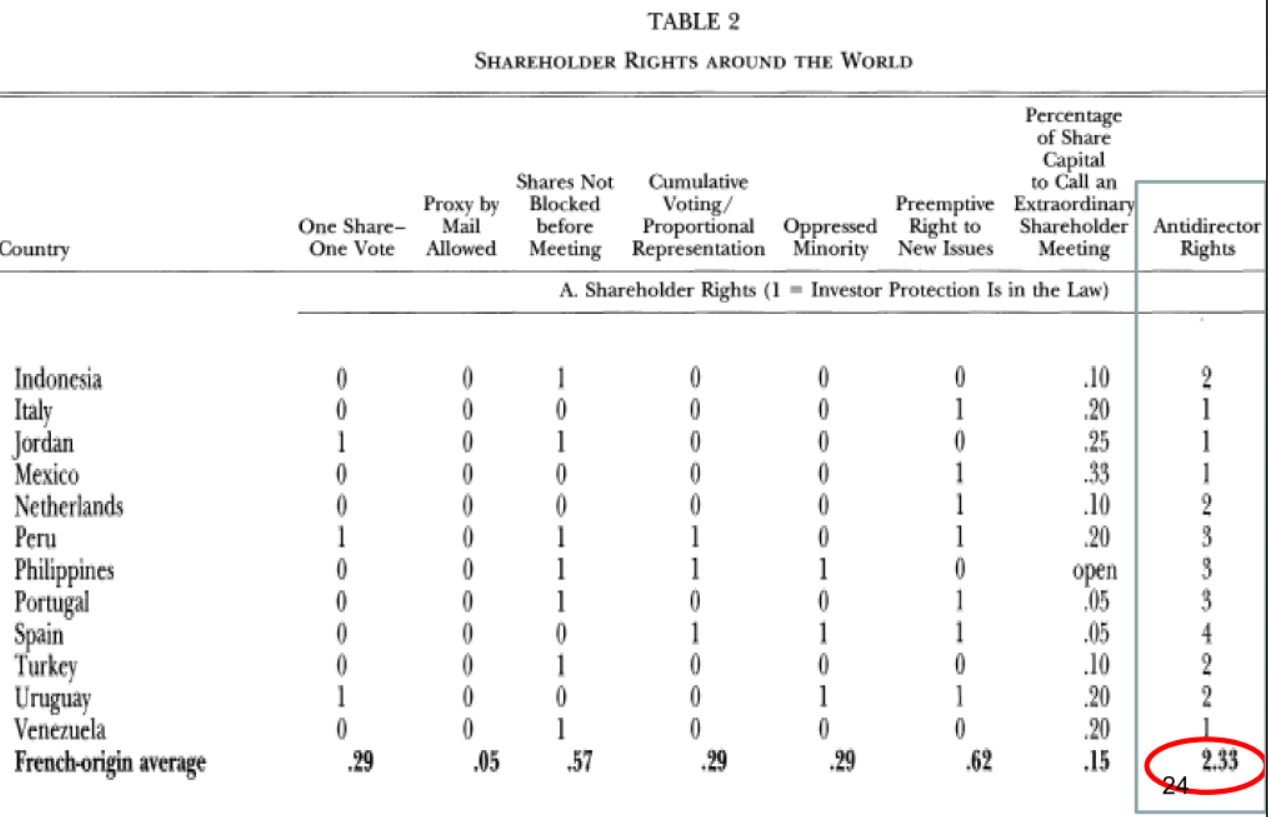

- Shareholder Rights (Anti-director Rights)

- Shareholders exercise their power by voting (for directors and on major corporate decisions). Thus, this measure will capture how strongly the legal system favors minority shareholders against either managers or dominant shareholders in the corporate decision-making process.

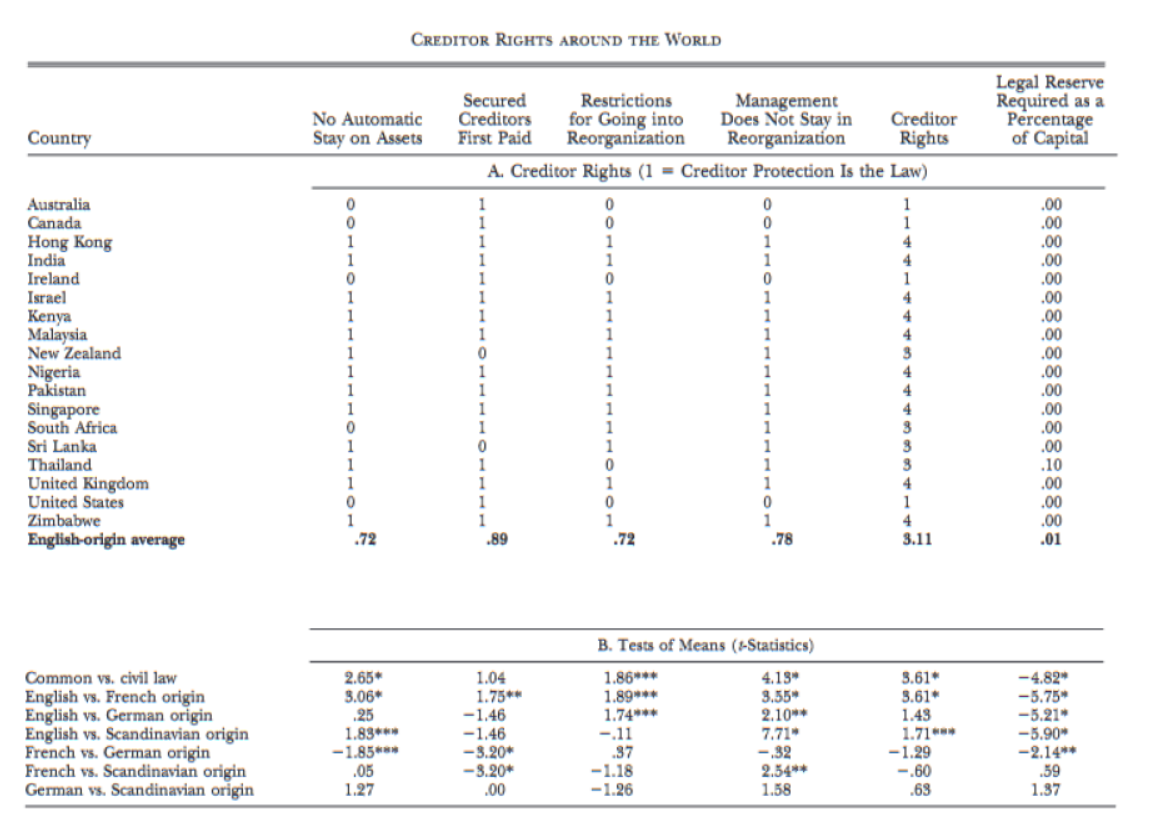

- Creditor Rights

- More complex to determine because there are many kinds of creditors (junior, senior, secured, unsecured). The perspective of the senior, secured creditor assumed here.

- Also, need to assess rights in both liquidation as well as in reorganization.

- Shareholder Rights (Anti-director Rights)

How well are the laws enforced, and what laws are in place?

- Quantify shareholder and creditor rights

- How easy difficult it is to seize the assets of the company and liquidate

Shareholder Rights Index

- The Issue is how to measure power shareholders have to make sure managers don’t steal the firm’s assets or make bad decisions.

- Each share owned carries one vote.

- The country allows shareholders to mail their proxy vote to the firm.

- Shareholders are not required to deposit their shares prior to the general shareholder’s meeting.

- Cumulative voting or proportional representation of minorities in board is allowed

In Australia, do not have to be physically present to vote

- In some countries, cannot sell shares immediately prior to shareholders meeting

- Straight forwarding system, In Australia can only cast max 1000 votes to another shareholder

- cumulative voting system can cast any number of votes to a representative

- The index continued..

- An oppressed minorities mechanism is in place

- The right to challenge the director decisions in court (derivative suit)

- The right to force the company to repurchase shares of minority shareholders who object to certain fundamental decisions (mergers or asset sales).

- Shareholders have preemptive rights to buy new issues of stock that can be waived only by a shareholder’s vote.

- The shareholder has the right to call an extraordinary shareholder’s meeting if own at least 10% of shares.

- An oppressed minorities mechanism is in place

Rule of thumb

Creditor Rights Index

- Measure creditor’s ability to seize the assets of the firm if the firm is unable to repay the loan or service the debt.

- The country imposes restrictions, such as creditors’ consent to file for reorganization

- Reorganization delays payment of creditors and gives management power (e.g., Chapter 11 in U.S.)

- Secured creditors are able to gain possession of their security once the reorganization petition has been approved (i.e., no automatic stay on assets)

- Secured creditors are first in line when the firm enters bankruptcy.

- As opposed to the government or employees

- Management can be dismissed during re-organization

- Creditors have more power than managers when the firm enters bankruptcy

- The country imposes restrictions, such as creditors’ consent to file for reorganization

If the creditors are not first in line for when firm enters bankruptcy, bad governance

- violates pecking order theory of finance governance

Where do laws come from?

- Laws in different countries are not typically written from scratch, but rather transplanted--- voluntarily or otherwise--- from a few legal families or traditions.

- Commercial laws come from two broad

traditions that have spread around the world by

conquest, imperialism, outright borrowing, and

more subtle imitation.

- Civil Law

- Common Law

Depends on legal origin

- Australia borrows from British legal system,

Common Law (English Origin)

- Common Law originated in England a millennium ago and was formed chiefly by judges who resolved specific factual disputes.

- Judicial precedents shape common law

- Spread to many British colonies, such as Australia, Canada, India, and the United States.

- Enforcement of common law is a private matter, accomplished through civil litigation (hence the importance of stockholder litigation in common-law countries, such as the U.S.)

- The penalty for violating common law is the award of damages to the party whose rights are proven violated.

Civil Law (French Origin)

- Civil Law, derived from Roman law, is the oldest, most influential, and widely distributed legal tradition around the world.

- Spread to most of the former colonies of France, Germany, Italy, Portugal, and Spain.

- Civil Law originates in governmental legislative bodies (who write “the code”) and is enforced by governments. It relies heavily on legal scholars to ascertain and formulate its rules.

- Code violation is a criminal matter, with criminal penalties (fines, imprisonment, restrictions on practice).

Not a private matter if there is a violation of rights

- Local governments/regulations sue the companies

- Relies on legal scholars rather than precedent

The Main Goal of the Study

- Show that shareholder and creditor protections

(legal rights and enforcement of those rights)

vary substantially across countries, and more

generally, across legal origins. Find that:

- French civil-law countries offer the weakest investor protections.

- English common-law countries offer the strongest investor protections.

If you are a shareholder in a common law country then you generally have more protection rights

Oppressed management system: sue managers

Creditor Rights

The Quality of Law Enforcement

- Efficiency of the Judicial System

- Rule of Law

- Corruption

- Risk of Expropriation

- Repudiation of Contracts by Government

- Also, include a measure of the quality of accounting standards

Corruption, risk of expropriation

- Do governments have a tendency to walk away from contracts?

- not just rights, enforcements of rights Quality of accounting standards

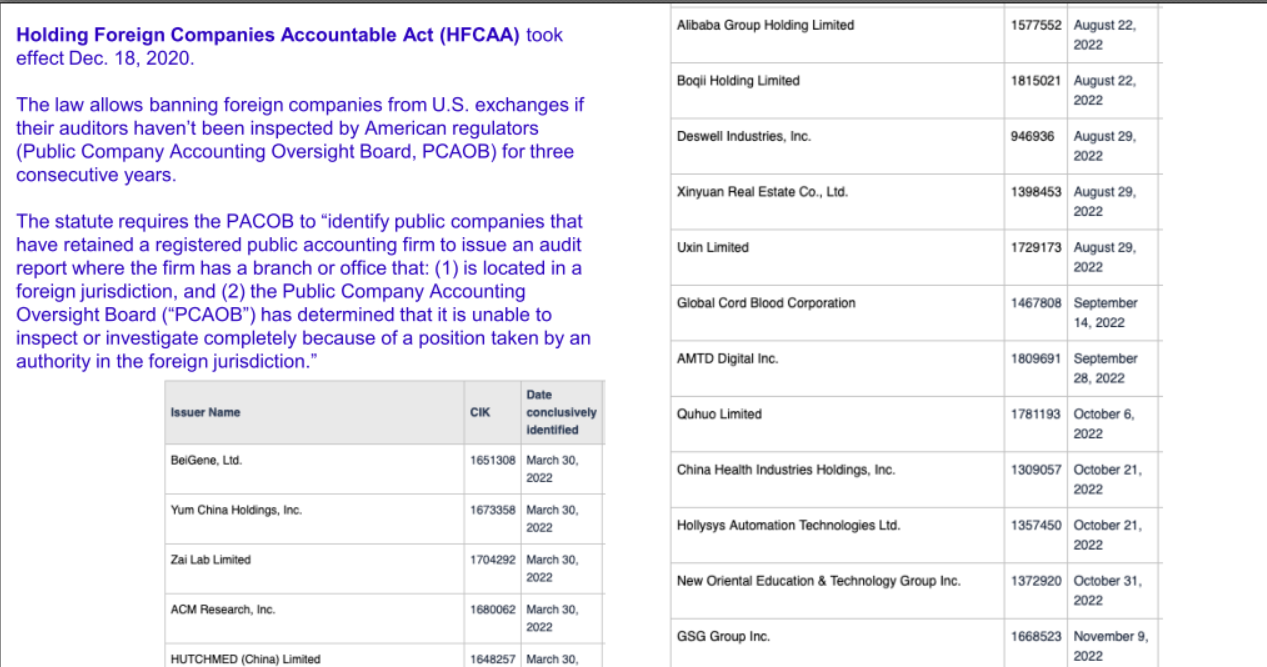

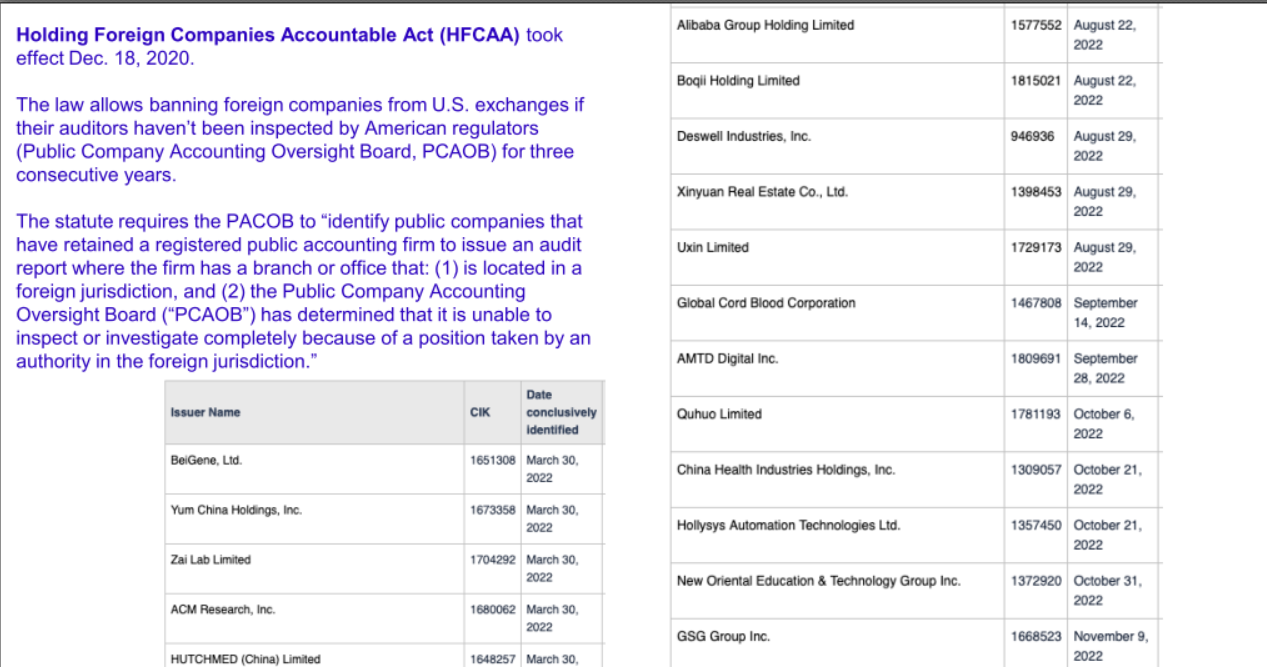

Law for Chinese firms that if they are being audited, overseas boards are not allowed to inspect their books

- US passed a law in 2020 which bans foreign countries from exchange if their books have not been audited

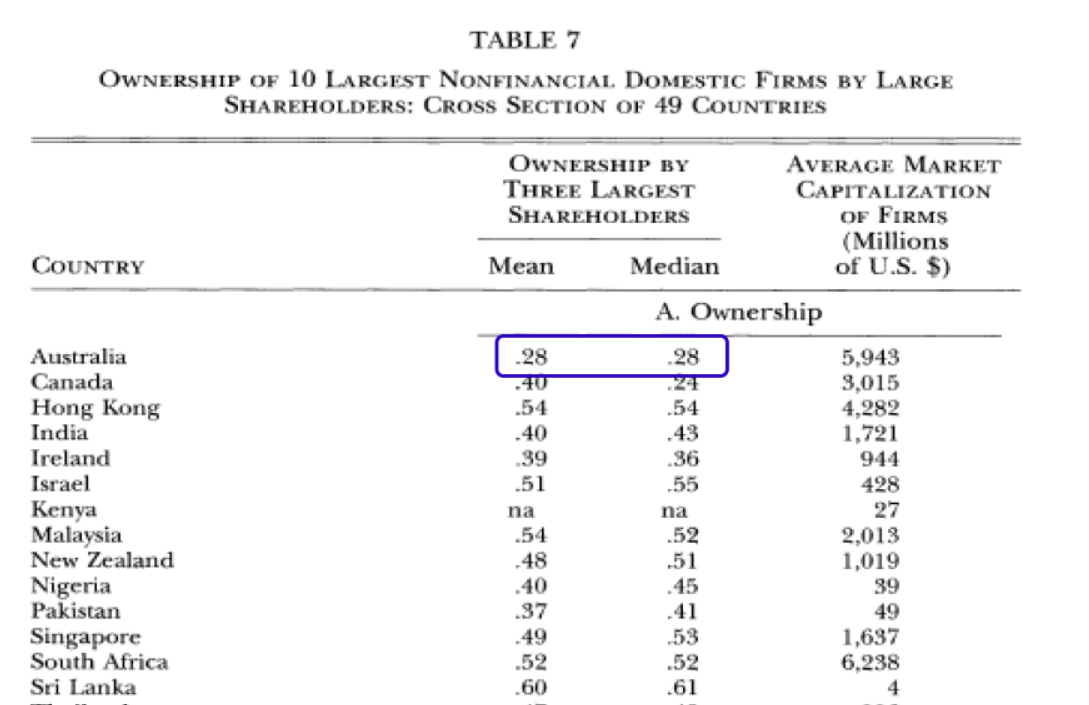

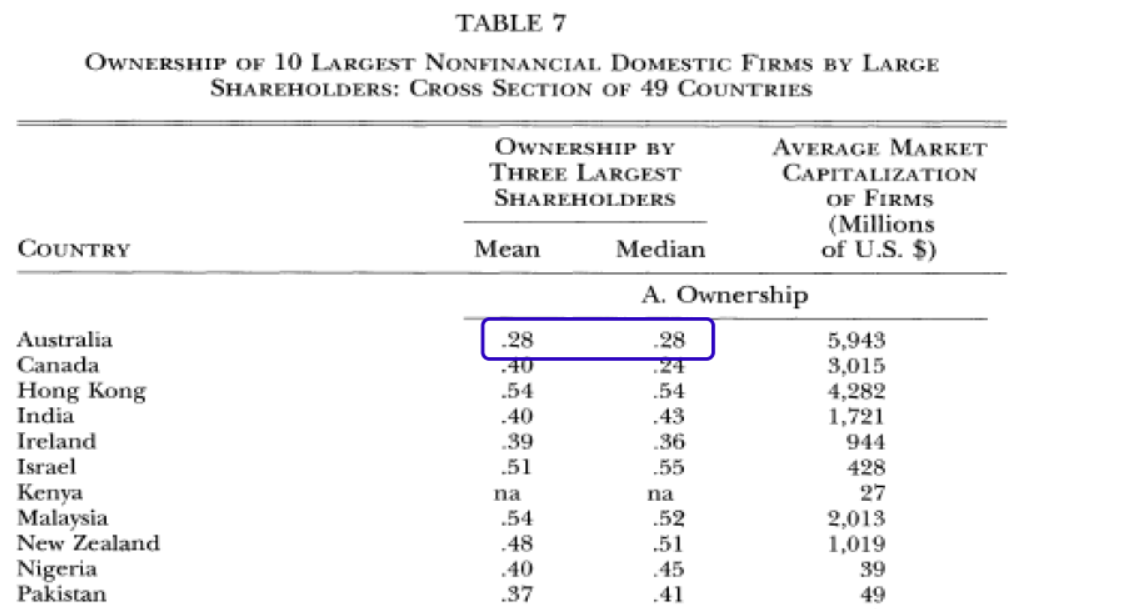

Large Shareholders

- Large Shareholders have incentive to monitor (e.g., Elon Musk’s initial Twitter stake of 9.2%).

- Demsetz and Lehn (1985) – In uncertain environments it is more difficult to monitor, so ownership concentration should be higher.

- Hypothesis: Ownership in countries with weak investor protections should be more concentrated because:

- More capital is needed to exercise control rights over management (prevent managers from expropriating the firm’s assets).

- Small (minority) shareholders might be willing to buy corporate shares only at very low prices that make it unattractive for firms to issue shares to the public.

- Economies evolve to have large shareholders

- Dispersed ownership is a myth -

Overall Tables 7 & 8 show

- “Dispersed ownership in large public companies is simply a myth. Even in the U.S., the average for the 10 most valuable companies is 20 percent.”

- “The finance textbook model of management faced by multitudes of dispersed shareholders is an exception and not the rule”.

- “The results support the idea that heavily concentrated ownership results from, and perhaps substitutes for, weak protection of investors in a corporate governance system.”

- “…these firms [in countries with weak investor protection] probably face difficulty raising equity finance, since minority investors fear expropriation by managers and concentrated owners.”

What matters for external finance?

- LLSV (1997) # relates the same investor protection measures (shareholder and creditor rights indices) to the ability of companies to raise external capital.

- English Common Law vs French Civil Law

- External Cap/GNP:

- 60% vs. 21%

- Domestic firms per 1 million people:

- 35 vs. 10

- IPOs per 1 million people:

- 2.2 vs. 0.19

- External Cap/GNP:

Probably because of the legal protections under common law

Is LLSV (1998) “settled science”?

- It turns out that the answer to this is No!!

- Holger Spamann of Harvard Law School critiques

the construction of LLSV’s Anti-Director index

- Faults the original paper for not using lawyers in each country to describe the various aspects of their legal system

- Re-collects data for 46 out of the 49 countries studied

- 33 out of 46 required corrections to the index.

- Correlation btw “old” & “corrected” index is 0.53

- Outcome: major conclusions of LLSV no longer hold.

Holger outlined that results were correct but conclusions were incorrect

- When you ask legal experts vs researchers to outline the quality of the legal standards in respective countries