Revision, lecture 1 & Chapt 5 textbook

Spot market

The spot market involves almost immediate purchase or sale of foreign exchange Quoted in direct or indirect terms

- Direct: Home currency per unit of foreign currency (FC)

- Indirect: Foreign currency (FC) per unit of Home currency

will refer to the price of one unit of currency in terms of currency .

Cross-exchange rate is an exchange between a currency pair where neither currency is the U.S. dollar

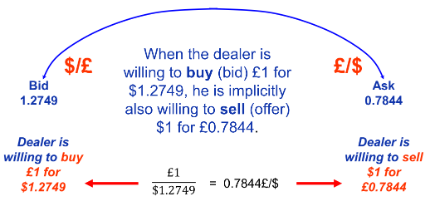

Bid-Ask spread

- Bid - the price in which the bank dealer will pay (buy) the currency for

- Ask - the price in which the bank dealer will sell the currency for

Calculating the cross-exchange rate Bid-Ask spread

- use two direct or indirect quotes

- a direct bid is the reciprocal of an indirect ask

- a direct ask is the reciprocal of an indirect bid

Forward market

- Contracting today for the future purchase or sale of foreign exchange

- , the price of one unit of currency in terms of currency for delivery in months

- under certain conditions the forward exchange rate is an unbiased predictor of the expected spot exchange rate months into the future.

- Trading at a premium to the dollar in American terms, we can say the markets expect the US dollar to depreciate relative to the Swiss franc

- When the dollar is trading at a discount to the Swiss franc, we can say the market expects the Swiss franc to appreciate, or become more valuable, relative to the dollar. It costs fewer francs to buy a dollar forward.

Forward premium

-

Express the premium or discount as an annualised percentage deviation from the spot rate

-

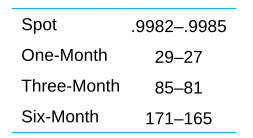

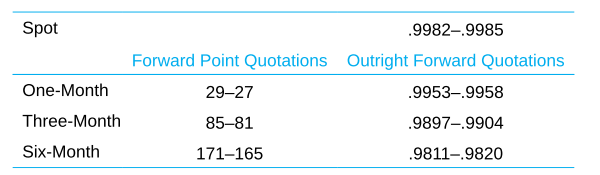

There are three ways to express forward rates:

- Via points to be added or subtracted from spot rate [known as swap points]

- Outright quotes

- As an annualized percentage forward premium or discount

Annualised percentage

Formula for calculating the forward premium or discount for currency over period in American terms is

3-month forward premium or discount for the Japanese yen versus dollar.

Current: .00897 3-month forward: .00903

three-month forward premium is 0.0265

Forward point transaction

forward rates might be displayed as:

- When the second known pair is smaller than the first, the dealer 'knows' the forward points are subtracted from the spot bid and ask price

Over/under valuation:

| Expected vs actual | Outcome | Reason | Arbitrage profit |

|---|---|---|---|

| Expected exchange rate (QC/BC) > actual exchange rate | - base currency is undervalued - Quotation currency is over-valued |

- You could be potentially earning more of the quotation currency given 1 unit of BC | - Buy the undervalued base currency - Borrow/Sell the overvalued quotation currency |

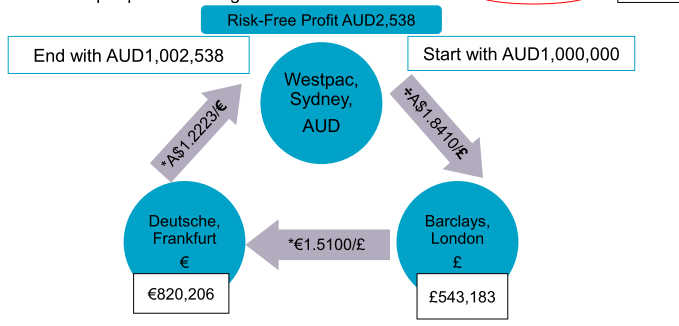

Triangular arbitrage

- Think of it in terms of the base currency. I.e., if the investment is in terms of $1M AUD, convert the cross rates to have an AUD base currency

- Between the synthetic cross rate and the actual cross rate

- You will want to transact the most expensive cross rate first. Because the rates are in BC of the investment, you would multiple by the first investment, and divide by the second.

- Risk free profit