Revision Lecture 10

International Diversification

Why Invest Overseas?

- Security returns are much less correlated across countries than within a country.

- This is so because economic, political, institutional, and even psychological factors affecting security returns tend to vary across countries, resulting in low correlations among international securities.

- Business cycles are often highly asynchronous across countries.

Foreign Exchange Returns

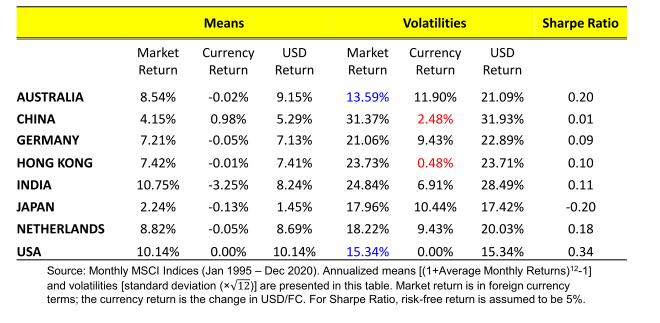

- An illustration with Australian stock returns

- The total return reflects not only the appreciation in the USD stock price but also the change in the USD (appreciation in this case)

- The formula for the total return is

Where

And

- - microsoft share

General Formula

- The total return of the foreign investment reflects not only the appreciation of the foreign asset, but also the appreciation (or depreciation) of the foreign currency relative to the home currency.

- The formula for the total return is:

where

- HC = home currency;

- FC = foreign currency relative to home currency (FC is in the denominator).

- Asset (FC) means the asset value is in FC

Foreign Returns and risk

Adding up volatilities

- As shown in the previous slide, the volatility of currency returns affects the volatility of USD return on a foreign equity (last column). But volatilities of FC market returns & currency returns are not additive. Why?

If correlation () = 1, the volatility of the dollar return is the sum of the foreign equity volatility and currency return volatility.

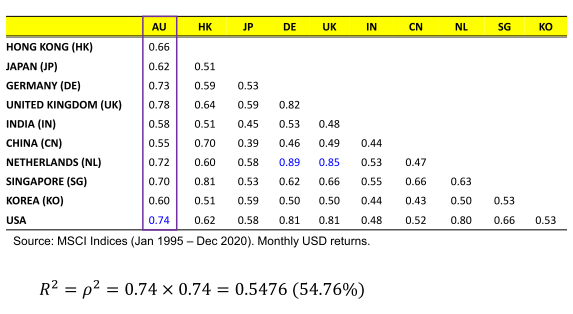

Key results of portfolio theory

- The extent to which risk is reduced by portfolio diversification depends on the correlation of assets in the portfolio.

- As the number of assets increases, portfolio variance becomes more dependent on the covariances (or correlations) and less dependent on variances.

- The risk of an asset when held in a large portfolio depends on its return covariance (or correlation) with other assets in the portfolio.

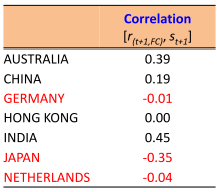

International Correlations & Risk Diversification

- This means that if we diversify our investments, we can reduce our risk.

International Correlations

- Why do we expect return correlations across markets to be lower than within markets?

- different regulation, tax laws

- different industrial structure

- different cultures

- affected by different shocks

- affected differently by same shocks

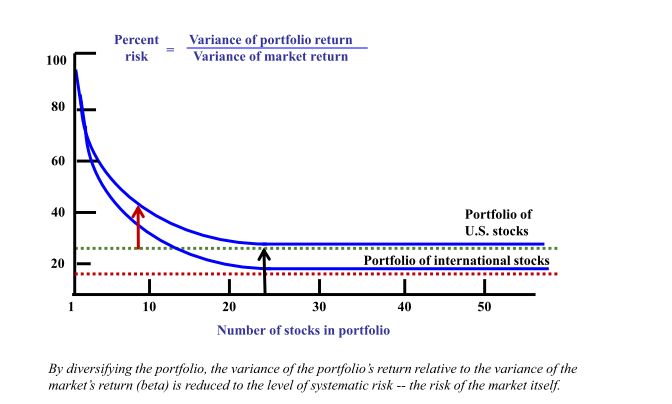

Case for International Diversification

Integrating with other Economies (international stocks)

- Risk reduction is even more dramatic

- about 15% of the risk of a typical security

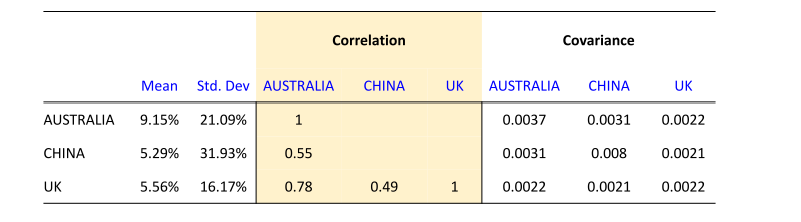

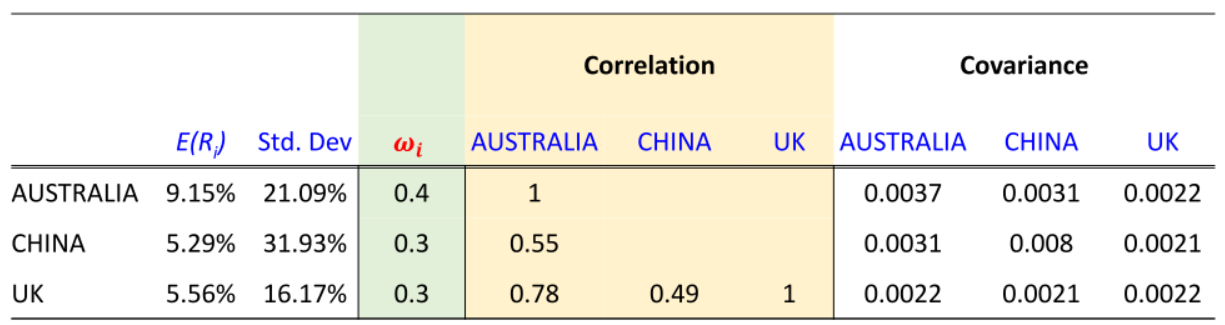

Risk and Return

- We can form a portfolio of these stock portfolios rather than invest in only one country.

Expected Return of the portfolio

Variance of the Portfolio

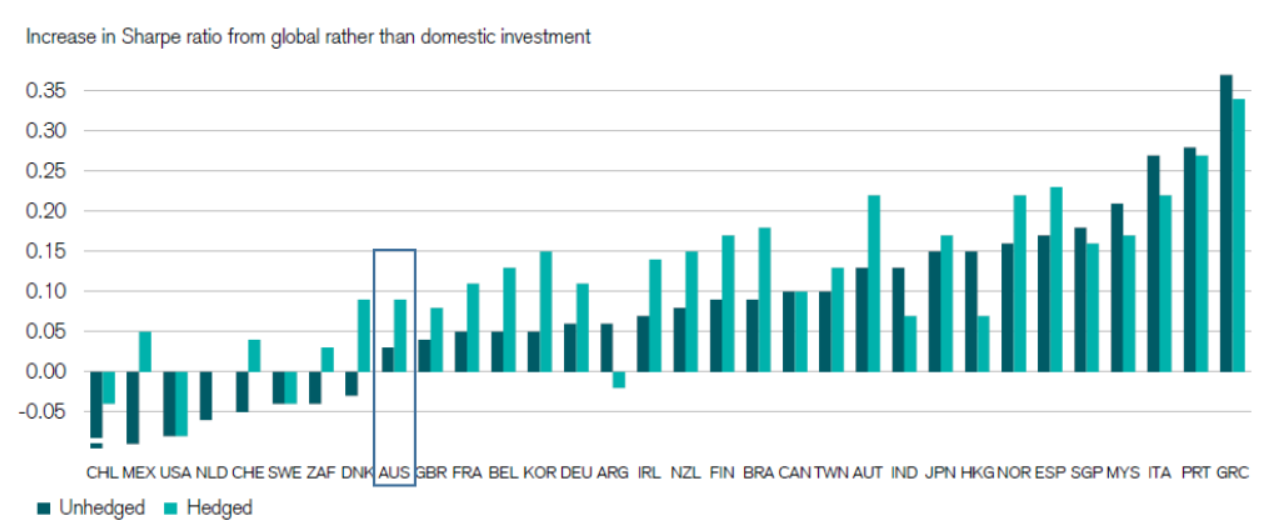

Does Diversification work elsewhere?

Below: increase in Sharpe ratio from global rather than domestic investment

- Compare Sharpe ratios for various strategies – local vs global.

- Bars below zero (8 countries) – better off investing in the domestic market. Mostly had high local returns combined with below average risk.

- Positive values – gains from global diversification.

Why List (or Cross-List) on Foreign Exchanges?

Reasons to List (i.e. a solo listing) or Cross-List

- Lowering of cost of capital

- Improve liquidity

- “Bond” to a better regulatory environment

- Broaden shareholder base

- Access to capital (obtain better valuations)

- Enables the use of stock to (a) compensate employees not in country of domicile; (b) pay for acquisitions

- Raise visibility of company