Lecture 2, revised

Floating exchange rate

- Under the floating rate system, the exchange rate is determined entirely by forces of supply and demand

- The system that prevailed was not quite “freely floating”

- Central banks had the obligation to intervene to prevent “disorderly conditions”

- A lot of rules in place, rules of capital movements

Advantages of a fixed vs a floating ER:

Advantages of a Fixed ER

- Reduce transaction costs and exchange rate risk which can discourage trade

Advantages of a float

- Ability to pursue an independent monetary policy

- Ability to use monetary policy to respond to recessionary effects on the economy

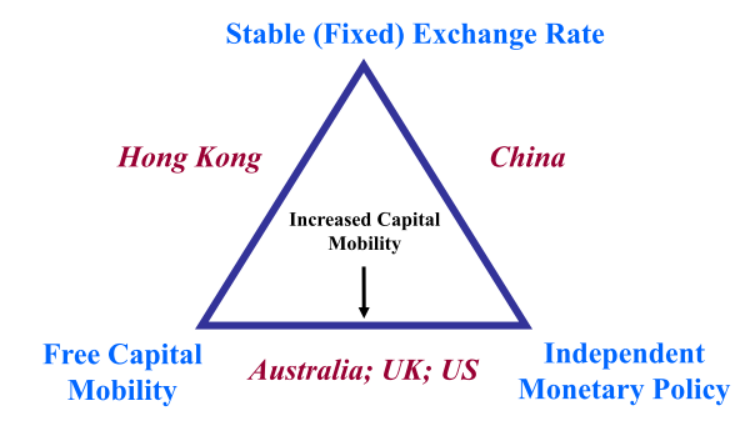

Impossible Trinity

A country must give up one of the three goals:

- Exchange rate stability

- Full financial integration (free flow of capital)

- Monetary independence (of domestic policies)

Balance of Payments - BOP

- The BOP is a statistical record of the flow of all of the payments between the residents of a country and the rest of the world in a given year.

For example, an overall BOP deficit indicates that a country is borrowing from overseas and running down its net asset position. A country running a CA surplus is accumulating claims on foreigners and building up a positive net foreign asset position.

Accounting Principles

- Any transaction resulting in a payment to foreigners is entered in the BOP accounts as a debit and is given a negative sign.

- Any transaction resulting in a receipt from foreigners is entered as a credit and given a positive sign.

Assuming change in official reserves and errors are approximately zero:

This will hold approximately for floating rate countries.

Current Account (CA)

Comprises of:

- Exports

- Imports

- Primary Income

- payments of receipts, dividends and other income on foreign investments that were previously made

- secondary income - unilateral transfers

- 'unrequited' payments, including foreign aid, reparations, official and private grants, etc.

NOTE:

A country must finance its current account deficit either borrowing from foreigners or by drawing down on its previously accumulated foreign wealth, a current account deficit represents a reduction in the country’s net foreign wealth

CA = Exports (x) - Imports (M)

- Current Account Deficit:

- Current Account Surplus:

Capital Account

- Capital account includes capital transfers and disposals of nonfinancial assets between residents and foreigners.

Financial Account (and capital account)

-

It includes all short and long-term financial transactions pertaining to both international trade and flows associated with portfolio shifts (stocks, bonds etc.)

-

There is also another account, the Capital Account and this account records “purchase/sale of non-produced, non-financial assets and capital transfers”.

-

Balance difference between sales of assets to foreigners and purchases of foreign assets

Comprises of:

- Portfolio investment

- Direct investment

- (takeover or acquiring a substantial portion of a foreign company, i.e., ˃ 10%)

- Other Investment

Sales of assets are recorded as credits, and result in inflows to the KA account. Purchases (imports) of foreign assets are recorded as debits and lead to capital outflow.

Official Reserve Assets

-

Total reserves held by official monetary authorities within a country (RBA in Australia).

-

These reserves are typically comprised of major currencies that are used in international trade and financial transactions, gold and reserve accounts (SDRs) held at the IMF.

-

When foreign governments wish to support the value of the dollar in the foreign exchange market, they sell foreign exchange, SDRs, or gold to 'buy' dollars

Errors and Omissions

- Errors and Omissions - difference between CA balance, Capital Account and Financial Account

- Errors and omissions also used in valuations

The only way you can run a deficit if is someone is willing to fund it - funded by the central bank

Linking CA to National Income

Where: - Consumption, - Investments, - Government spending

National Savings (S)

Therefore:

- CA Deficit → CA < 0 → Borrowing from Abroad to finance domestic spending

- CA Surplus → CA > 0 → Lending Abroad

Implication

- If a country’s income exceeds its spending, savings will exceed domestic investment, yielding surplus capital.

- This surplus capital will be invested overseas and will be reflected as a financial account (KA) deficit for that country (more capital is flowing out of the country than into it).

NOTE

- If Australia is running of CA surplus and its domestic residents are NOT acquiring foreign assets, then it must be that the RBA is acquiring foreign assets (i.e., there is a drawing down of the central bank’s reserve holdings)

- If the BOP is negative, then ORT is positive with the RBA selling FOREX reserves and buying domestic currency.

CA and KA balances

| Credit (+) | Debit (-) | Account |

|---|---|---|

| Export of goods and services | Import of goods and services | CA |

| Income received (dividends or interest) | Income paid | CA |

| Unilateral transfer received | Unilateral transfer paid | CA |

| Increasing domestic asset owned by foreigner | Decreasing domestic assets owned by foreigners | KA |

| Decreasing foreign assets owned by home residents | Increasing foreign assets owned by home residents (giving out a loan, e.g.) | KA |

| Increase in liabilities (to foreign country) | Decrease in liabilities (to foreign country) | KA |