Revision Lecture 4

Foreign Currency derivatives

- These are financial instruments whose value depends on an observable value

- Derivatives include:

- Options: A contract that grants the holder the right, but not the obligation, to transact in an asset.

- Futures: A contract to buy or sell a commodity at a point in the future. Changes in prices in the commodity are settled daily.

- Swaps: A contract in which two parties exchange cashflows from different financial instruments.

Futures and Forwards

Currency forward and futures contracts both represent an obligation to buy or sell a certain amount of a specified currency some time in the future at an exchange rate determined now.

| - | Futures contracts | Forwards Contract |

|---|---|---|

| Markets: | Prices determined in centralised exchanges | Decentralised interbank market |

| Trading Hours: | Most trading during exchange hours | Open somewhere around the world |

| Contract size | Standardised sizes depending on currency | Standard size of $1m etc. and can be tailored |

| Contract maturity | Fixed delivery dates: 3rd Wed. of March, June Sept or Dec. | Fixed maturities (1, 3, 6 or 12 months) or can be tailored to specifications |

| Quotation: | American terms (USD/FC) | American (USD/FC) or European (FC/USD) |

| Settlement | Delivery of underlying fx is feasible, but almost never occurs. Position closed out by taking an offsetting position | Delivery of foreign exchange normally takes place |

| Security against default | Clearing houses stand behind traders | Assets of bank |

| Required collateral | Margin requirements ("Performance bond") | Deposit required if not standing relations with bank |

| Cash flows | Occur daily because of "market-to-market" feature | No cash flows until forward contract matures |

Options contracts

Options contracts give the option holder the right, but not the obligation to buy or sell a specified amount of the underlying asset (currency; stock) at a pre-determined price (exercise or strike price).

Basics of Options

'The right, but not the obligation'

- Types of Options

- Call: gives the holder the right to buy

- Put: gives the holder the right to sell

- An American option gives the buyer the right to exercise the option at any time between the date of writing and the expiration or maturity date.

- American option will always be more expensive than an equivalent European option (of the same terms)

- A European option can be exercised only on the expiration date, not before.

- The exercise or strike price (X), which is the exchange rate at which foreign currency can be purchased (call) or sold (put).

- The premium, cost, price, or value of the option itself (paid in advance by the buyer to the seller).

- The underlying or actual spot exchange rate in the market.

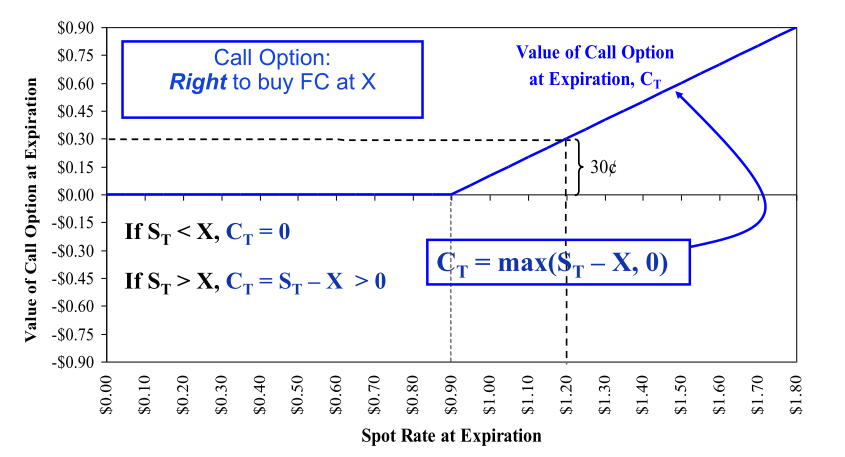

Value of a call option at Expiration

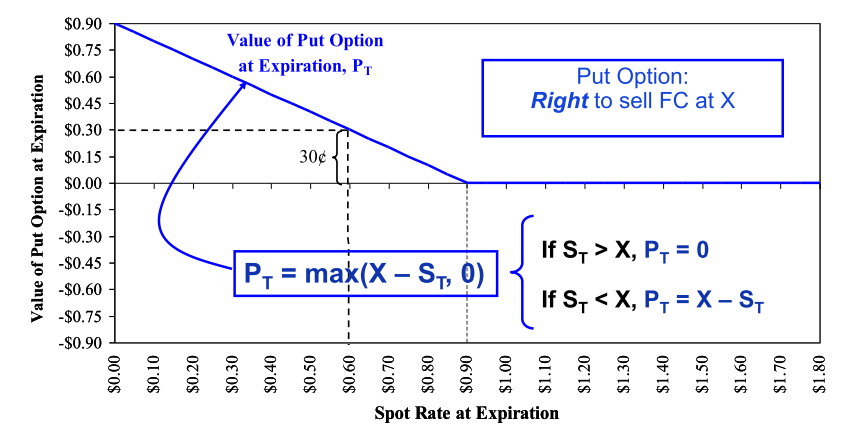

Value of the put option at Expiration