Lecture 5 Revision

Hedging Transaction Exposure

Foreign exchange rate exposure

- Unexpected changes in exchange rates may affect a firm’s cash flows and market value

- either through its effect on existing contracts -> Transaction Exposure

- or through its impact on the future operating cash flows of the firm -> Operating Exposure (aka Economic Exposure)

- Exchange rate changes may have an impact on accounting values

- This is called Accounting Exposure or Translation Exposure

Transaction Exposure

- Transaction exposure measures gains or losses that arise from the settlement of existing financial obligations (e.g., account receivables, account payables) whose terms are stated in a foreign currency.

- A classic example of transaction exposure is a firm that has signed a contract to ship goods overseas at a fixed foreign currency price.

Sources of Transaction Exposure

- Transaction exposure arises from:

- Purchasing or selling on credit goods or services whose prices are stated in foreign currencies

- Borrowing or lending funds when repayment is to be made in a foreign currency

- Being a party to an unperformed foreign exchange forward contract

- Otherwise acquiring assets or incurring liabilities denominated in foreign currencies.

Measuring Exposure: Value-at-Risk

- Aim: To estimate the potential loss in value due to adverse exchange rate movements over a defined horizon with a specific confidence level.

- Regulators use Value-at-Risk (VaR) to compute capital requirements for financial institutions (e.g., Basel II)

- Typical confidence level is 99% or 95% focusing on the 1% or 5% worst case scenario.

- REVISIT IF RELEVANT

Hedging Transaction Exposure

- Transaction exposure can be managed by contractual, operating, and financial hedges:

- Contractual Hedges employ the use of

- Forwards/futures, Options, and Money Markets

- Operating and Financial Hedges employ the use of

- Risk-Sharing Agreements, Leads and Lags in Payment Terms, Swaps and Other Strategies

- Contractual Hedges employ the use of

Contractual Hedging Techniques

-

Forward/Futures Hedge

-

Currency option hedge

- A way to hedge contingent exposure

-

Money Market hedge: Taking a money market position to hedge future receivables/payables

-

Structuring the Hedge

- exporters (sell FOREX, buy AUD) - receivables

- importers (buy FOREX, sell AUD) - payables

Hedging with Options

- Recall, options give the option holder the right, but not the obligation to buy or sell a specified amount of the underlying asset (currency) at a pre-determined price.

- Premium is paid in advance by the buyer to the seller.

- In the context of hedging, these contracts can be viewed as exchange rate insurance written against adverse exchange rate movements – options are written on the spot rate.

- FOREX call options on spot can be used as insurance to establish a ceiling price on the home currency cost of foreign exchange.

- Ceiling Price = exercise price of call + call premium

- FOREX put options on spot can be used as insurance to establish a floor price on the home currency cost of foreign exchange.

- Floor Price = exercise price of put – put premium

- FOREX call options on spot can be used as insurance to establish a ceiling price on the home currency cost of foreign exchange.

Money Market Hedge

- Money Market Hedge: Borrow (or lend) in the foreign currency to hedge its foreign currency receivables (payables) – match foreign currency assets & liabilities in the same currency

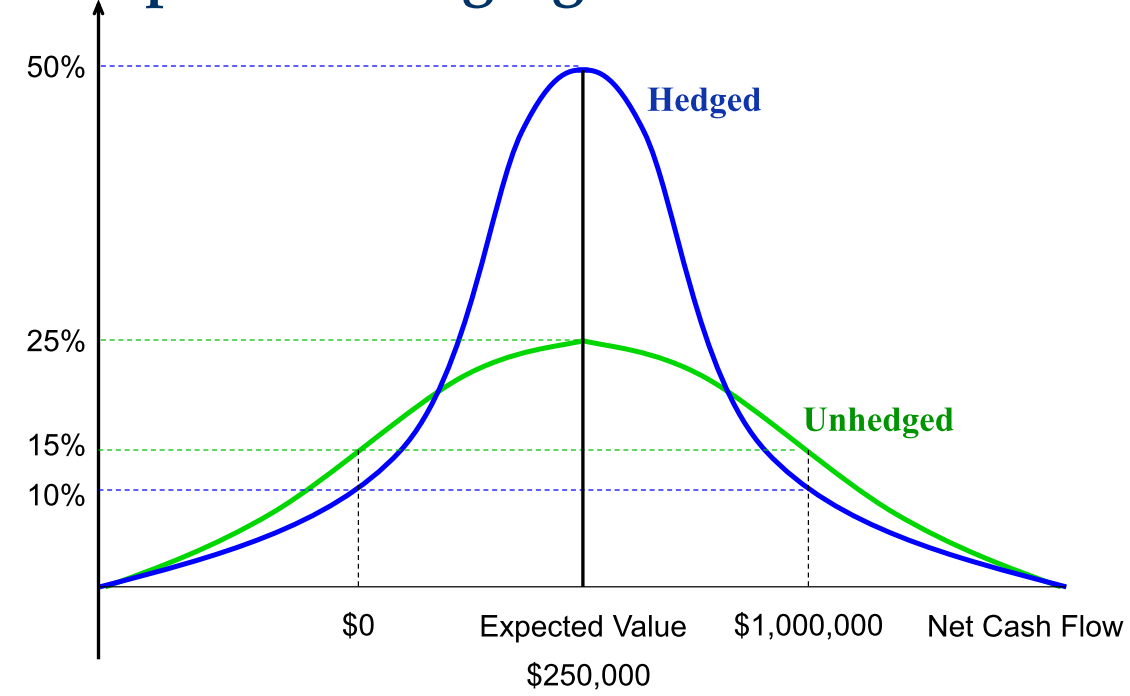

Impact on Hedging on E(Cash flows)

Hedging reduces the variability of expected cash flows about the mean of the distribution.

Views of Hedging

Is the reduction of variability of cash flows then sufficient reason for currency risk management?

-

Opponents of currency hedging commonly make the following arguments:

- Stockholders are much more capable of diversifying currency risk than the management of the firm.

- Currency risk management does not add value to the firm, and it incurs costs (i.e., it is costly).

- Hedging might benefit corporate management more than shareholders.

- Management’s motivation to reduce variability is sometimes driven by accounting reasons.

-

Proponents for currency hedging argue:

- Risk Profile of Investments (Agency Costs)

- Shareholders hold an option on the value of the firm and would prefer riskier projects.

- Since, riskier projects reduce the value of bondholders’ claims, bondholders are likely to require compensation in the form of a higher returns.

- If shareholders can credibly commit not to unduly increase risks, a lower cost of debt financing could result.

- Additional sources of agency costs come from managers’ preference for less risky projects (job security).

- Reduction of risk in future cash flows reduces the likelihood that the firm’s cash flows will fall below a necessary minimum (and put the firm in financial distress).

- Reduction of risk in future cash flows improves the planning capability of the firm. - If the firm can more accurately predict future cash flows, it may be able to undertake specific investments or activities that it might otherwise not consider.

- Individuals and corporations do not have same access to hedging instruments or same cost.