Revision Lecture 9

International Corporate Governance

Separation of Ownership and Control

- Who owns companies? Owners/Investors

- Who runs companies? Managers

- When ownership and control of corporations are not aligned there is potential for conflicts of interest between owners and managers.

- Are managers using company funds for the right purposes?

- Are they investing in positive NPV projects?

- Are they spending too much money on themselves?

Shareholder & Creditor Rights

- The RIGHTS attached to securities become important when managers act in their own interests, instead of in shareholders’.

- For example, the right to vote for directors on the board, or the right to repossess collateral.

- Otherwise, why would managers pay anything to shareholders or bondholders?

- And why would shareholders or bondholders provide any capital to them?

Do Legal Environments Matter?

- Does being a shareholder in China or France give an investor the same privileges as being a shareholder in the United States, Australia, or Mexico?

Shareholder may have better protections in some countries than others

How to protect shareholder interests?

- Elect board of directors to represent shareholders’ interests

- The use of takeover markets to remove inefficient managers

- Active and continuous monitoring by large blockholder

- Aligning managers and investor interests through executive compensation

- Clearly defined fiduciary duties for CEOs; the threat of lawsuits

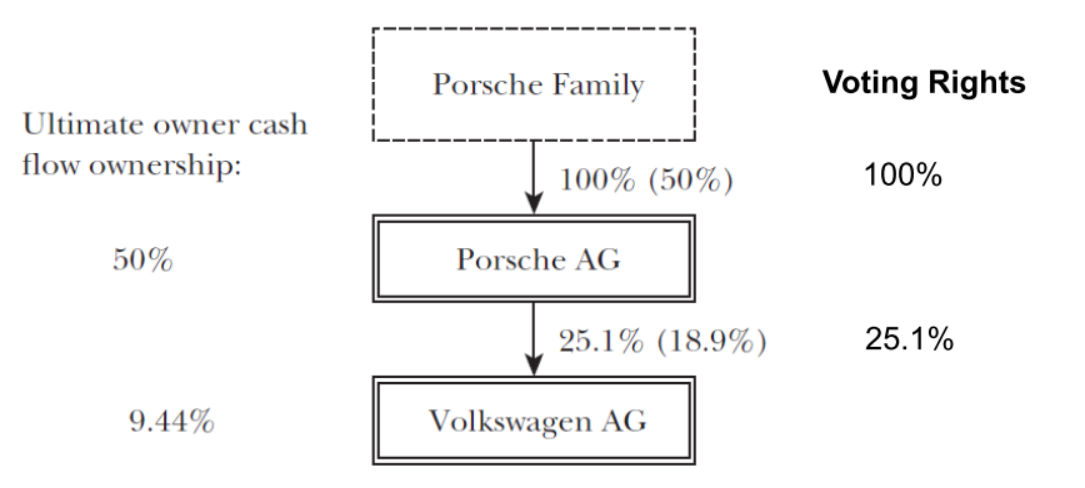

VW-Porsche Pyramid, 2006

Ownership and control is hard to disentangle. Voting rights is about how much say shareholders have.

Porsche AG - own 50% of the company but 100% of the voting rights, as all investors only own preferred shares

Computing Porsche’s ultimate voting rights in VW:

- Weakest link = minimum (25.1%, 100%) = 25.1%

- Last link = 25.1%

The “Law and Finance” view

- The Law and Finance view recognizes that the rights promised by stocks and bonds are only meaningful and secure if the legal system provides rights written into laws and a means for their enforcement.

- How could variation in investor protections across countries explain cross-country variation

in:

- the ability of firms to raise external capital?

- the ability of firms (and the economy) to grow and prosper?

How do laws vary across countries?

- For this we need to measure the laws protecting security

holders as well as the quality of their enforcement.

- Shareholder Rights (Anti-director Rights)

- Shareholders exercise their power by voting (for directors and on major corporate decisions). Thus, this measure will capture how strongly the legal system favors minority shareholders against either managers or dominant shareholders in the corporate decision-making process.

- Creditor Rights

- More complex to determine because there are many kinds of creditors (junior, senior, secured, unsecured). The perspective of the senior, secured creditor assumed here.

- Also, need to assess rights in both liquidation as well as in reorganization.

- Shareholder Rights (Anti-director Rights)

Shareholder Rights Index

- The Issue is how to measure power shareholders have to make sure managers don’t steal the firm’s assets or make bad decisions.

- Each share owned carries one vote.

- The country allows shareholders to mail their proxy vote to the firm.

- Shareholders are not required to deposit their shares prior to the general shareholder’s meeting.

- Cumulative voting or proportional representation of minorities in board is allowed

- An oppressed minorities mechanism is in place

- The right to challenge the director decisions in court (derivative suit)

- The right to force the company to repurchase shares of minority shareholders who object to certain fundamental decisions (mergers or asset sales).

- Shareholders have preemptive rights to buy new issues of stock that can be waived only by a shareholder’s vote.

- The shareholder has the right to call an extraordinary shareholder’s meeting if own at least 10% of shares.

Creditor rights index

- Measure creditor’s ability to seize the assets of the firm if the firm is unable to repay the loan or service the debt.

- The country imposes restrictions, such as creditors’ consent to file for reorganization

- Reorganization delays payment of creditors and gives management power (e.g., Chapter 11 in U.S.)

- Secured creditors are able to gain possession of their security once the reorganization petition has been approved (i.e., no automatic stay on assets)

- Secured creditors are first in line when the firm enters bankruptcy.

- As opposed to the government or employees

- Management can be dismissed during re-organization

- Creditors have more power than managers when the firm enters bankruptcy

- The country imposes restrictions, such as creditors’ consent to file for reorganization

Where do laws come from?

- Laws in different countries are not typically written from scratch, but rather transplanted--- voluntarily or otherwise--- from a few legal families or traditions.

- Commercial laws come from two broad traditions that have spread around the world by conquest, imperialism, outright borrowing, and more subtle imitation.

- Civil Law

- Common Law

Common Law (English Origin)

- Common Law originated in England a millennium ago and was formed chiefly by judges who resolved specific factual disputes.

- Judicial precedents shape common law

- Spread to many British colonies, such as Australia, Canada, India, and the United States.

- Enforcement of common law is a private matter, accomplished through civil litigation (hence the importance of stockholder litigation in common-law countries, such as the U.S.)

- The penalty for violating common law is the award of damages to the party whose rights are proven violated.

Civil Law (French Origin)

- Civil Law, derived from Roman law, is the oldest, most influential, and widely distributed legal tradition around the world.

- Spread to most of the former colonies of France, Germany, Italy, Portugal, and Spain.

- Civil Law originates in governmental legislative bodies (who write “the code”) and is enforced by governments. It relies heavily on legal scholars to ascertain and formulate its rules.

- Code violation is a criminal matter, with criminal penalties (fines, imprisonment, restrictions on practice).

Legal origin study outcomes:

- French civil-law countries offer the weakest investor protections.

- English common-law countries offer the strongest investor protections.

Large Shareholders

- Large Shareholders have incentive to monitor (e.g., Elon Musk’s initial Twitter stake of 9.2%).

- Demsetz and Lehn (1985) – In uncertain environments it is more difficult to monitor, so ownership concentration should be higher.

- Hypothesis: Ownership in countries with weak investor protections should be more concentrated because:

- More capital is needed to exercise control rights over management (prevent managers from expropriating the firm’s assets).

- Small (minority) shareholders might be willing to buy corporate shares only at very low prices that make it unattractive for firms to issue shares to the public.