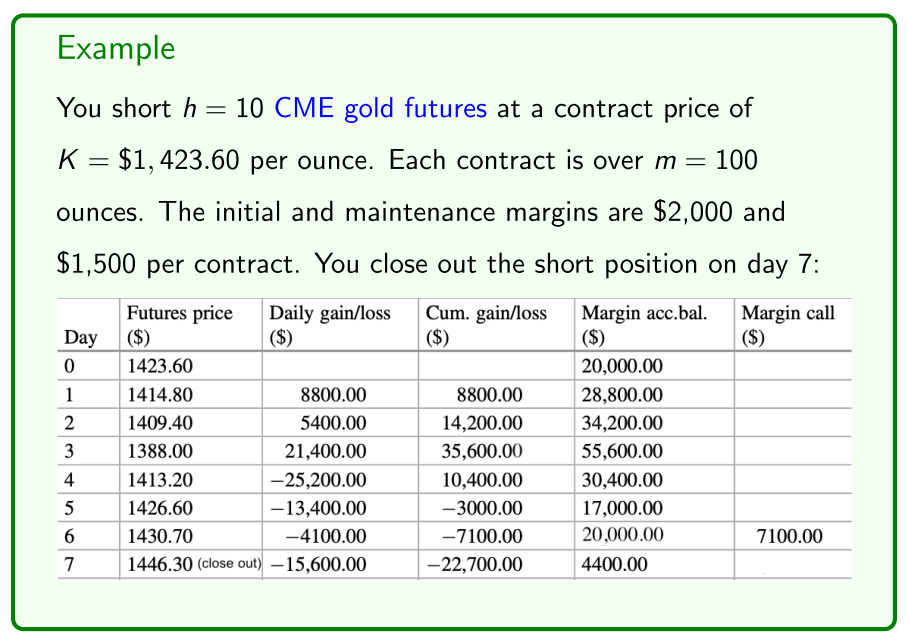

Lecture 2 Futures and forwards - Examples and basic concepts

Futures and forwards are contracts between two parties to trade an agreed quantity of an asset for an agreed contract or forward price on an agreed future delivery or maturity date .

- Written over all kinds of assets including shares, ETFs, indices, commodities, interest rates, currencies, energy, weather events, etc.

- Traded all over the world, with forward contracts traded in OTC markets and futures contracts traded on organised exchanges.

- Many uses including speculation and trading, risk management or hedging, arbitrage trading and price discovery, structured and synthetic product construction, portfolio exposure modification, etc.

contract price or forward price

- delivery date of the asset

- written on other derivatives

- forwards are traded (arranged) OTC

- futures are traded on organised exchanges

- nowadays

Get a sense of underlying assets from futures market trading

- shares are based on the futures market trading price

- futures used for construction and synthetic products

Futures and Forwards

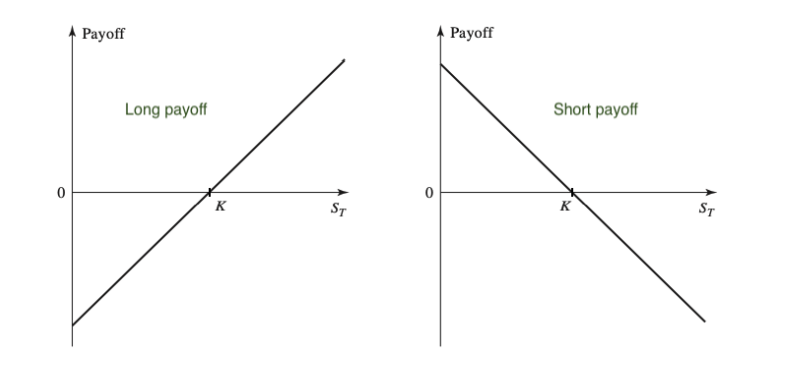

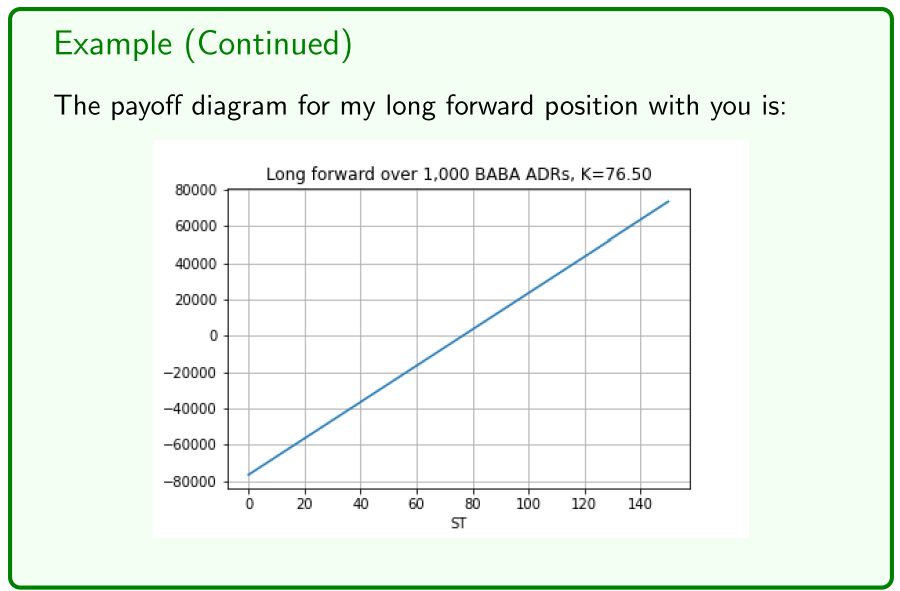

The payoffs at maturity from 1 contract (over 1 asset) are:

long payoff = and short payoff = .

buying assets for K

- spot price is higher, can sell at the spot price for higher and make a profit

Futures and Forwards

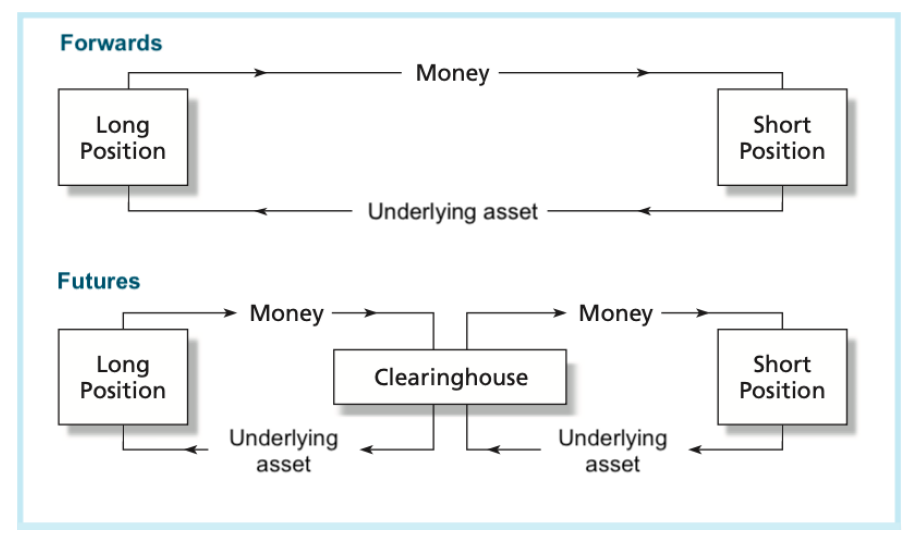

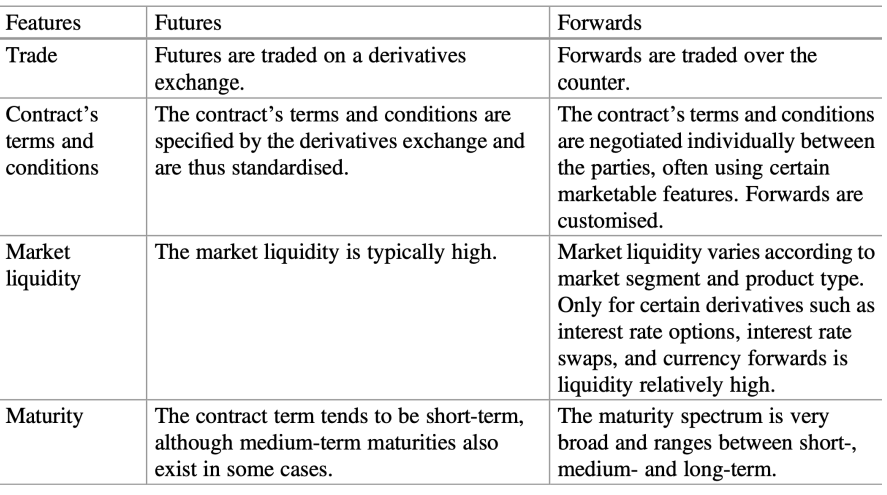

The basic difference between futures and forward contracts is:

- Futures are traded on exchanges (and other trading venues).

- Forwards are negotiated directly between market participants OTC.

This has a number of implications, including:

- Contract standardisation.

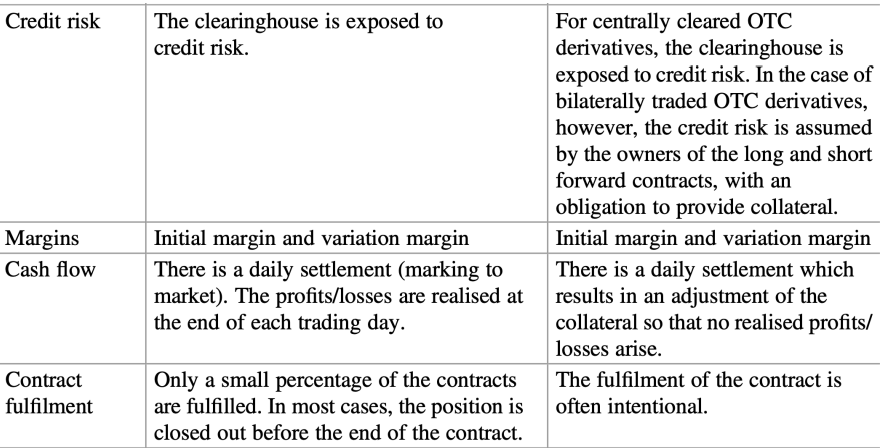

- Centralised counterparty.

- Counterparty risk.

- Trading liquidity and ability to close out positions.

- Holding to maturity vs closing out early.

- Margin mechanism and daily settlement: See below.

- normally doing it with a major bank

- OTC can be very non-standard

- quants trade here, more potential for arbitrage

- futures, trading with the clearinghouse

- obligations are with the clearinghouse - like the intermediary

- more standardised

These differences would seem to entail separate treatments of forwards and futures, but we can show that they can be viewed as equivalent under simplifying assumptions such as frictionless financial markets, constant or deterministic (nonrandom) interest rates, etc.

- So we treat them identically in these notes.

- unrestricted borrowing holdings, no fees, etc we can treat them basically the same

Notation

We use the following notation and terminology throughout these notes:

- We work on a hypothetical time interval .

- Time is a contract’s initiation date.

- Time is a contract’s maturity or delivery date.

- Time is some intermediate date: .

- is the underlying asset’s spot price at time .

- is the contract price at time .

- We write and to reduce notation.

- is the contract multiplier.

- is the notional or face value of 1 contract.

- is the number of contracts we enter into.

Note that it’s very important to be clear about exactly what is.

- is the contract price when initiating a contract at time .

- Long position at time : Agree buy the asset for at maturity .

- Short position at time : Agree sell the asset for at maturity .

The futures prices quoted on exchanges, or the forward price negotiated between parties OTC, is the contract price .

varies over time and is the price you trade futures for. Suppose you:

- Go long contracts at time for .

- Close out your position at time by shorting contracts for .

- The contract prices K and will almost certainly be different!

- You have locked in a payout of at the delivery date T.

Futures trading involves entering into and out of futures contracts over time at different contract prices up to the delivery date .

- Traders typically trade the contract with the closest delivery date, and then roll over into the contract with the next delivery date. The margin mechanism governs your trading profits/losses over time:

decided to buy in your opening position

- locking in different prices

- People typically only trade the futures contract that has the closest maturity date

- not exposed to as much basis risk

- close out your position as it is nearly due for delivery

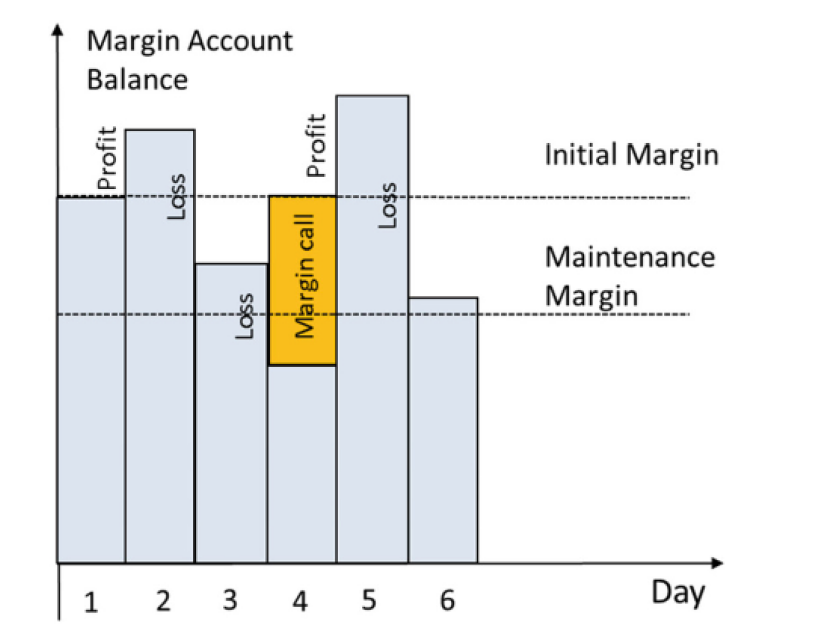

Margin mechanism

The futures margin mechanism can be described as follows:

- You post an initial margin into your margin account, which is a percent of the contract price (per contract).

- Your position is marked to market on a daily basis, with daily gains (losses) credited to (debited from) your margin account.

- There is a maintenance margin, usually less than the initial margin.

- If your margin account falls below the maintenance margin, you get a margin call to top your account back up to the initial margin.

- If you don’t pay it, the exchange closes out your position and your broker will likely “unfriend” you...

- When closing out your position before maturity, your position is immediately marked-to-market using your closing-out price.

- futures exchange requires a margin mechanism

- have to post an initial margin (safety buffer) have money to honor your trade

- between 4-6%

- daily basis, marked to market at COB

- earned a profit, get put into a futures account

Remark

- The above process is often called daily settlement.

- There may be intraday settlement and margin calls.

- You’re free to use the excess funds in your margin account over and above the maintenance margin.

- Daily settlement is the main way exchanges protect themselves against counterparty risk:

- The maintenance margin is typically less than the maximum allowable daily fluctuation or variation in the contract price.

- If the daily variation limit is hit, a circuit breaker or trading halt occurs and all margin accounts are marked-to-market.

- only if large moves in the market

- they won't do anything unless there is money in the margin account

- far less counterparty risk

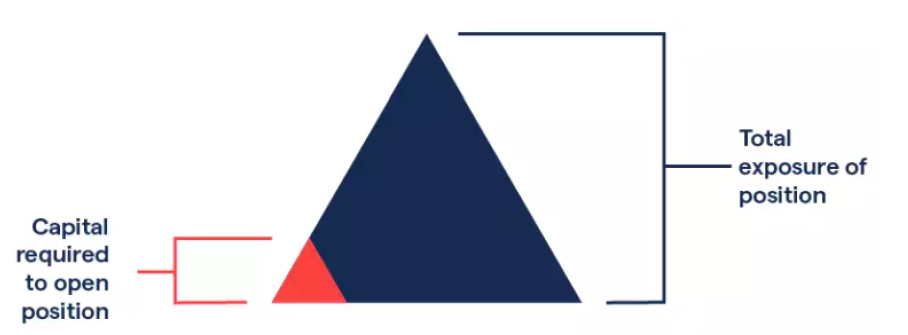

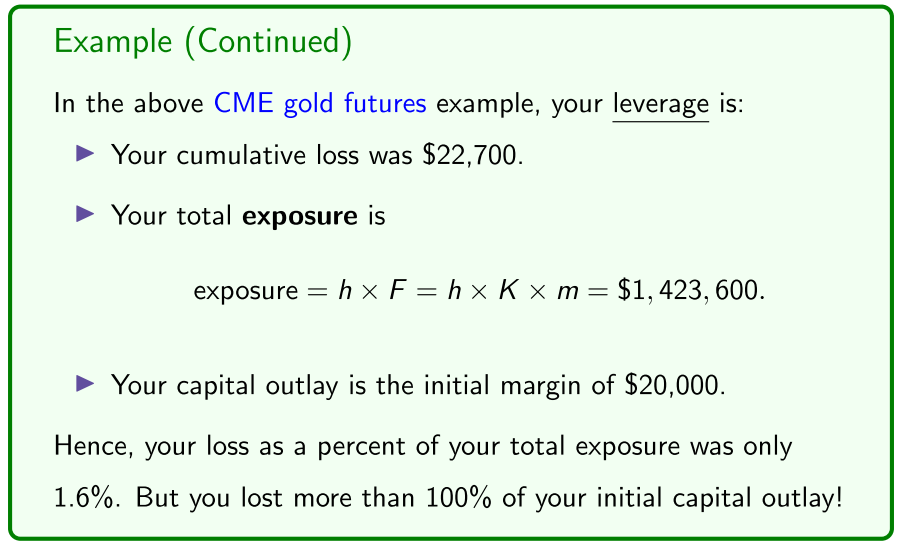

Leverage Effect

Leverage effect: Your profit/loss as a percent of the initial margin.

- The danger with futures is you post only the initial margin upfront:

- Long position: You don’t post the full amount upfront.

- Short position: You don’t need to own the underlying asset.

Don't actually have to post the contract:

- only post the initial margin

- have a massive exposure

Contract value

Another important concept is the value of a futures/forward position at a given point in time that was entered into at time . Suppose you:

- Go long contracts at time for .

- Close your position at time by shorting contracts for .

The cashflow locked in at the delivery date is risk free. With the risk-free rate, the value at time t of a long position is

The value of a short position is thus

ASK TUTOR, WHAT DOES THIS MEAN?

- why do you need beginning e term?

- priced so that they initially have 0 value

- no initial exchange of cash flows

Examples, hedging, speculating

We now cover pricing, speculating and “perfect” hedging with futures contracts over the following general classes of underlying assets:

- Commodities.

- Equities:

- Individual shares and ETFs.

- Share indices.

- Currencies.

- Simple money market interest rates:

- FRA.

- BAB futures.

- main classes of futures and forwards

Commodity futures

Commodity futures are contracts to trade an agreed quantity (and grade/quality) of a commodity for the contract or forward price at the maturity or delivery date .

Futures are written on all kinds of commodities:

- Metals: Gold, silver, copper, aluminium, platinum, nickel, tin, etc.

- Energy and environment: Gas, oil, coal, electricity, carbon, etc.

- Agriculture and food: Beef, pork, milk, wheat, rice, corn, soy, sugar, cocoa, coffee, orange juice, wood, fertiliser, etc.

Many commodity futures are physically settled (but of course can be closed out prior to maturity). Some trading volume statistics:

- most commodity future contracts are physically settled

- don't close out, have to physically trade to collect commodity

Commodity futures “perfect hedging”

To use futures to hedge an exposure to the underlying asset:

- Go long to hedge against prices going up.

- Go short to hedge against prices going down.

lock in the price (either buying or selling) with a futures contract

- using a contract to lock in a certain price, so you are not exposed to price fluctuations in the future

Remark We call this “perfect hedging” since:

- The underlying asset in the contract is exactly the asset exposure we want to hedge.

- The number of units in the underlying asset we want to hedge is covered by an integer number of contracts.

- And our hedge date is exactly the contract delivery date. But things are rarely this “neat” in reality so next week we cover the notion of optimal hedging.

Commodity futures speculating

To use futures to speculate on the direction of the underlying asset:

- Go long if you expect prices to go up.

- Go short if you expect prices to go down. Suppose you go long h contracts at time at K, and then closed it out at time by shorting h contracts at . Your payoff at time is

Long Position payoff

long position payoff =

Short Position payoff

short position payoff =

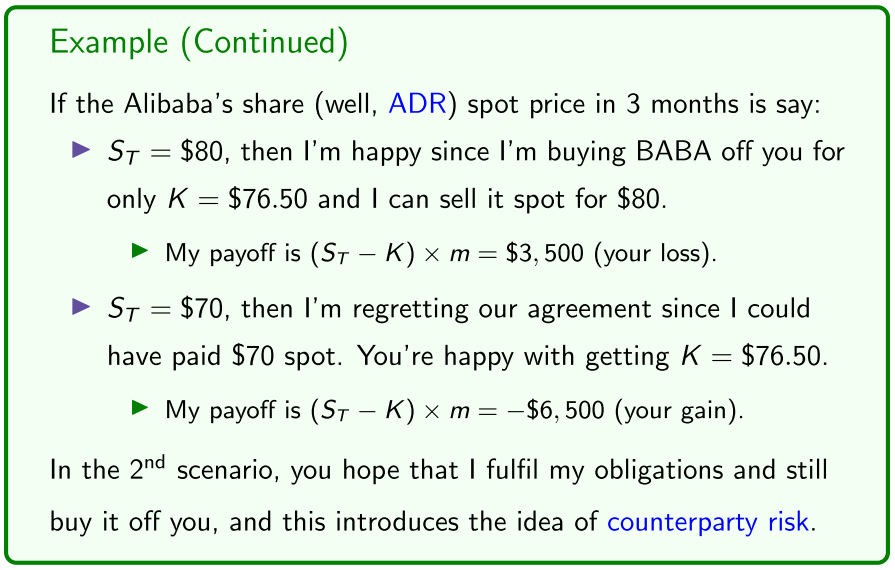

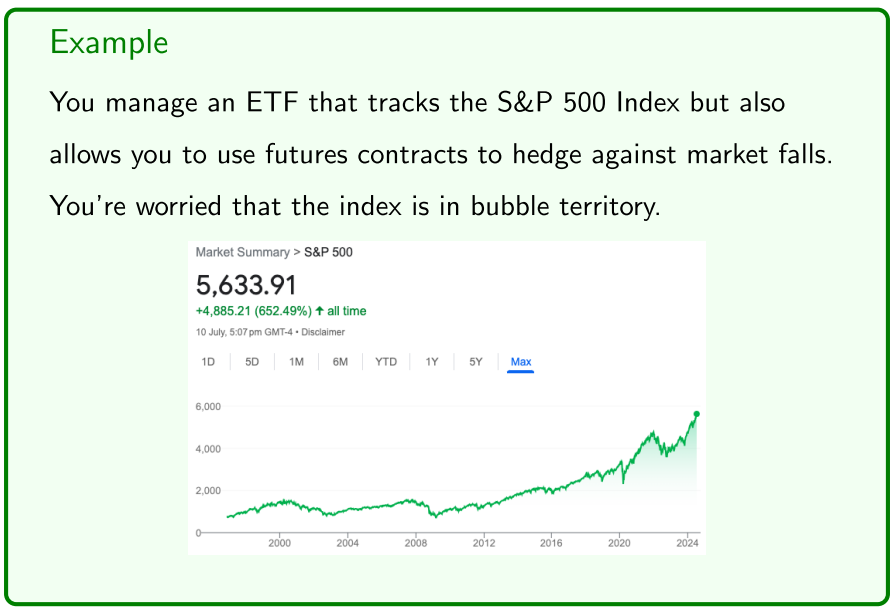

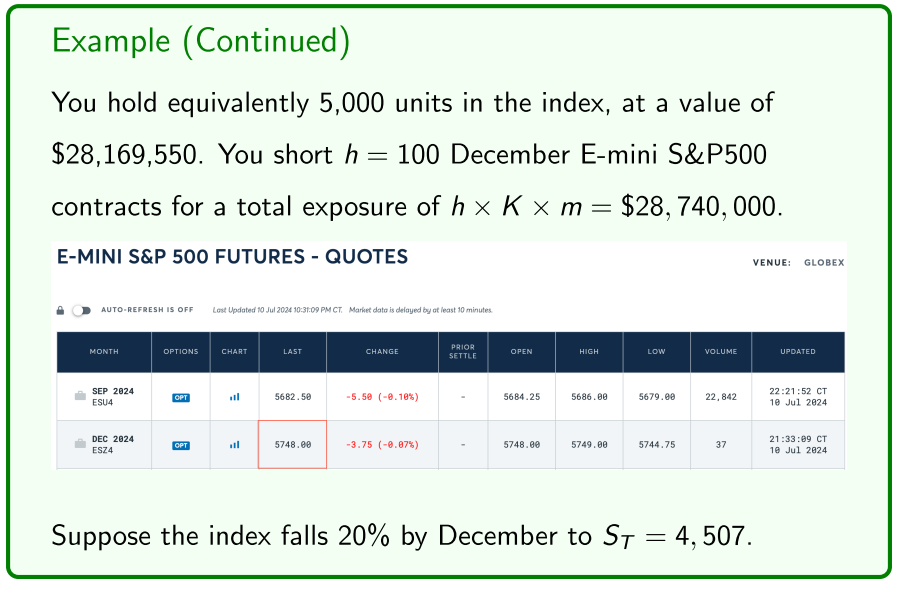

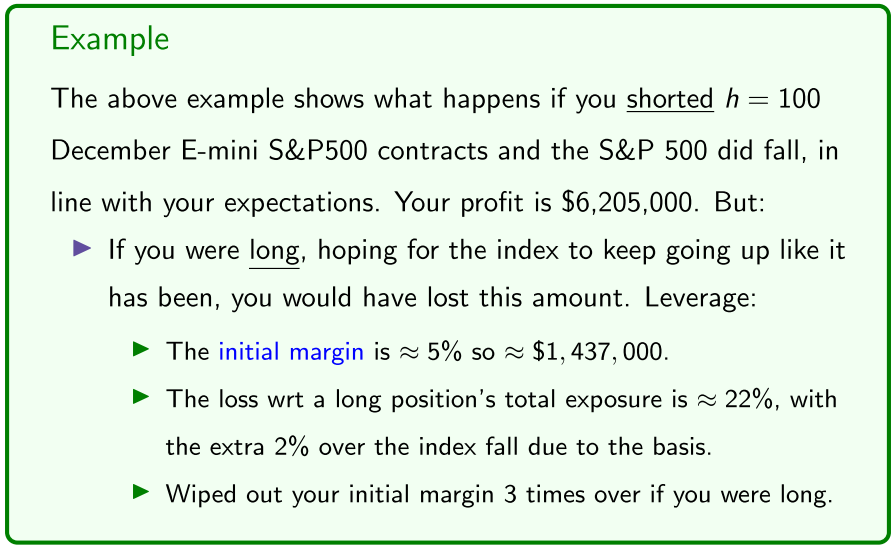

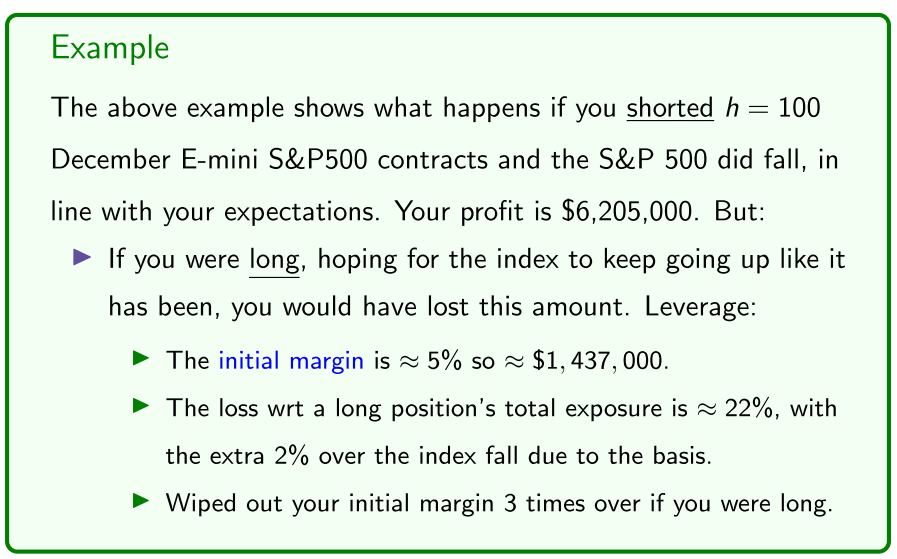

Equity futures

- Share and ETF futures are contracts to trade a quantity of shares in a company or ETF for the contract price at maturity .

- Share index futures are contracts to trade a “share market index” for the contract price (in units of the index) at maturity .

- The notional or face value of a share index futures contract is calculated as , where is the multiplier.

Individual share and ETF futures are typically physically settled but share index futures are usually cash settled (not possible to “trade a whole share index”, but ETF futures effectively enable this). Market statistics:

a little bit more strange, organising to buy/sell a share market index

- not a monetary value, value of the index

- multiplier m

- contract value is the dollar value of S&P500 e.g.

- physically settled

- optimal hedging - minimise the basis risk

Equity futures speculating

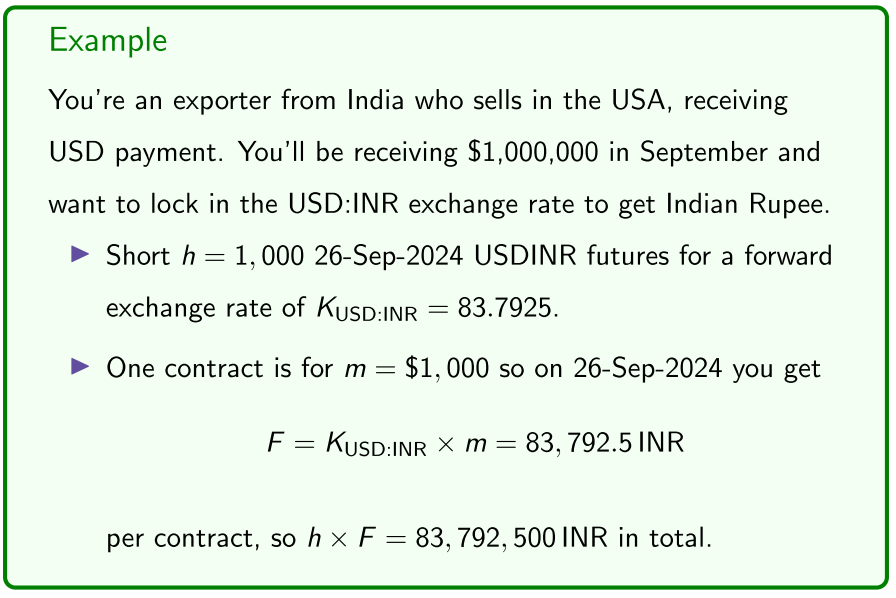

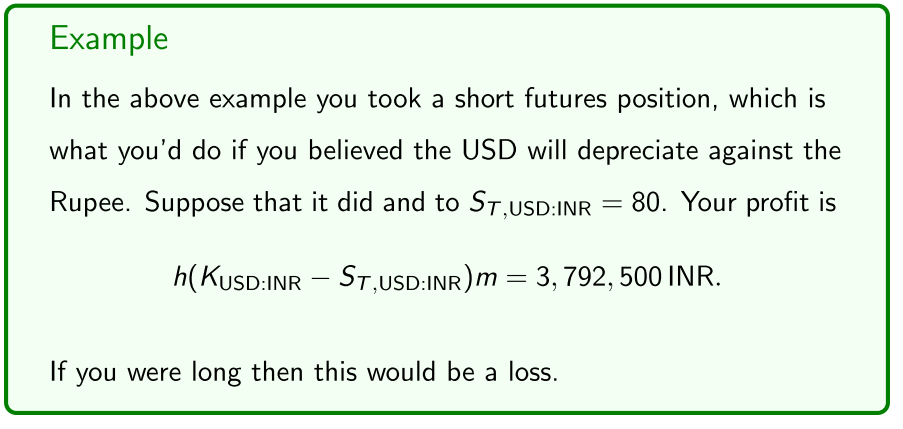

FX futures

Foreign exchange (FX) futures are contracts to exchange an agreed quantity of units in one currency for another currency for the contract price (forward exchange rate) at maturity T.

Our quoting convention for exchange rates is 1 unit of currency exchanges for units of currency . We then have that 1 unit of currency B exchanges for units of currency A.

- careful what we mean by an exchange rate

Remark - FX futures

One way to think about these FX futures quoting conventions is that the foreign currency is being viewed as the “underlying asset”. Thus the futures price is telling us how much Indian Rupee it “costs” to buy 1 unit of the underlying asset.

- In the national stock exchange in India

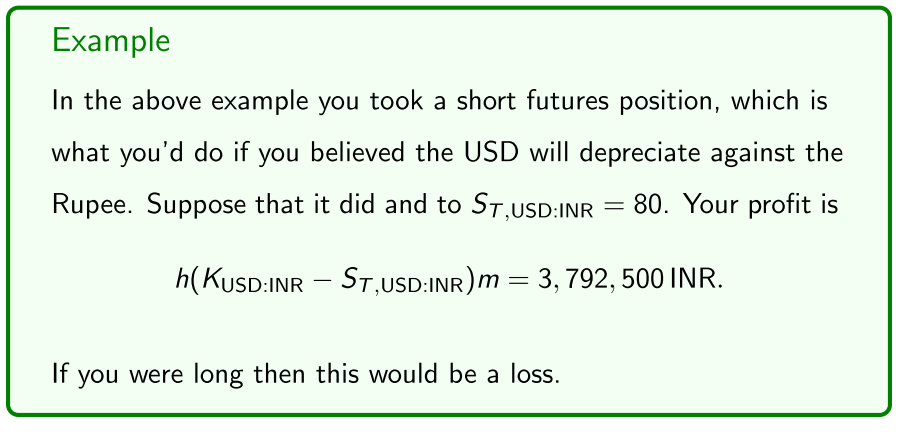

FX futures speculating

Interest rate contracts

We now present two simple interest rate contracts:

- Forward rate agreements (FRA), which are OTC interest rate forward contracts over some global reference rate.

- 90 Day Bank Accepted Bill (BAB) Futures, which are an Australian ASX traded futures equivalent of a FRA over the BBSW rate.

Yield curve, interest rate quoted over the next six months

- work out what the implied forward rate over a period

- lock in interest rate over that period

- must have the same final price

- forward rate agreements, lock in implied interest rate

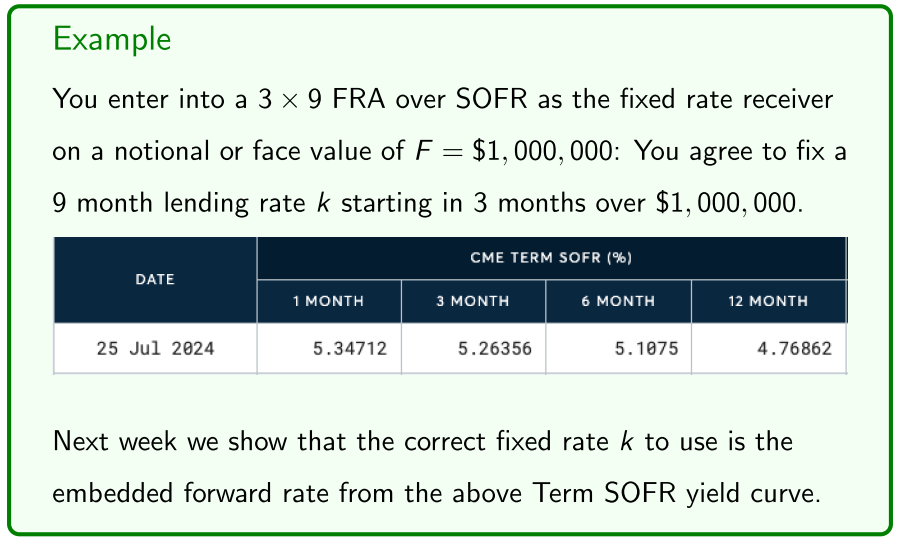

Forward Rate Agreements (FRA)

A forward rate agreement (FRA) is a OTC traded forward contract over a reference interest rate such as SOFR or EURIBOR.

In an FRA the parties agree to fix an interest rate over an agreed notional value for an agreed time period starting on the FRA’s agreed maturity date and ending on .

FRA fix a simple interest rate to begin at maturity for borrowing or lending over the time period of length T, but are cash settled, so no actual borrowing or lending takes place at time .

- A FRA’s payoff at maturity depends on the difference , where is the spot reference rate at time for the period .

- Fix an interest rate, a loan or investment over a given period

- loan or investment, starts on the maturity Get to the maturity date at the enf of the year

- Go long, hypothetical investment over that period

- organising at maturity date, the interest rate you would receive

Payoff

- Interest rate you agree to, versus the spot reference rate (the spot rate at a future time t)

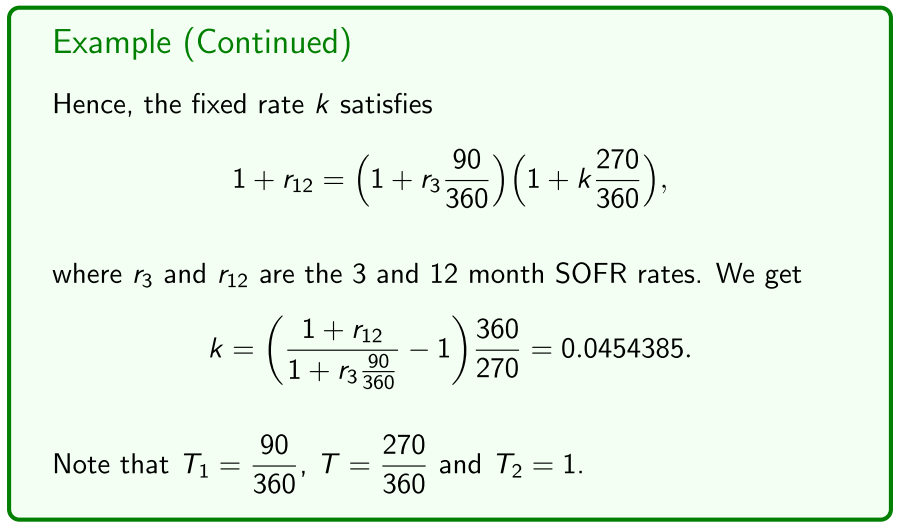

Pricing an FRA involves calculating the agreed upon rate , which we call the fixed rate, and we cover this next week. Using this terminology:

- Being long an FRA involves locking in as a lending or investment rate, and this party is called the fixed rate receiver.

- Think of this as agreeing to lend or invest at maturity, time , and thus to receive the investment proceeds at time .

- Being short an FRA involves locking in as a borrowing or funding rate, and this party is called the fixed rate payer.

- Think of this as agreeing to borrow at maturity, time , and thus to pay off the loan amount of at time .

- long party - fixed rate receiver

- earn interest on an investment

FRA are cash settled, so we want to calculate its payoff, that is, its net cashflow to each party, at maturity . We do it as follows:

- At the FRA’s fixed rate , the amount invested at time to get the agreed cashflow at time is

- But at the spot reference rate at time , the amount invested is

- If the FRA benefits the fixed rate receiver, by .

- If the fixed rate receiver is disadvantaged, by .

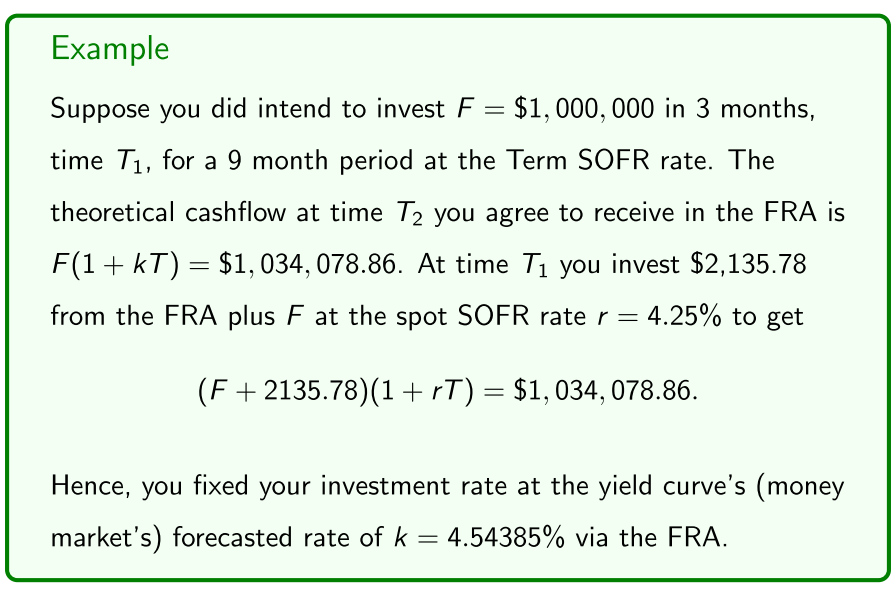

We can easily calculate that The cashflow and thus payoff to the fixed rate receiver at maturity is

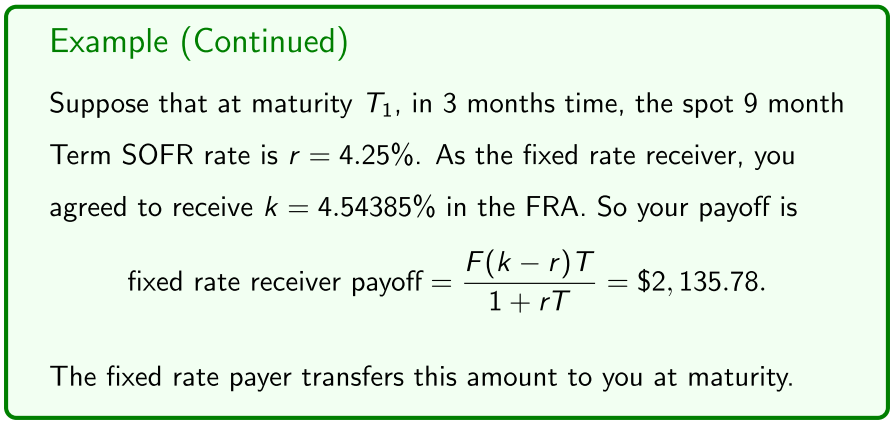

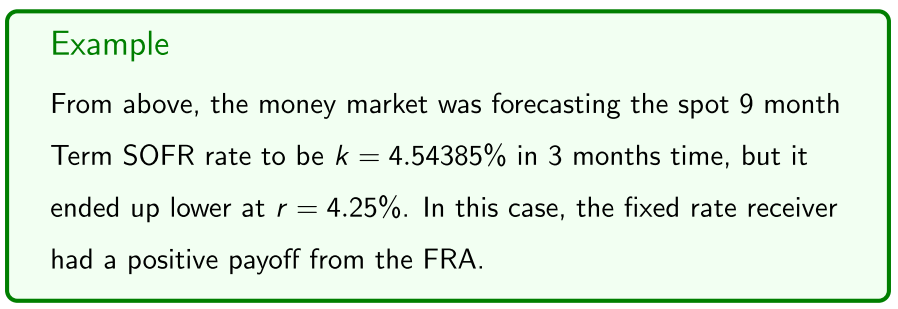

We continue with this example to illustrate hedging with an FRA. Note that the yield curve was forecasting the spot 9 month Term SOFR rate to be k = 4.54385% in 3 months, but it ended up being lower at r = 4.25%

OTC FRA “perfect hedging”

To speculate with FRA, if you expect interest rates to be:

- Lower than the yield curve is forecasting:

- Enter into a FRA as the fixed rate receiver.

- Higher than the yield curve is forecasting:

- Enter into a FRA as the fixed rate payer

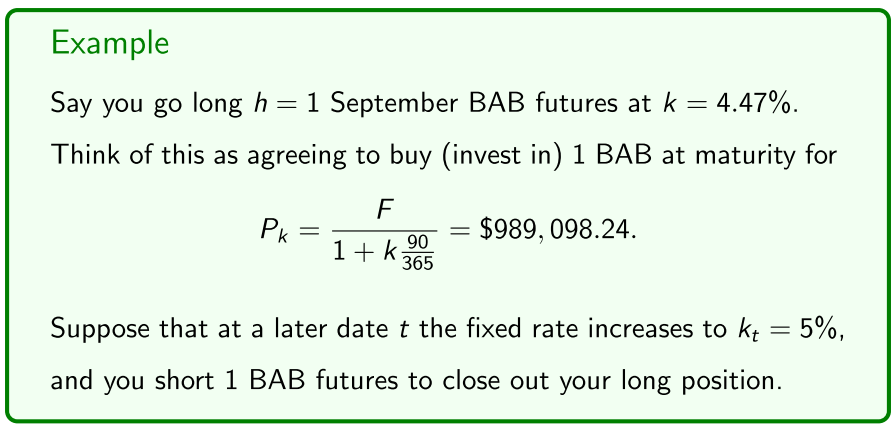

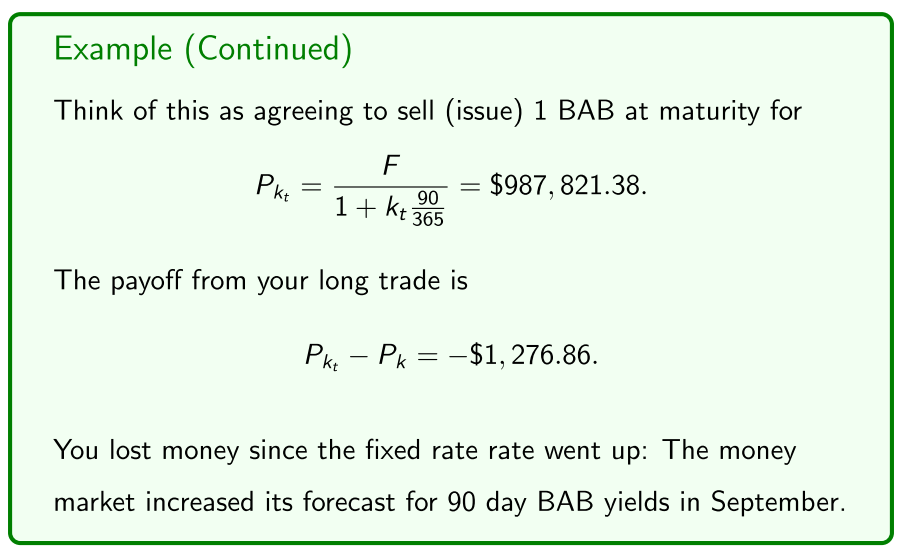

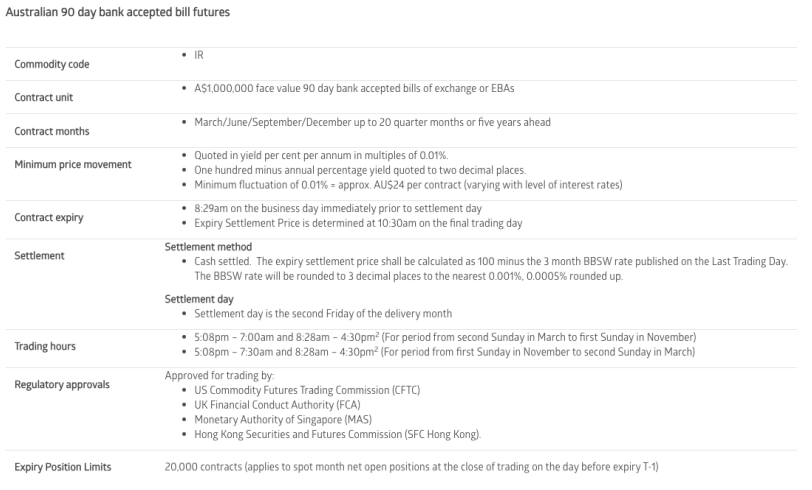

BAB futures

The ASX’s 90 Day Bank Accepted Bill (BAB) Futures contract is effectively a standardised, ASX traded “FRA” but over the Bank Bill Swap (BBSW) rate, which is the main reference rate in Australia. Also:

- You can only lock in the BBSW rate for 90 day periods.

- The BBSW rate’s day count convention divides by 365, the standard day count convention in Australian money markets, so

- The face value of 1 contract is F = $1,000,000 but this refers to the hypothetical cashflow at time , so we use slightly different equations to calculate the values and and hence the net cashflow or payoffs at maturity as we did for FRA:

To calculate the payoffs at contract maturity , let:

- be the fixed rate agreed to in the BAB futures.

- be the spot 90 day BBSW rate at maturity .

At k, the amount invested at maturity to receive F = $1,000,000 at time is

At , this amount is

The payoff at maturity to the fixed rate receiver is:

The payoff to the fixed rate payer is the negative of this.

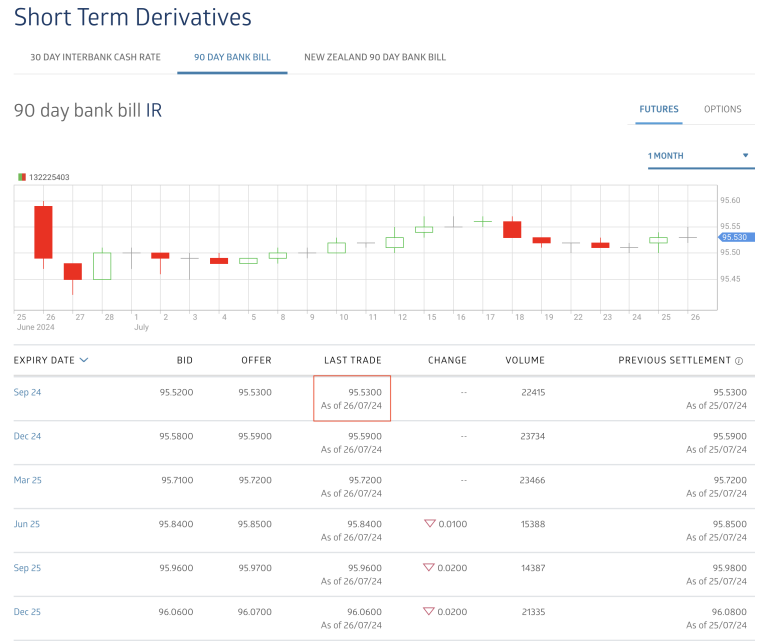

| Contract details | Trade Price |

|---|---|

|

|

Note that BAB futures are quoted as , so the last traded September contract below has fixed rate %:

How would you calculate trading profits/losses in BAB futures?