FINM3405 Revision

Lecture 1 - Basic definitions

Lecture 1

-

- Basic definitions of:

- 1.1 Futures and forwards.

- 1.2 Options.

- 1.3 Swaps

- 1.3.1 interest rate swaps

- 1.3.2 FX swaps

- 1.3.3 currency swaps

- 1.3.4 credit default swaps

-

- Differences between futures and forwards.

- Basic payoff diagrams of futures/forwards and options. (1.1 - 1.3)

-

- Central, foundational, fundamental building block concepts on which all of financial theory and practice are built:

- 3.1. Law of finance and present value (later became risk-neutral pricing).

- 3.2. No arbitrage and the law of one price.

Derivative securities facilitate the management of risks

- The financial system performs its core function of transferring savings and investment funds to long-term investments in real assets.

- Businesses simply go about their usual day-to-day trading activities.

Uses

- Trading, speculation and arbitrage.

- Derivatives can be more efficient and cost effective means by which to speculate on movements in the underlying asset than trading the asset itself

- Risk management or hedging.

- Credit/default and counterparty risk.

- Market risks including adverse movements in interest rates, exchange rates, commodity prices, equity/share prices, etc.

- Government/political/sovereign risk, uncertainty and instability, including changing regulations, elections and military conflict.

- Market making.

- Market makers, and dealers in OTC markets, perform this liquidity function by continuously providing bid and ask quotes in the market for other participants to trade at

- Regulators and other industry bodies and associations.

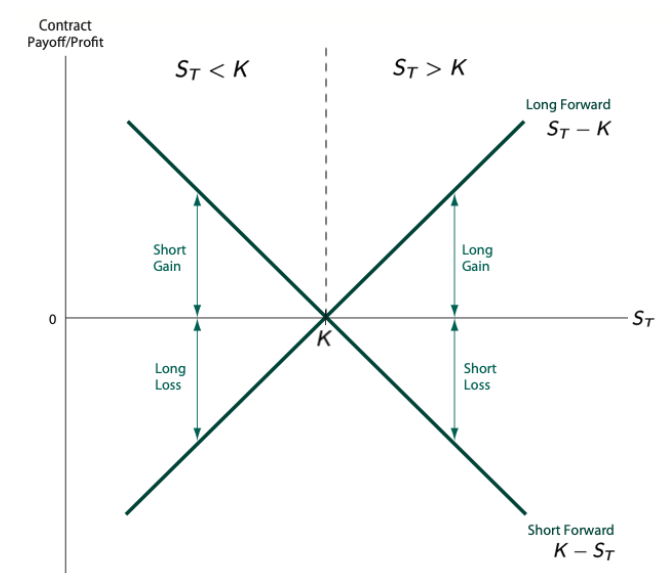

1.1 Futures and forwards

Defn

Futures and forwards are contracts obligating two parties to trade an agreed quantity of the underlying asset for an agreed contract price K on an agreed future date T (the maturity date).

The basic difference between futures and forward contracts is:

- Futures are standardised contracts traded on trading venues (exchange-traded).

- Forwards are negotiated between the parties in OTC markets.

At maturity T, the long party buys the underlying asset for . If at maturity, then the long party has benefited by the amount .

But if at maturity then the short party, who sells the underlying asset for K, has benefited by the amount .

- Hence, the payoffs to the long and short parties are:

long payoff = and short payoff= .

1.2 Options

There are two basic types of option contracts, namely call and put options:

The holder of a European call option has the right but not the obligation to buy an agreed quantity of the underlying asset for an agreed strike price K on an agreed future date T (expiry).

The holder of a European put option has the right but not the obligation to sell an agreed quantity of the underlying asset for an agreed strike price K on an agreed future date T (expiry).

Note that an American option gives the holder these rights to exercise an option at any point up and including the expiry date T.

- The holder of an option is also called the taker, and is said to be long.

- The other party to the contract is called the writer and said to be short.

Expiry - call

European call holder’s payoff at expiry is call holder payoff = max.

Expiry - put

European put holder’s payoff at expiry is put holder payoff = max .

1.3 Swaps

Swaps include:

- Interest rate swaps.

- Foreign exchange (FX) swaps.

- Currency swaps.

- Credit default swaps.

1.3.1 Interest Rate Swaps

A plain vanilla fixed-for-floating interest rate swap involves two parties swapping their existing loan payment obligations:

- One party swaps fixed-rate payments with floating-rate payments.

- They have an existing fixed-rate loan but want to pay floating.

- The other swaps floating-rate payments with fixed-rate payments.

- They have an existing floating-rate loan but want to pay fixed.

Reasons

- Interest rate swaps can help businesses manage interest rate risk

- Enable a business to borrow at terms most favourable to them and then swap their loan to their desired interest rate exposure

1.3.2 Foreign Exchange (FX) Swaps

A foreign exchange (FX) swap is an agreement to exchange one currency for another at an agreed rate on an agreed date and to re-exchange those two currencies at a later date at an agreed rate.

FX swaps are negotiated and arranged OTC.

1.3.3 Currency Swaps

A currency swap is an agreement between two parties to swap interest payments on a loan made in one currency for interest payments on a loan made in another currency.

1.3.4 Credit Default Swaps

A credit default swap is effectively an insurance contract between two parties in which one party purchases protection for a defined period of time from another party against losses from the occurrence of some credit event, usually default of a third party called the reference entity.

- The buyer pays the seller regular premiums, and in return receives a payout from the seller if the reference entity defaults.

- Hence, credit default swaps help businesses manage credit risk, but they’re also used for speculation and arbitrage.

- They are negotiated and arranged OTC.

3. Foundational Concepts

3.1. Law of finance (Present Value)

The value of an asset is the present value of its expected future cashflows.

3.2. No arbitrage and the law of one price

-

A very common approach or technique used in derivative security valuation is to construct a portfolio of more basic securities (such as stocks, bank accounts, simple forwards and futures, etc) which replicates the derivative’s future cashflow structure or payoff.

-

Securities or portfolios with the same future cashflow structure or payoff must have the same price

No Arbitrage

An arbitrage opportunity can be defined in various equivalent ways, and the following two alternative definitions will suffice for this course:

- An arbitrage opportunity is a scenario that has no initial, upfront cashflow or exchange of money, no risk of future loss (negative cashflow), but a chance of a future profit (positive cashflow).

- Keep investing at 0 cost with the possibility of a future profit.

- Alternatively, an arbitrage opportunity is a scenario of two different portfolios or financial securities having the same future cashflow structure or payoff, but different prices.

- Long the cheap and short the expensive security/portfolio.

Neither of these scenarios can last long in efficient financial markets.