Revision lecture, Week 13

- REDE3201 sustainable real estate management

- REDE3102 advanced valuation

- REDE2201

- REDE3100 investment method of valuation

How real estate applied to finance

- How to approach a real estate matter, quote, finance, advise

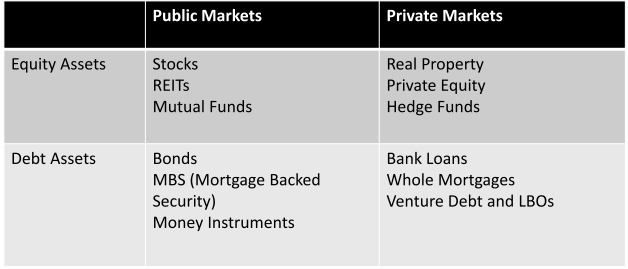

Real Estate as an asset class

- Real Estate - Bundle of Rights Theory

- Ownership (private right enforceable against strangers)

- Possession (possession is 9/10 of the law)

- Control (what is built and what takes place)

- Enjoyment (can use as see fit)

- Exclusion (no trespassing)

- Disposal (sale, lease or by will) & Destruction

- These rights are not unconstrained

- Government controls (ie Planning, Environment, Heritage and Property Laws, Compulsory Acquisition)

- Common law (ie nuisance)

- Self imposed (Contracts – restrictive covenants, leases, mortgages, liens, caveats)

- Not limited to the physical realm

- Relationship between humans and space

- Ownership is a private right

- exclude others and dispose and destroy it

- Communitarian obligations (ownership rights are not absolute)

- permitting, planning, property laws that can take away your laws

- Torts of nuisance, rights are not an absolute ownership

- impose your own constraints on property, lease, restrictive covenant

- Breach of restrictive covenant, might make you tear it down but courts down like it, but courts may award damages

- Conceptual frameworks for property ownership

- Socialist

- Communist

- Capitalist

- Liberal democratic ideology

- Purpose of built form – historic, current and future and how this impacts investment decisions

- Enclosure/delimitation of space

- Climate barrier/modifier

- Protection and privacy

Social frameworks

- grund norm - right of private property

- as a group, want to remove rights that may adversely affect community

- Environmental planning, heritage laws,

Purpose of property and built form

- barrier to climate and modifier of climate

- not subjected to temperature changes

- Privacy

- Communicating an aesthetic appeal

Real estate market characteristics

- Heterogeneous Products

- Real Property is unique

- Immobile Products

- Real estate exists in a defined spatial context

- Buildings can be relocated but land is immovable

- Localised Market

- Markets differ from region to region

- Segmented Market

- Segmentation can be based on use, size/scale and location

- Private negotiations with high transaction costs

- Time consuming, costly and complex

- Defined spacial context

- localised market

- segmented market, cannot make generalisations about the performance of real estate

- Long, complex transactions

Comparison with other asset classes - Why are decisions about property generally more complex and time consuming compared to decisions about other asset classes?

- Size - large capital requirements

- Regulatory environment - high degree of regulatory control and compliance

- Uniqueness

- Time line - long time from inception to use/monetisation

- Property is a wasting asset - depreciation and obsolescence

- Limited liquidity

- Quality of management impacts value

EXAM QUESTION?

- some assets aren't as complicated - talk about the complexities of real estate compared to other asset classes (e.g. commodities)

- size of transaction compared to real estate

- regulatory environment, massive amount of regulatory control and compliance

- air conditioning, controls and measures etc.

- lot of controls you don't have when buying futures

- uniqueness, gold commodity exactly the same, real estate is never exactly unique

- Timeline for doing real estate transactions is really long

- analyse a lot of properties before deciding on one

- a lot of money and time before approvals

- Wasting asset, subject to depreciation and obsolescence

- Limited liquidity, shares in small cap company might be similar

- engagement of good and bad managers

- long WALE, tenancy mix and how long the tenants are staying come down to management

- Portfolio management of shares, compared to asset management

Ownership structures

Doctrine of Tenure (spatial)

- All land is held by way of grant from the Crown (or in modern language from the State)

Doctrine of Estates (temporal)

- All land tenure gives the owner the right of possession for specific duration (an estate can be a future interest – ie vested vs contingent)

- Freehold - uncertain duration

- Fee simple (akin to absolute ownership)

- Fee tail (historical - inheritance limited to certain descendants)

- Life Estate (granted for duration of a person’s life - remainder/reversion)

- Leasehold - certain duration

Doctrine of Waste

- Owners of limited estates (ie less than fee-simple) are limited in their use of the land (ie cant do things to degrade its value) to protect future interests

other than native title land is held by way of the crown

- states that grant it, not the federal government

- One of the residual powers that stayed in federation

- roots back to norman conquests

- Magna carta, bad use of doctrine of tenure without compensation

Doctrine of estates

- Right of possession

- non-exclusive possession for a period of time is a license

Right in REM

- enforce rights against strangers, the whole world

- Distinction between a right and contract and a license to occupy is just a contractual right

- Can only enforce your rights to the party to the contract

Doctrine of waste

- Cannot destroy property if you have less than fee simple

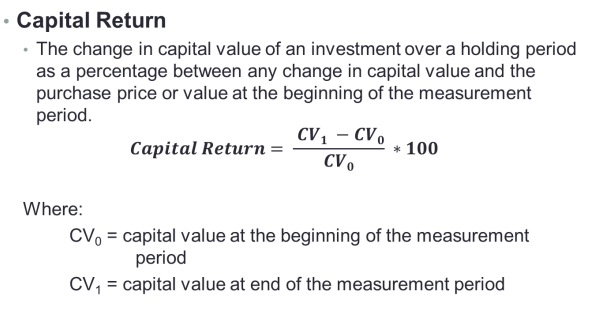

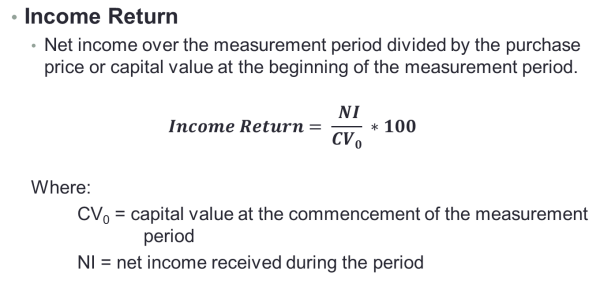

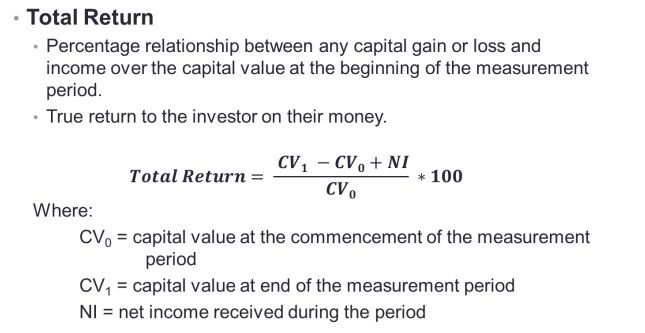

Asset Returns

- meaningful comparisons between property and other asset classes

- Portfolio return:

- Return is a weighted average of expected return on each asset.

- Consider two assets with weights, w

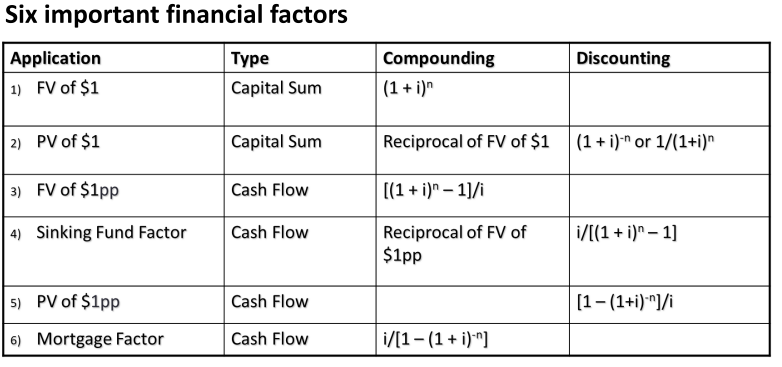

Real Estate Appraisal (Valuation)

What is a valuation and the role of a valuer? Methods of Valuation:

- Direct Comparison

- Summation

- Before and After

- Hypothetical Development (more detail in week 5)

- Discounted Cash Flow (more detail in week 6)

- Units of Production

- Capitalisation method

Direct comparison

- For what a willing and not overly anxious buyer and seller

- Sale may not satisfy those tests

Summation

- summing the component parts of the property

- Depreciate a replacement cost

Before and after

- applies to resumptions

Hypothetical Development

- Often get the sale price at the end wrong

- Get the sales period wrong, how many sell in a particular period

- Sensitivity of getting that wrong is significant

- Deriving the profit and risk rate to work out your development margin

- Knowing cap rate in the end

- Construction costs can be wrong

DCF

- driver terminal value with cap rate

- Escalation factor, how do you know what CPI will be running at?

- Discount rate - what led you to that decision

- investment horizon, massive capital expenditures past investment horizon, skewing investment horizon

- What a representative cash flow model for the performance of the asset

Units of production

- Carrying capacity of a farm, hospital beds, on productive capacity

Cap method

- Capitalising in perpetuity, future net sustainable income at a cap rate derived from evidence of other sales

Capitalisation method

- This valuation method is used for investment class properties

- This method has been widely accepted as being suitable for the estimation of Market Value.

- Under this method, the Future Sustainable Annual Net Income of the subject property is converted to a capital sum (or value) by a market derived multiplier.

- There is a basic assumption that the level of income will remain constant in perpetuity, or at least sufficiently long term to adopt a calculation of the income stream in perpetuity.

Capitalisation Rate

-

Cap rate often referred to as yield or “All Risks Rate”

-

It is a rate that represents all current and future expectations and benefits to be derived from a property.

-

The rate can be used as a benchmark for the comparison of investments

-

Benefits - very simple to use and easy to compare with other assets

-

Challenges – integrity and availability of market data to derive rate

-

The formula used for the Capitalisation Method is:

- Where:

- CV = Capital Value

- NI = Net Annual Sustainable Income (also sometimes called Net Operating Income)

- i = Capitalisation Rate (or Yield)

- The valuer needs to establish:

- The Open Market Rental Rate applicable to the property by reference to market rental evidence.

- The Cap Rate by analysis of recent sales evidence.

- The factor is generally applied to the analysis/valuation of income streams (annuities) from real property held freehold in fee simple which are considered to be enjoyed in perpetuity.

Passing yield and initial yield

Cap rate

- What is my net income after recoverable outgoings

- Net operating income

- Cap rate from industry commentary

Challenges

- market sales evidence

- no single source of data

The Valuation of Varying Incomes

- There are several methods available for the valuation of varying incomes:

1 – Term and Reversion;

- This method capitalises and then aggregates the term and reversionary Incomes. The reversionary value will need to be converted to a present value.

2 – Hard Core Method;

- Under this method, income flows are dealt with as horizontal slices, with passing rent being the “core” income, and future increases due to reviews or reversions being additional slices.

3 – Shortfall Method.

- This method calculates the “loss” of income before market rates are achieved and deducts the value so derived from full market value.

Anything did in tutorials, have a go doing with a calculator and formula EXAM?

- Passing rent is less than market rent, you need to make an adjustment for that period where you have a shortfall in rent or a period where you have an excess in rent

- Allowance before you get to market rent - can use any three methods to make the adjustment

Nature of Development Process

Creative

- Often intuitive

- Especially up-front

- Assimilate multiple inputs

- Importance of networks

Rational

- Often pain-staking

- Multiple constraints to be satisfied

- Optimisation by options and feasibility studies

Creative

- level of basement, car park,

Rational

- reports, environmental assessments

- inputs from various assessment to come up with feasibility

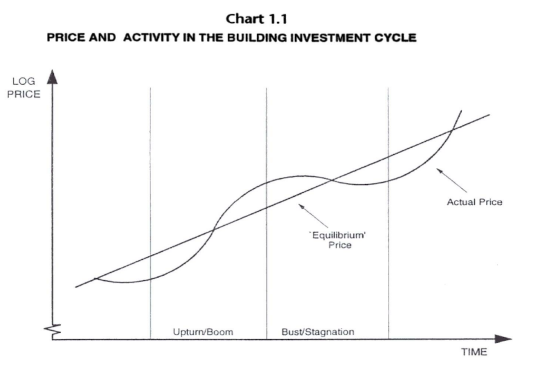

Market cycles

Building Cycle Natural stock cycle

- Fuelled by uncertainty and long lead times

Uncertainty in:

- Underlying demand

- Building activity

- Prospective yields

Cycle - Upturn

- New demand emerges

- Rental prices increase

- Increasing yields attract investors

- Sale prices and activities to rise

- Attracts yield-seeking investment

Cycle - Boom

- Entry of growth capital

- Volatile investment flows

- Rising prices attract new investors, further raising prices

- Developers enter as margins improve

- Over-heated - activity overshoots

- Overvalued prices lower yields

Cycle - Bust

- Oversupply & low rental yields

- Yield-seeking investors withdraw

- Sales, prices & activity fall

- Average prices distorted by forced sales

- Prices flatten (fall in real terms)

- Activity very low as prices below vendor’s expectations

Cycle - Stagnation

- Activities stabilise at lower levels

- Excess stocks absorbed over time

- Lasts until demand gets ahead of stock levels

- One or two year period of massive growth

Building cycle

- yield seeking people coming in

- Building part of the cycle

Upturn

- Rental prices increase because supply hasn't fully taken up the demand yield

- Investors who are looking for good yields come in and activity rises

Boom

- More activity, more people are paying more and yields start dropping down, people are paying more

- Capital growth

Bust

- little capital growth

- Yield seekers leave

- prices flatten and potentially fall

Stagnation

- catalyst comes along, government changes, new demand

- Change in infrastructure,

Cycle Characteristics

Dwellings

- 5-8 years

- Activity upturns of 50-80%

Offices

- up to 15 years

- Activity by 400% during upturn

- Boom can last 6 years

- Price rises of 30-80%

Hypothetical Development Equation

- “Value of Finished Product” = land value + dev costs + finance costs + profit

- Value of Land = Value of Finished Product that is Gross Realisation – (dev costs + finance costs + profit)

Real Estate Financial Modelling

Capital markets - Four Categories

- Ratio of debt to equity in property

Equity Multiple

- Very basic metric

- Doesn’t take into consideration discounting or time value of money

- Its simplicity makes it popular

The equity multiple is arrived at as follows: EM = Er/Ei where: Ei = equity invested Er = total cash returned (income and capital) EM = equity multiple

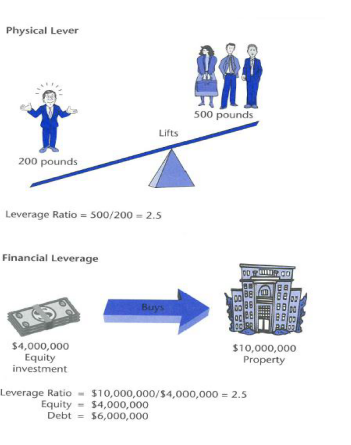

Mechanics of Leverage

- Analogy between financial and physical leverage proves helpful.

- $4m in equity can purchase $10m in property.

- Leverage Ratio = value of underlying asset divided by the value of the equity investment.

- buy more assets with less equity

- If property prices go up greater than the interest that you are spending

Calculating Loan Payments and Balances

-

There are Four Basic Rules for calculating loan payments and balances:

-

Rule 1: The interest owed in each period equals the applicable interest rate times the outstanding principal balance at the end of the previous period

-

Rule 2: The principal amortised (paid down) in each payment equals the total payment (net of expenses and penalties) minus the interest owed

-

Rule 3: The outstanding principal balance after each payment equals the previous outstanding principal balance minus the principal paid down in the payment

-

Rule 4: The initial outstanding principal balance equals the initial contract principal specified in the loan agreement

Possible Exam question

- need to be able to apply them practically

Interest only loan

- Oldest and most basic of loan payments.

- In interest only loan, no amortization of principal

- Outstanding loan balance remains constant throughout the life of the loan

- Entire original principal must be paid back to the borrower in a lump sum (balloon) at the loan’s maturity date.

- Regular loan payments consist purely of interest

- If interest rate is fixed, loan payments will remain constant

Key Features of Mortgage Backed Securities

- Securitisation: process of pooling mortgages

- Tranching: separation of securities into classes

- Bond Credit Rating: the riskiness of an investment

- Other: Loan maturity, waterfall (tiering of creditor payment priority)

Understand what is a mortgage-backed security

- use a bond rating to sell the asset in its own right

Corporate Real Estate & Investment Real Estate

Investment real estate

- I dont care how effective it is as a means of production, as long as it pays rent

- Investment perspective, care about the return on investment

Corporate property

- Land labour capital

- Land being used as an input to production

- means of production for economic activity

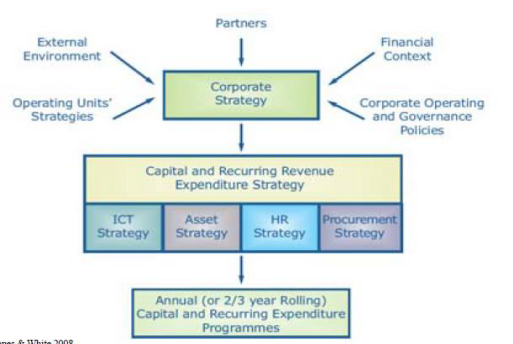

Need to be able to talk to this slide, understand what it means

- How property relates to other elements of businesses

- create value for stakeholders and shareholders

- Existence of property forms corporate strategy

- Have to figure out how they spend money, asset strategy, procurement strategy

- Change procurement strategy, has potential to change their asset strategy or HR strategy

- HR changes, asset classes changes because technology changes

- much more difficult to pivot an asset strategy than it is an ICT or procurement strategy

Question whether or not they are using it in the most profitable or efficient manner

CRE Strategic Framework

- Lease / Own Strategies

- Business Criticality - Portfolio Approach

- Core Accommodation.

- Long lease - own

- Flexible Accommodation

- Lease - medium to short term

- Serviced - Licensed

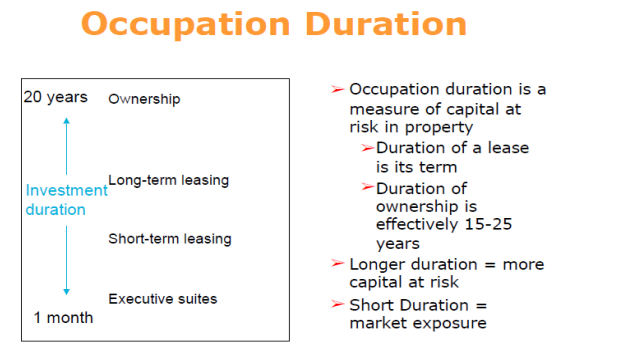

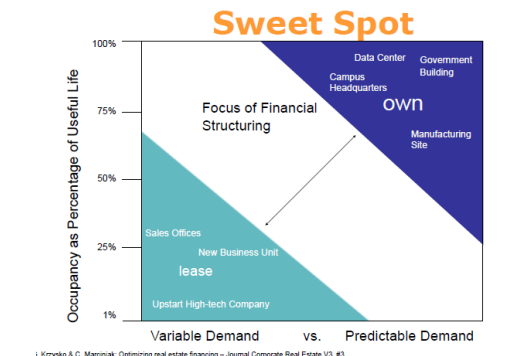

I buy or lease my building, and I asked you, could you answer that question, please? Think whether you can answer that question, you know, if you were asked that, you know, um, you know, if if somebody said well, what what? What? What factors should I consider? We spoke through them. You know, you have a portfolio approach. You have a accommodation approach, you know? Is it core to your business? You know, if it's a long-term requirement, do you lease it? Do you own it? Is it Is it a Is it a short, periodic requirement? Um, is it is it determinable How much you need Or is it likely to be owned? it for? Is it indeterminable? Um, so there are factors which you can consider, you know, the, uh, the duration of occupation. You know how often it lends to your investment decision? What's your availability of capital? Can you actually fund it? Do you have equity to fund it? Do you have debt access to debt? Are you likely to have a long-term lease or is it likely to just be a licence? Or is it likely to be owned? And excuse me, I if you're lucky, you sit in either one of these, um um coloured triangles. If it's a very small percentage of the, um, useful life that you're occupying the building for and it's a very variable demand, you don't own it. It's obvious if it's extremely predictable to and you're using it for the majority of its useful life. It's predictable. It's it's it's obvious you own it, but it's that big, um, white strip in the middle where it's a bit more complicated.

not sure if holding for long enough or predictable enough

There are Two Decisions Involved: Investing & Financing

- Financial management is comprised of two distinct decisions

- Investing decision

- What assets should we acquire?

- Risk v return

- Financing decision

- How should we pay for the assets?

- Financing cost, capital structure considerations

- Investing decision

- Overall objective is to maximize net present value

Not constrained by the capital to fund it or buy it,

How do I maximise the NPV for the business

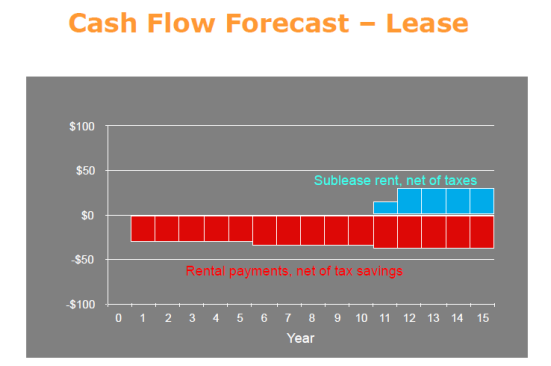

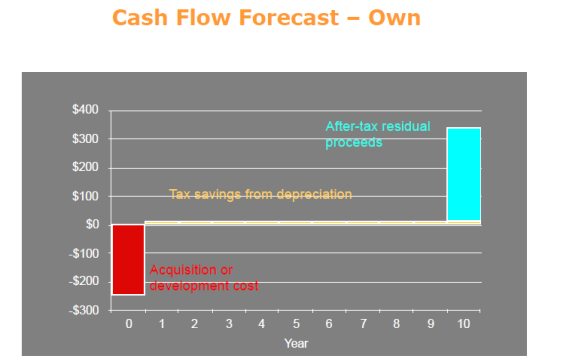

Look at the cash flow modelling from a leasing perspective

Savings from depreciation offset repairs and maintenance

Cash flow from leasing

Choose the more positive Net Present Value

It's better off to own, um, if you if you know what your assumptions are in terms of cost escalations, outgoings, um, future value. You know what your expectations are if you can figure that out cos you spend a whole bunch of money today to buy it, and then you gotta make an assess assessment of what it's worth when you when you cease using it. Um, there is a there is a There is another element to it as well. From a business perspective, um, if you do have the access to capital to buy it, um, you're T you're tying up a whole bunch of your company's equity and your company's, um, debt funding availability, which may preclude you from using equity and debt in other parts of your business. So So you you have this, uh, initial, Can I get the debt and equity by it. If you can't. Well, it's at least,

ESG and Real Estate

- Environmental, Social and Governance – reporting performance of key metrics against benchmarks

- Why does ESG matter in Real Estate

- Availability of funding

- Regulatory compliance

- Consumer behaviour in the space market

- GHG emissions from buildings

- National Framework for Energy Efficiency and Renewable Energy Targets

- Jevon’s Paradox - Improvements in efficiency of resource use can lead to increased consumption of that resource

- GBCA – Green Star Rating

- NABERS – 6 Star System and Commercial Building Disclosure Scheme

- Green Leases – Government National Green Leasing Policy

Company reporting their performance of certain metrics against benchmarks

- CO2, equal pay,

Certain funds who only want to invest in promoting environmental sustainability

Environmental footprint

Consumer behaviour in the space market is stating to mature

- Levers in the market to compare environmental performance

- Consumers can make informed choices

- Companies report their ESG, carbon footprint is lower because they are in spaces which are lower

Building are a massive contributor to greenhouse emissions

National Framework for energy efficiency

Jevon's paradox

GBCA - Green Star Rating

- materially additional or incrementally additional?

- Effectiveness in practise

NABERS - have to disclose rating is greater than 1000m2

Green leases - from governments with 2000m2