Lecture 3

- Exam will only cover the first four weeks of content

Outline

- Risk Management (continued from last week)

- Indirect Ownership Structures

- REITs

- LPTs

- PPPs

- JVs, partnerships, clubs etc

- Modern Portfolio Theory Overview

- Acquisition and Disposal Process

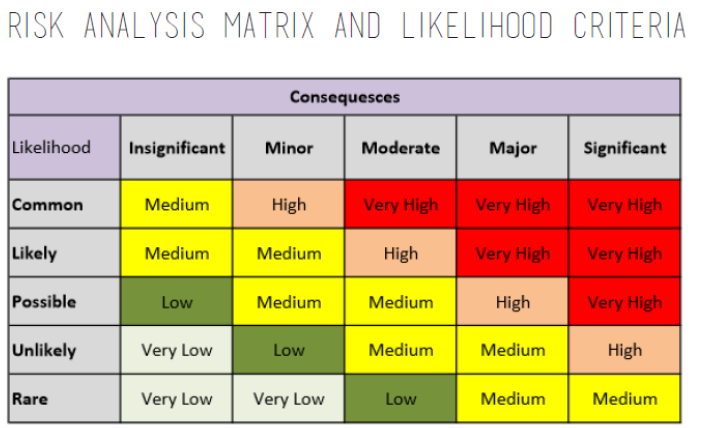

Risk Management

- What is Risk?

- The extent to which an actual outcome is adverse and differs from the expected/predicted outcome

- The probability of the adverse outcome occurring

- NOTE: expect x to happen, what is the likelihood of y happening

- What is a mitigated vs unmitigated risk, and find out how much it costs to mitigate the risk

- Include an opportunity register, contract more for xy etc.

- Risks costs were offset against opportunities you might have

- Risks vs Issues

- Risks are potential adverse outcomes

- Issues are actual adverse outcomes

- NOTE: people often confuse them in projects

- Manage risks and issues differently; risks you monitor, issues you have to put an action in place to manage it.

- Risks aren't real until they become an issue. Risks are potential issues that have a probability of becoming an issue that are used to allocate a costs, but they are not issues.

- Challenge: properly evaluated the risk and pass on many opportunities

- Good property developers don't price the risks originally, and miss many 'potential' risks that never become an issue.

- How do you individually manage all your risks?

- Risk vs Returns

- The greater the degree of risk should correspond with a greater expected return

- Worst risk that can happen is someone dying

- when evaluating a project, which risks do you escalate, mitigate, etc?

- e.g. anything medium or below we just monitor

Financial Risks

- Systematic Risk (beta):

- Variance attributable to the market and influences all assets.

- Example: RBA changes interest rates

- Cannot be diversified away.

- Unsystematic Risk:

- Is asset / firm specific risk and unrelated to the market.

- Example: Balance sheet changes in a firm or vacancy in property asset due to a tenant restructure.

- Diversification is key for the protection against unsystematic risk

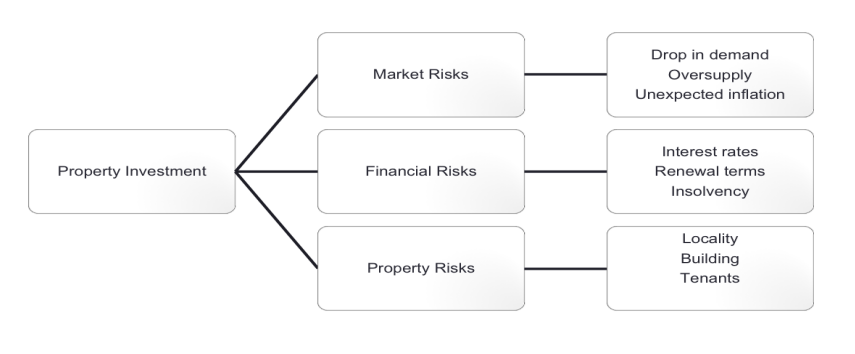

Property Risk

- Risks that affect the property investment but not the market as a whole. May damage location, buildings and tenants.

Risks:

- location rental and capital value impacts: trading potential of a retail store impacted by reduced pedestrian access

- Building failure- unexpected running costs, claims against owners allowing contaminating uses etc

- Soundness or 'covenant' of a tenant - checks on financial stability of a tenant prior to purchasing a property

- Many building risks can be insured against

Other major risks impacting property ownership:

Business Risk

- Business risks due to fluctuations in economic activity that affect the variability of income produced by the property.

- Properties with well-diversified tenant mixes are less subject to business risk

Financial Risk

- Use of debt financing magnifies business risk.

- Degree of financial risk increases as the amount of debt increases and depends on the cost and structure of debt

Liquidity Risk

- Occurs when a continuous market with many buyers and sellers and frequent transactions is not available. The more difficult an investment is to liquidate, the greater the risk that a price concession may have to be given to a buyer should the seller have to dispose of the asset quickly.

- NOTE: Not just a problem which is limited to property

Management Risk

- Most investments rely on management to keep space let and maintained.

- The rate of return that the investor earns can depend on the competency of the management

- NOTE: the quality of the management will directly impact its performance and potential litigation and liabilities

- e.g. outsourced the management of supermarket to a bad management company and the property is never cleaned, more susceptible to TP accidents, e.g.

Interest Rate Risk

- Changes in interest rates will affect the price of all securities and investments.

- Real estate tends to be highly levered, thus, rate of return earned by equity investors can be affected by changes in interest rates.

- rates go up, property prices go back

- Residential real estate is opposing this trend - should have stabilised -> supply not keeping uop with demand

Legislative Risk

- Real estate is subject to numerous regulations such as tax laws, rent control, zoning and other restrictions imposed by government.

- Changes in legislation can adversely affect the profitability of an investment - especially for new development.

- NOTE: legislation impacts property, zoning, environmental heritage. Dealing with three layers of government

- State reserves rights with respect to property law

- Local government have delegated the laws of town planning

- Council makes decisions about planning that impacts peoples lives

Environmental Risk

- Value of real estate is often affected by changes in the environment or sudden awareness that the existing environment is potentially hazardous. E.g. Asbestos

- NOTE: clean up costs with contamination

- Environmental risk can cause more of a loss than other risks mentioned because the investor can be subject to clean-up costs that far exceed the property value.

- NOTE: is there an excessively large 'environmental risk' e.g.

Inflation Risk

- Unexpected inflation can affect an investors expected rate of return if the income of the property does not increase sufficiently to offset the impact of inflation.

INDIRECT OWNERSHIP STRUCTURES

| Retail | Wholesale |

|---|---|

| - Suitable for institutional and “mum and dad” style investors - Minimum investment for syndicates generally $5,000+ | - Designed for large scale sophisticated investors - Investors must qualify under Corporations Act - Minimum Fund investment $500,000+ |

Investor types: Wholesale

Wholesale Investor Types:

- Sophisticated investor:

- Deemed to have sufficient investing experience and knowledge to weigh the risks and merits of an investment opportunity.

- Net assets of at least $2.5m or;

- Gross income for each of last two financial of at least $250,000

- Deemed to have sufficient investing experience and knowledge to weigh the risks and merits of an investment opportunity.

- Professional Investor:

- Australian financial services licensee;

- A body regulated by APRA outside of Superannuation;

- A body registered under the Financial Corporations Act 1974

- Trustees of superannuation funds with assets >$10m

NOTE:

- good projects are fully subscribed or offered to wholesale investors before retail investors

- retail investors tend to get the 'dregs' of bad investment

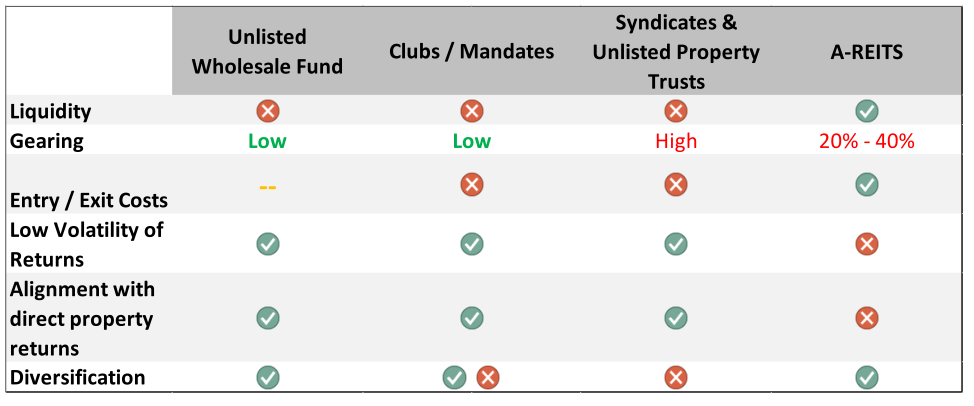

Wholesale Funds: Overview:

- vehicles set up for acquiring 1 or more properties

- normally sector specific

- gearing - the amount of leverage. Typical low and spread across a variety of assets

| No. of Investors | Typically 20 - 50 investors for Funds |

|---|---|

| Minimum Investment | $500,000 upwards |

| Diversification | Usually 10+ assets - Sector specific or diversified across assets |

| Term | Generally open ended |

| Gearing | 0% to 30% for ‘Core’ Funds e.g. Target gearing of 15% to 25% with a maximum of 40% |

-

Institutional investors make investments to wholesale funds based on a view that unlisted private equity format accurately represents the true returns of the underlying real estate assets

-

Wholesale unlisted property trusts are aimed at institutional investors

- Predominantly AU superannuation funds or foreign pension and sovereign wealth funds

- May include Ultra High Net Worth Individuals

-

Each trust tends to have a specific strategy or mandate to invest within a particular sub sector of the real estate market and takes two forms:

- Open-ended vehicles:

- No fixed life, target ‘core’ real estate assets across industrial, retail and office sectors

- Closed-end fixed-life vehicles:

- Invest in higher risk real estate

- Involves value-add opportunities or development projects

- Within life, get these assets and distribute back after 5 years e.g.

- Open-ended vehicles:

Clubs/Mandates

| Info | Description |

|---|---|

| No. of Investors Clubs: | Less than 5 investors - Mandates: Generally 1 investor |

| Typical Investor | Large Super Funds - Insurance Companies - International Institutions |

| Minimum Investment | $50 million upwards |

| Diversification | Usually 5+ Assets - generally target a specific strategy |

| Term | Opportunity specific |

| Gearing | Opportunity Specific |

- Clubs and segregated mandates becoming more popular

- Investors:

- Tend to be large domestic superannuation funds

- Sovereign wealth funds

- International institutions

- Most vehicles no or low gearing

- Particular strategy, particular risk profile ie. Mandate

- Reasons for growth

- Larger investors favour a more hands on approach with asset managers

- Investors are becoming more sophisticated and are looking for specialist skills in asset classes and geographies

- Ability to gain tailored exposure to specific asset classes

NOTES:

- e.g. selling the national broadband network. Mandate might come together to create a management vehicle (fund) under a mandate to acquire a particular fund

- generally needs a lot of money, often no gearing

- reasons for growth, bring in people that have particular skills. Some funds want to partner with entities that have expertise

Syndicates

| Size | $5 million to $50 million |

|---|---|

| No. of Investors | Typically 100+ |

| Typical Investor | Private investors - Self managed super funds |

| Minimum Investment | $1,000 to $10,000 |

| Diversification | Varies from funds with only one asset up to 10+ assets |

| Term | Fixed term investment (typically 5 -7 years) |

| Gearing | Typically 40% to 60% |

-

Closed-end funds with a fixed life expectancy

- Further capital is not raised after initial offering

-

Target high net-worth individuals and SMSF

-

Investors hold their interest until property is sold or rolled over

-

Offer document such as a product disclosure statement (PDS)

-

Repetitive process

- Identify opportunity

- Negotiate structure and investment

- Purchase building

- Raise debt and pool investor equity

-

Individual property strategies

-

Enhanced regulatory focus in recent years

-

Recent resurgence in popularity for syndicates

-

Retail funds management industry is less consolidated

- Lower barriers to entry and wider investment base

- Difficult to identify all players due to small size of typical funds

-

NOTE: directly investing in properties without the capital hurdle

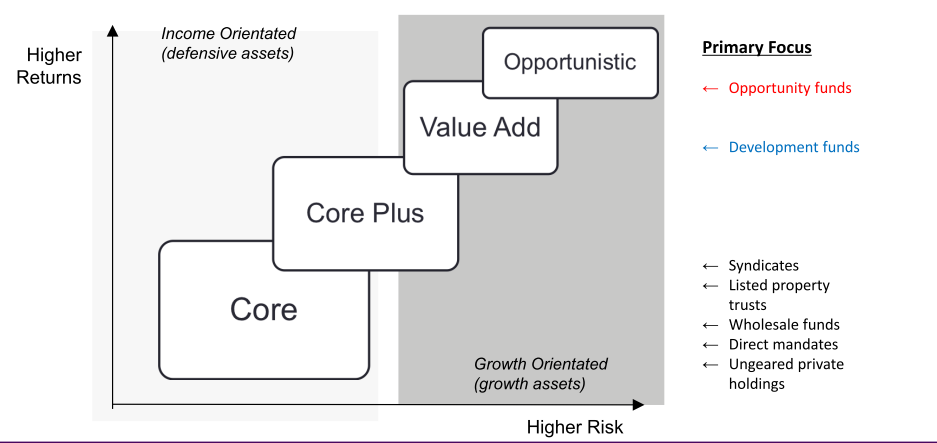

Fund investment strategies

Core

- Primarily invest in:

- Stabilised existing properties

- Current cash flows

- Low vacancy

- Located in major metropolitan areas

- Invest in a wide variety of property types

- Use limited leverage - low risk

Core Plus

- Core plus properties can be a minor component of core fund:

- Core assets in need of minor improvements

- “a B property in an A location”

- Core property that includes current undeveloped land

Value Add:

- Take on more risk by purchasing properties which:

- Carry current vacancies

- Have upcoming major tenant rollovers

- In need of renovation and capital outlay

- Funds create value by renovating and leasing up the property

- Use more leverage compared to core plus

Opportunistic

- Take on even more risk by doing ground up development projects

- Expose the fund to additional construction risks:

- Entitlements

- Construction delays

- Cost overruns

- Complex JV management issues, etc.

- High degree of financial leverage

- May be less diversified and concentrate in certain geographic areas or property types

- Strategy may involve purchasing “distressed property assets”

NOTE:

- not diversified, because you mitigate legislative and planning risk because you have to make sure what you build on there makes a massive profit

- pick a market, council, state, etc.

Investment management fees

-

Fees charged by fund managers generally fall into one/more of the following categories:

-

Acquisition fees charged when each property is acquires and typically a percent of the acquisition cost

-

Disposition fees charged when asset is sold.

-

Performance fees paid as an added incentive to enhance fund performance

- Based on the extend to which the fund managers return exceeds a “hurdle rate of return”

- Typically paid to fund managers to compensate them for taking on additional risks in development or repositioning properties

- Performance fees disappearing from the Wholesale ‘Core’ landscape

-

Management fees:

- Charged to the investor for the entire term of the fund

- Core funds charge base fees on equity capital

- Generally expressed annually as a percentage or basis points (bps)

-

Management fees may be calculated on:

- Committed capital or invested capital

- A percentage of cash flow distributions

- Project Revenues

- Project costs

-

NOTE: property management is very admin intensive

-

fund manager will want more performance fees if exceeds expected performance of the asset

A-REIT

- A Real Estate Investment Trust (REIT) is an investment vehicle that allows investors to purchase an interest in a diversified and professionally managed portfolio of real estate that is listed on the stock exchange.

- A-REITS or Listed Property Trusts (LPT) make up one of the largest sectors on the Australian Stock Market

- A-REITs were established to allow investors to gain exposure to high-grade real estate both domestically and offshore, without the need for large levels of capital, and with the addition of liquidity.

Generates wealth in two ways:

-

They provide exposure to the value of the real estate assets that the trust owns and the accompanying capital growth,

-

as well as rental income.

-

The fund manager selects the investment properties and is responsible for all administration, improvements, maintenance and rental.

-

Some A-REITs specialise in particular sectors, and usually fall into one of the following categories:

- Industrial trusts invest in warehouses, factories, and industrial parks

- Office trusts include medium- to large- scale office buildings in and around major cities

- Hotel and leisure trusts invest in hotels, cinemas and theme parks

- Retail trusts invest in shopping centres and similar assets

- Diversified trusts invest in a mixture of industrial, offices, hotels and retail property.

NOTE

- all day-to-day running of the property

- tend to be sectorised

Why invest in REITS?

- A-REITs have been the preferred property asset class for retail investors and some wholesale investors over direct property.

- The key benefits of investing in A-REITs are:

- Exposure to high quality assets

- Diversification - geographic, sector etc

- High yielding

- Liquidity

- Management efficiency and quality

- Low transaction costs (no stamp duty)

- Corporate governance

- On the negative side – volatility, fee leakage.

NOTES:

- Able to review the efficiency, effectiveness and performance of the management company, lot of information about their costs, how they performed in the past

- low transaction costs - easy to get in and out. If listed, under all the asx rules

- negatives: profit in capital growth or income bled through fees

- Volatility - management is not performing well and you unit is losing value as a result

Fund From Operation (FFO)

There are 5 ways a REIT can grow income and increase funds from operations:

- Growing income from existing properties

- Renting more space

- Raising rent

- Redevelopment

- Growing income through acquisitions

- Growing income through development

- Growing incomes through provision of services

- Financial engineering

- refinancing and allocate resources and capital

REIT characteristics

- Legal Form

- No specific REIT rules in Australia - can be listed or unlisted

- May be sector specific or diversified

- Corporations Act states a REIT must be registered as a Managed Investment Scheme

- No specific REIT rules in Australia - can be listed or unlisted

- Capital Requirements

- No capital requirements for a REIT if listed (but must meet ASX requirements)

- Capital requirements for a manager

- Listing Requirements

- No listing requirements – REITs can be listed or unlisted

- Restrictions on investors

- No investment restrictions on investors

- Restrictions on foreign assets

- No restrictions on foreign assets

- Distribution requirements

- Undistributed income on gains taxed at 46.5%

- gains are taxed at your prevailing personal tax rate

- Full distribution of income and gains by REITS generally occurs

- Undistributed income on gains taxed at 46.5%

REIT Distributions

- Trusts distribute 90% to 100% of earnings

- AREIT trusts do not have franking credits – income is not taxed at trust

- Distributions taxed at the individual income tax rate

- REIT distribution includes a tax deferred component

- Tax deferred component – represents the return of capital rather than income

- Plant and equipment depreciate which reduces taxable income - can be distributed to beneficiaries of the REIT - can get some of the capital back too

- As REITs collect income – manager can decide if the payments made to investor are income collected or capital invested

A-REIT forms

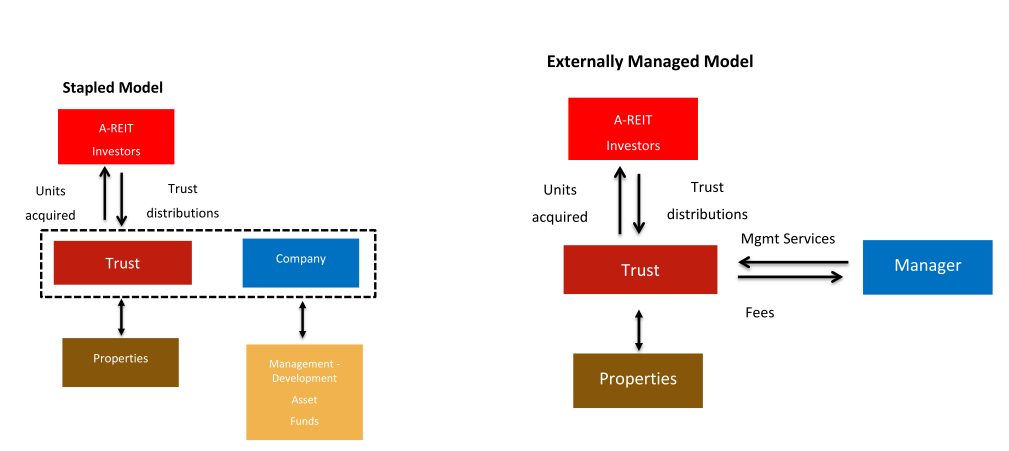

- Broadly speaking, A-REITs comprise one of two forms:

- Externally Managed (passive); or

- Stapled (active).

RHS:

- investors put money into the trust

- trustees purchase properties and hire a manager

- entity managing the property is not necessarily the same as the trustee that owns the property

LHS:

- unit holder holds shares in the trust and the management company

- have an equity position in the company also

- unit in the trust, and shares in the management company

- most common

Stapled securities

- Some trusts adopt hybrid structures called ‘stapled securities’ funds.

- Stapled securities A-REITs provide investors with exposure to a funds management and/or a property development company, as well as a real estate portfolio.

- A share in a stapled securities fund usually consists of one trust unit and one share in the funds management company.

- These securities are ‘stapled’ and cannot be traded separately.

- The trust holds the portfolio of assets, while the related company carries out the fund’s management functions and/or manages any development opportunities.

Externally Managed model:

- Management taken on by separate entity to the property trust

- Slowly collapsing over time

- Often conflicts of interest between management and trust

- Can provide better resourcing and management services than some REITs have capacity for

MODERN PORTFOLIO THEORY

- For many investors income properties are just one part of an investment portfolio:

- May include other properties or asset classes (shares, interest bearing securities)

- The key is that the risk of a property as an isolated investment is greater than the risk the property adds to a portfolio.

- Modern portfolio theory (MPT) has become a well-accepted framework to construct or rebalance real estate portfolios

- MPT assumes investors are risk-averse

- Given two assets offer the same expected return, investors will prefer the less risky one

- Investors will accept increased risk if compensated by higher expected returns

NOTE:

- balancing real estate portfolios

- assets with different risks and returns, when aggregating them you are overall mitigating aggregate risk

- By balancing multiple assets with different risk profiles, you overall have a better risk portfolio and better risk management

Asset Returns

- Total (Accumulation) Return accounts for two categories of return: income and capital

- Income includes interest paid by fixed-income investments, distributions dividends or the net income of direct property

- Capital/ Price return represents the change in the market price of an asset.

- income and capital

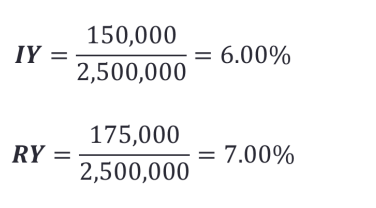

- Initial Yield

- The income yield for the asset. Shows the ratio of the current passing rent to the current property value

- IY = passing rent / property value

- passing yield - how much rent I am currently versus from the current property value

- The income yield for the asset. Shows the ratio of the current passing rent to the current property value

- Reversionary Yield

- The market yield for the asset. Shows the ratio of the market rent to the current property value (on properties rented below market)

- RY = market rent / property value

- what is the market rent of the property value

- reversionary - at the end of the lease term, the right to possess the property reverts back to the owner

- in a perfect world, initial yield and reversionary yield is the same

Income return

A property is valued at $2.5m and has a current net income of $150,000 p.a. The assessed market income for the property is $175,000 p.a. Compute the initial yield and reversionary yield for the asset.

Capital Return

The change in capital value of an investment over a holding period as a percentage between any change in capital value and the purchase price or value at the beginning of the measurement period.

Capital Return=

Income Return

- Net income over the measurement period divided by the purchase price or capital value at the beginning of the measurement period.

Income return =

Total Return

Percentage relationship between any capital gain or loss and income over the capital value at the beginning of the measurement period.

- True return to the investor on their money.

Total return =

CV = capital value at the beginning of the measurement period CV1 = capital value at end of the measurement period NI = net income received during the period

- Over time, land tends to appreciate while building depreciate

- If the majority of the value is attributed to the build component, over time the future capital value will be a small part of it increasing the land and a large part decreasing the value

- common to have small income (and small building) but large capital component or other way around

Asset Yields vs Asset Returns

- Yield reflects the relationship between a current net income and the purchase price and does not take into account any capital loss or gain made.

- Return usually reflects any income, expenditure and/or capital gain or loss made on investments.

- Return gives a clear indication of the financial position of the investor.

- Yields are used to estimate the market value of an investment while a return is used as a means of comparing the financial attractiveness of different investments to an investor.

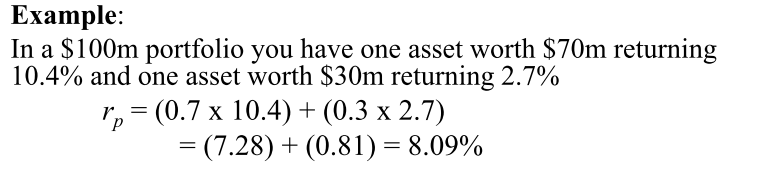

Portfolio returns

- Return is a weighted average of expected return on each asset.

- Consider two assets with weights, w 1 w 2 and returns r 1 r 2 .

Portfolio return:

Acquisition and Disposal process

-

Direct or indirect ownership decision

-

Timing – what stage of the property cycle do you buy into?

-

Asset physical characteristics

- Segment

- Size

- Location

- Age and condition of improvements

-

Financial characteristics

- Hurdle rate for return on investment/return on capital

- WALE (weighted average lease expiry)

- Income and capital growth opportunities

-

process purchasing every kind of infrastructure, e.g.

-

timing - hot market, buying/selling market will impact due diligent time frames etc.

-

WALE - 100 leases expiry at the end of year, WALE is one year. Average the lease expiry

- can also weight based on income too, or how much space is becoming available

Acquisition Process

Typical Expression of Interest process (can be over 12 months)

- Initial Review of an Asset

- Engage Consultants

- First Round Bids

- Second Round Bids

- Third Round Bids

- Due Diligence

- Contract Signing

- Settlement

- normal process to acquire a project

- 12 months is not an unusual EOI

- Initial Review of an Asset

- Meet with agents to discuss opportunity

- Review of Information Memorandum

- Initial Pricing of Asset based on Financial Pack - Budget, Outgoings recovery model, Tenancy Schedule

- Initial review of documents provided in data room

- Multiple pricing scenarios and sensitivity analysis

- not uncommon to pay $50-150K for an unsuccessful property purchase

- Engage Consultants

- Usually only applicable in complicated transactions such as large scale retail for a market / trade area analysis

- First Round Bids

- Submission of First Round Bids to Agents

- Includes price and terms

- i.e. $80,500,000, subject to FIRB Approval, subject to Board Approval, 60 day settlement, subject to Due Diligence period of 4 weeks etc etc

- NOTE: look at them, how compliant are they to community objective, etc. Aligns to policy objective to what the seller has outlined

- Second Round Bids

- Shortlisted parties (usually 3) are invited to provide a second round bid

- Usually a higher/ more competitive bid based on sensitivity analysis, market assessment undertaken throughout first round bids and assumption clarification

- 3rd Round Bids (BAFO – Best and Final Offer)

- Only applicable in very competitive markets

- Not always applicable in the bid process - subject to vendor and agent’s preference

- Due Diligence

- Often 4 - 6 weeks

- Hot / competitive market is reducing DD periods to 4 weeks or less

- Some transactions in the market have taken place with no DD

- Allows for detailed analysis of financial, technical and legal review of the asset

- Contract Signing

- Property sale contract signed by all parties

- Settlement

- Settlement varies dependent on vendor and purchaser preferences

- Often 30 - 60 days

- Can be as long as 6 months

Typical Due Diligence Checklist

- Rent Roll Analysis

- Lease Agreement Review

- Review of Service and Maintenance Agreements

- Pending or threatened matters review

- Review of Title/deed documents

- Property Survey

- Government Compliance

- Physical Inspection

- Tax Matters

- Insurance Policies

- Engineering studies

- Market studies

- List of personal property

Divestment Criteria

- Reposition of Fund

- Too much retail in a Fund benchmarked against diversified assets. i.e. high capital returns in funds invested in Sydney/ Melbourne office markets have increased the return benchmark for funds that might carry too much retail (lower total returns compared to certain office markets)

- Cyclical Play - i.e. Office Market - buy low, sell high

- Closed end Fund

- requires divestment of assets at the end of the Fund

- Capital Requirements

- Liquidity windows and unit redemption may force sale of assets

- sell assets to offset leverage

- Liquidity windows and unit redemption may force sale of assets

Disposal Process

- Internal Approvals

- Internal Board and Investment Advisory Committee Approvals

- Data Collection

- Collection of all documents relating to the asset

- Leases, management agreements, service contracts, maintenance records, tenant tax invoices, dispute notices

- Internal Valuation of the Asset

- Multiple pricing scenarios to target marketing date, use for recommendation of divestment.

- Due Diligence

- Validation of all documents related to asset

- Can be 2,000 - 3,000 documents requiring validation

- Agency Appointment

- Agency submissions and appointment of successful agent

- Agent’s domestic and international reach taken into consideration as well as fees

- One or two agents dependant on size of transaction

- Launch Campaign

- International campaign typically 1-2 weeks ahead of domestic campaign

- Campaign length typically 4 weeks domestically

- Bid Submissions

- Bid submissions taken and parties shortlisted

- Second Round Bids

- Shortlisted parties invited to submit second round bids

- Parties shortlisted dependant on bid price, terms, perceived settlement risk

- Due Diligence

- Contract Signing

- Settlement

- data rooms, partially redact data and can see what data the other entity has accessed