Lecture 3 Revision - Important Concepts

Real Estate Ownership Structures Pt2

INDIRECT OWNERSHIP STRUCTURES

| Retail | Wholesale |

|---|---|

| - Suitable for institutional and “mum and dad” style investors - Minimum investment for syndicates generally $5,000+ | - Designed for large scale sophisticated investors - Investors must qualify under Corporations Act - Minimum Fund investment $500,000+ |

Investor types: Wholesale

Wholesale Investor Types:

- Sophisticated investor:

- Deemed to have sufficient investing experience and knowledge to weigh the risks and merits of an investment opportunity.

- Net assets of at least $2.5m or;

- Gross income for each of last two financial of at least $250,000

- Deemed to have sufficient investing experience and knowledge to weigh the risks and merits of an investment opportunity.

- Professional Investor:

- Australian financial services licensee;

- A body regulated by APRA outside of Superannuation;

- A body registered under the Financial Corporations Act 1974

- Trustees of superannuation funds with assets >$10m

Wholesale Funds: Overview:

| No. of Investors | Typically 20 - 50 investors for Funds |

|---|---|

| Minimum Investment | $500,000 upwards |

| Diversification | Usually 10+ assets - Sector specific or diversified across assets |

| Term | Generally open ended |

| Gearing | 0% to 30% for ‘Core’ Funds e.g. Target gearing of 15% to 25% with a maximum of 40% |

- Institutional investors make investments to wholesale funds based on a view that unlisted private equity format accurately represents the true returns of the underlying real estate assets

- Wholesale unlisted property trusts are aimed at institutional investors

- Predominantly AU superannuation funds or foreign pension and sovereign wealth funds

- May include Ultra High Net Worth Individuals

Clubs/Mandates

| Info | Description |

|---|---|

| No. of Investors Clubs: | Less than 5 investors - Mandates: Generally 1 investor |

| Typical Investor | Large Super Funds - Insurance Companies - International Institutions |

| Minimum Investment | $50 million upwards |

| Diversification | Usually 5+ Assets - generally target a specific strategy |

| Term | Opportunity specific |

| Gearing | Opportunity Specific |

- e.g. selling the national broadband network. Mandate might come together to create a management vehicle (fund) under a mandate to acquire a particular fund

- Bring in people that have particular skills. Some funds want to partner with entities that have expertise

Syndicates

| Size | $5 million to $50 million |

|---|---|

| No. of Investors | Typically 100+ |

| Typical Investor | Private investors - Self managed super funds |

| Minimum Investment | $1,000 to $10,000 |

| Diversification | Varies from funds with only one asset up to 10+ assets |

| Term | Fixed term investment (typically 5 -7 years) |

| Gearing | Typically 40% to 60% |

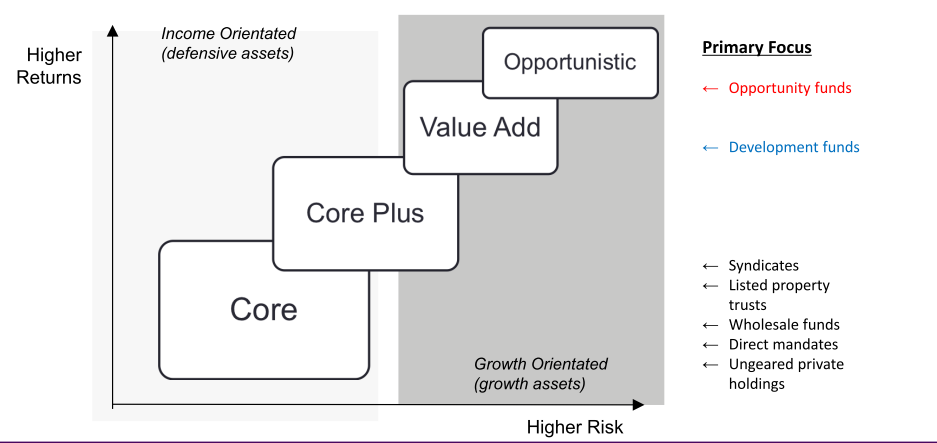

Fund investment strategies

Core

- Primarily invest in:

- Stabilised existing properties

- Current cash flows

- Low vacancy

- Located in major metropolitan areas

- Invest in a wide variety of property types

- Use limited leverage - low risk

Core Plus

- Core plus properties can be a minor component of core fund:

- Core assets in need of minor improvements

- “a B property in an A location”

- Core property that includes current undeveloped land

Value Add:

- Take on more risk by purchasing properties which:

- Carry current vacancies

- Have upcoming major tenant rollovers

- In need of renovation and capital outlay

- Funds create value by renovating and leasing up the property

- Use more leverage compared to core plus

Opportunistic

- Take on even more risk by doing ground up development projects

- Expose the fund to additional construction risks:

- Entitlements

- Construction delays

- Cost overruns

- Complex JV management issues, etc.

- High degree of financial leverage

- May be less diversified and concentrate in certain geographic areas or property types

- Strategy may involve purchasing “distressed property assets”

A-REIT

- A Real Estate Investment Trust (REIT) is an investment vehicle that allows investors to purchase an interest in a diversified and professionally managed portfolio of real estate that is listed on the stock exchange.

- A-REITs were established to allow investors to gain exposure to high-grade real estate both domestically and offshore, without the need for large levels of capital, and with the addition of liquidity.

REIT characteristics

- Legal Form

- No specific REIT rules in Australia - can be listed or unlisted

- May be sector specific or diversified

- Corporations Act states a REIT must be registered as a Managed Investment Scheme

- No specific REIT rules in Australia - can be listed or unlisted

- Capital Requirements

- No capital requirements for a REIT if listed (but must meet ASX requirements)

- Capital requirements for a manager

- Listing Requirements

- No listing requirements – REITs can be listed or unlisted

- Restrictions on investors

- No investment restrictions on investors

- Restrictions on foreign assets

- No restrictions on foreign assets

- Distribution requirements

- Undistributed income on gains taxed at 46.5%

- gains are taxed at your prevailing personal tax rate

- Full distribution of income and gains by REITS generally occurs

- Undistributed income on gains taxed at 46.5%

REIT Distributions

- Trusts distribute 90% to 100% of earnings

- AREIT trusts do not have franking credits – income is not taxed at trust

- Distributions taxed at the individual income tax rate

- REIT distribution includes a tax deferred component

- Tax deferred component – represents the return of capital rather than income

- Plant and equipment depreciate which reduces taxable income - can be distributed to beneficiaries of the REIT - can get some of the capital back too

- As REITs collect income – manager can decide if the payments made to investor are income collected or capital invested

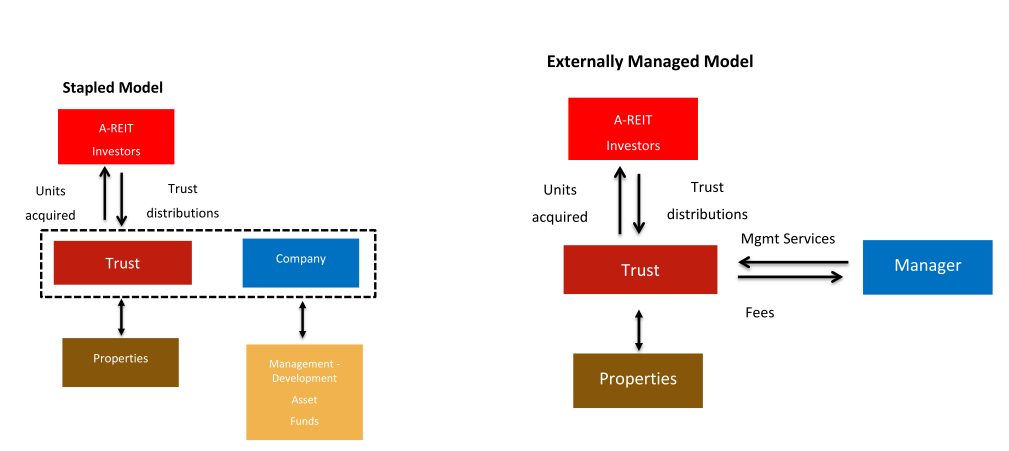

A-REIT forms

- Broadly speaking, A-REITs comprise one of two forms:

- Externally Managed (passive); or

- Stapled (active).

RHS:

- investors put money into the trust

- trustees purchase properties and hire a manager

- entity managing the property is not necessarily the same as the trustee that owns the property

LHS:

- unit holder holds shares in the trust and the management company

- have an equity position in the company also

- unit in the trust, and shares in the management company

- most common

Stapled securities

- Some trusts adopt hybrid structures called ‘stapled securities’ funds.

- Stapled securities A-REITs provide investors with exposure to a funds management and/or a property development company, as well as a real estate portfolio.

- A share in a stapled securities fund usually consists of one trust unit and one share in the funds management company.

- These securities are ‘stapled’ and cannot be traded separately.

- The trust holds the portfolio of assets, while the related company carries out the fund’s management functions and/or manages any development opportunities.

Externally Managed model:

- Management taken on by separate entity to the property trust

- Slowly collapsing over time

- Often conflicts of interest between management and trust

- Can provide better resourcing and management services than some REITs have capacity for

Modern Portfolio Theory

Capital Return

The change in capital value of an investment over a holding period as a percentage between any change in capital value and the purchase price or value at the beginning of the measurement period.

Capital Return=

Income Return

- Net income over the measurement period divided by the purchase price or capital value at the beginning of the measurement period.

Income return =

Total Return

Percentage relationship between any capital gain or loss and income over the capital value at the beginning of the measurement period.

- True return to the investor on their money.

Total return =

CV = capital value at the beginning of the measurement period CV1 = capital value at end of the measurement period NI = net income received during the period

Initial Yield and Reversionary Yield

Initial Yield

- The income yield for the asset. Shows the ratio of the current passing rent to the current property value

- IY = passing rent / property value

- passing yield - how much rent I am currently versus from the current property value

Reversionary Yield

- The market yield for the asset. Shows the ratio of the market rent to the current property value (on properties rented below market)

- RY = market rent / property value

Example A property is valued at $2.5m and has a current net income of $150,000 p.a. The assessed market income for the property is $175,000 p.a. Compute the initial yield and reversionary yield for the asset.

Asset Yields vs Asset Returns

- Yield reflects the relationship between a current net income and the purchase price and does not take into account any capital loss or gain made.

- Return usually reflects any income, expenditure and/or capital gain or loss made on investments.

- Return gives a clear indication of the financial position of the investor.

- Yields are used to estimate the market value of an investment while a return is used as a means of comparing the financial attractiveness of different investments to an investor.

Portfolio returns

- Return is a weighted average of expected return on each asset.

- Consider two assets with weights, w 1 w 2 and returns r 1 r 2 .

Portfolio return: