Lecture 5

VALUATION METHODOLOGIES

The Lessor:

- The lessor has a right to receive rental and other income from the property under the terms of the lease. Once the lease has expired, the property reverts to the full control of the lessor who can then relet the property at the prevailing full market rental rates.

- The income derived from the lease can be capitalised to establish the value of the based on the lease term.

- The potential income at lease expiry is known as the Reversionary Income which can then be capitalised in perpetuity to establish the reversionary value of the property at that time.

Only income they can receive is what the lease says they can get

- Stuck with a rent (for the term of the lease) unless they breach the lease

- During the term of lease, have a reversionary interest

Bundle of rights

- right of occupation, exclusion

By created a lease, you have essentially divested some of these rights away to another entity

- Profit

The Lessee:

- If the property is being rented by the lessee at a rate below the market rate, there is the potential for a profit to be made on the rent:

- For example:

| Full Market Rent | $1,000 per annum |

|---|---|

| Passing Rent | $800 per annum |

| Profit Rent | = $200 per annum |

- Subject to certain provisions of the lease, the lessee has the right to sub-lease the premises for the remaining term of the lease . In such cases, the lessee will become the Head-Lessee and this terminating “leasehold interest” (capitalisation of the profit rent) is the lessee’s interest.

The Valuation of Varying Incomes

There are several methods available for the valuation of varying incomes:

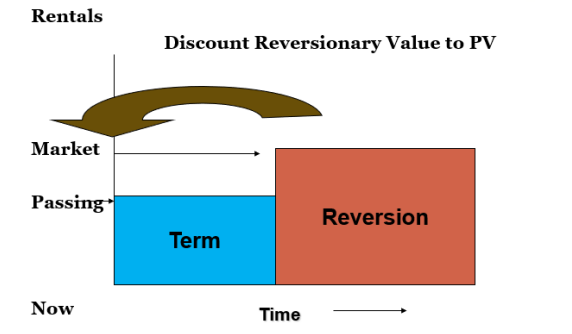

1 – Term and Reversion

- This method capitalises and then aggregates the term and reversionary Incomes. The reversionary value will need to be converted to a present value.

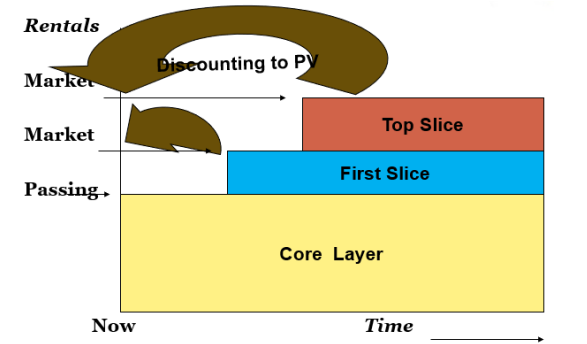

2 – Hard Core Method

- Under this method, income flows are dealt with as horizontal slices, with passing rent being the “core” income, and future increases due to reviews or reversions being additional slices.

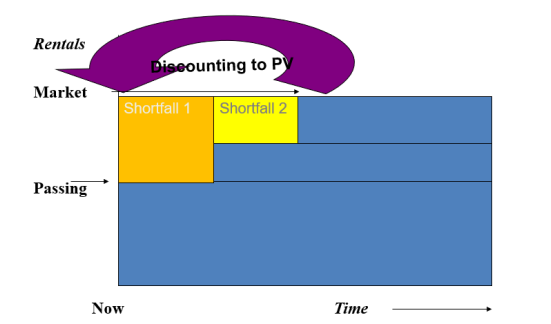

3 – Shortfall Method.

- This method calculates the “loss” of income before market rates are achieved and deducts the value so derived from full market value.

Term & Reversion

- Consider a relatively long lease term in a commercial class income producing property. The rental rates may well have been market based at the start of the lease, but over time have drifted to levels above or below market rates. This could easily happen where under the lease the rents are to be reviewed to a non-market based formula, ie to a set percentage rate or to CPI.

- This creates a problem when we need to value the freehold interest in the property. Remember, the freehold value of the property is based on the right to receive income from that property.

- As an example, consider an industrial building which is now leased for 3 years at $40,000 net pa (no outgoings). The market rent is still $50,000 pa and the Cap Rate for this property is still 8%.

- In order to establish the property value subject to the lease, we need to assess the value of the lease term and then the reversionary value, and then aggregate the two.

Often have long rentals, rent often goes up each year

- long term passing income may stray and is not the same as market rental income

| 1st step (Term Value) | Value |

|---|---|

| Passing Rental | $40,000pa |

| YP (period) for 3 years at 8% | = 2.5771 |

| Capital Value = $103,084 |

To calculate the YP (period) for 3 years at 8%, we simply applied the PV of $1 pp formula for an amount of $1, to establish the factor to be applied to the annual net rent; ie.,

Or, by calculator

- Pmt = $1

- n = 3

- i = 8

- PV = ? = 2.5771

2ND Step (Reversionary Value)

Market Rental $50,000 Cap Rate 8% CV = NI x YP = $50,000 x 100/8 = 50,000 x 12.5 = $625,000

Capitalise the reversionary interest

- know in three year time the property is worth 625,000

However, this is the value as at lease expiry, 3 years in the future. We now must discount that amount back to a Present Value.

By Calculator

- FV = 1

- n = 3

- i = 8

- PV = ? = 0.7938

Therefore $CV =

3rd Step Add Term and Reversionary Values to arrive at the property value.

- Capital Value = $103,084 (term) + $496,125 (reversion)

- = $599,209 (Adopt $600,000)

Hard Core, or Layer Method

- Income under this method is treated in horizontal slices. The passing income is the “core” income which is the most secure. Rental increases achieved after future rent reviews are then additional slices (ie 2 nd slice, 3 rd slice, top slice) added later and are considered to be less secure income sources.

- Each slice is valued in perpetuity, with later slices being discounted to a present value.

- This method is useful when the property being valued has multiple tenancies.

- 15 year structured lease at the following rental rates:

- 1st 5 years: $100,000 pa

- 2nd 5 years: $150,000 pa

- 3rd 5 years: $200,000 pa

- then reversion (at year 15) to Full Market Rental at $250,000 pa

- We should be able to value this income flow using the Hard Core method at a Cap Rate of 10%.

- We need to capitalise each layer in perpetuity, then bring each to a Present Value and aggregate to obtain the total value.

1st Step - Find the capital value of each layer

| Layer and formula | Cost |

|---|---|

| Layer 1 | |

| CV = NI x YP | = $100,000 x 10 |

| . | = $1,000,000 |

| Layer 2 | |

| CV = NI x YP | = $50,000 x 10 |

| . | = $500,000 |

| Layer 3 | |

| CV = Ni x YP | = $50,000 x 10 |

| . | = $500,000 |

| Layer 4 | |

| CV = NI x YP | = $50,000 X 10 |

| . | = $500,000 |

2ND Step - Bring each of the future values back to a present value using the PV of $1 formula, or by calculator:

- FV = amount shown

- n = period shown

- i = 10

- PV = ?

| Layer | FV | Period | PV |

|---|---|---|---|

| Layer 1 | 0 | $1,000,000 | |

| Layer 2 | $500,000 | 5 yrs | $310,460 |

| Layer 3 | $500,000 | 10yrs | $192,772 |

| Layer 4 | $500,000 | 15 yrs | $119,696 |

| TOTAL VALUE | $1,622,928 |

Shortfall method

- This Method essentially values the loss or profit above or below market to add or subtract from the market capitalisation

- Value a property subject to a 10 year structured lease at the following rental rates:

- 1st 5 years: $100,000 pa

- 2nd 5 years: $150,000 pa

- then reversion to Full Market Rental at $200,000 pa

- Cap Rate of 10%.

1st Step - Find the capital value of Shortfall 1 PV of $100,000 pa being received for 5 years

- PMT = $100,000

- n = 5

- i = 10

- PV = ? = $379,079

2nd Step - Find the capital value of Shortfall 2 PV of $50,000 pa being received for 5 years from Year 10

- PMT = $50 000

- n = 5

- i = 10

- PV = ? = $ 189 539 (FV 5 Years)

- FV = $ 189 539

- n = 5

- i = 10

- PV = ? = $ 117 688

3rd Step - Find the capital value of property assuming no lease

- $200000 / .1 = $ 2,000,000

- Subtract Rental Shortfall

- Shortfall 1 - $379,079

- Shortfall 2 - $117,688

- CV = $ 1,503,233

REAL ESTATE DEVELOPMENT

- “Property development is a process that involves changing or intensifying the use of land to produce buildings for occupation”

- “It is not the buying and selling of land for a profit: land is only one of the raw materials used.”

property development may also be demolishing a building,

- applying capital, applying smarts to it

Nature of Development Process

| Creative | Rational |

|---|---|

| Often intuitive | Often pain-staking |

| Especially up-front | Multiple constraints to be satisfied |

| Assimilate multiple inputs | Optimisation by options and feasibility studies |

| Importance of networks |

forced to work within a framework which doesn't necessarily help you make money

Development as a process

- Driven by “organic” growth

- Regulated by government (use, size, appearance, facilities, neighbourliness)

- Commercial/ political implications

- Market cycles

- High end of risk/ reward spectrum

Government funnels development

- put rules in place, town planning

- government tax you out of doing things in a particular way through regulations market cycles drive the behaviour of development

Development as a Progression

Why does this matter?

- At what point along this is there a project

- How certain is it?

- What risks are there?

Development Options

- Site selection

- Scale of improvements

- Single or mixed use

- Design options

- Market positioning

- Timing

- Staging

- Finance options

- Structuring options

- Resourcing options

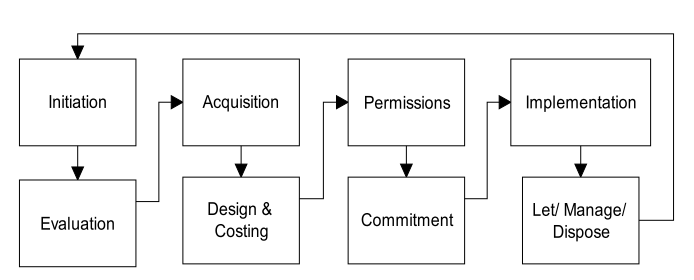

Project Initiation

Can be...

- Demand driven

- Supply driven

- Driven by regulatory change

- Success when all these intersect

Sources of Initiation

- Freelance initiation

- Organic Site Availability

- Site Amalgamation

- Formal invitations

- Land disposal motive

- End user driven

- Government Surplus

Go out an find it, or government released bundles of land

Market Cycles

- sectors perform at other paces to each other

- Different points in the property cycle for every property sector

The Building Cycle

Natural stock cycle

- Fuelled by uncertainty and long lead times Uncertainty in:

- Underlying demand

- Building activity

- Prospective yields

- creating a product you can't sell tomorrow

- appetites, products may have changed. Interest rates may change

- No one foresaw the price changes in materials in 2020 due to COVID

Cycle - Upturn

- New demand emerges

- Rental prices increase

- Increasing yields attract investors

- Sale prices and activities to rise

- Attracts yield-seeking investment

- Start of the cycle, upturn

- new demand, immigration increased, new change in lifestyle, etc.

- static supply increase in demand, prices go up

- activities rise

Cycle - Boom

- Entry of growth capital

- Volatile investment flows

- Rising prices attract new investors, further raising prices

- Developers enter as margins improve

- Over-heated - activity overshoots

- Overvalued prices lower yields

- Developers satisfy demand

- Boom sees activities, lower yields start coming back in

Cycle - Bust

- Oversupply & low rental yields

- Yield-seeking investors withdraw

- Sales, prices & activity fall

- Average prices distorted by forced sales

- Prices flatten (fall in real terms)

- Activity very low as prices below vendor’s expectations

- People getting out of investment

Cycle - Stagnation

- Activities stabilise at lower levels

- Excess stocks absorbed over time

- Lasts until demand gets ahead of stock levels

No excess demand, no excess supply

Dwellings

- 5-8 years

- Activity upturns of 50-80%

Offices

- up to 15 years

- Activity by 400% during upturn

- Boom can last 6 years

- Price rises of 30-80%

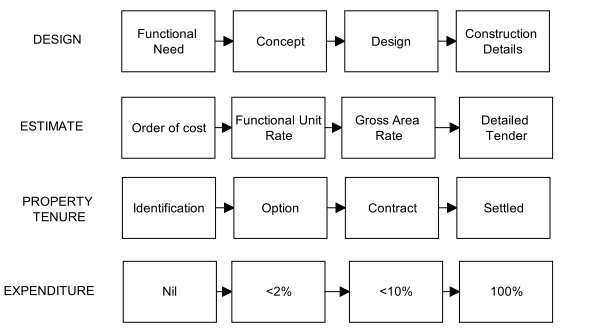

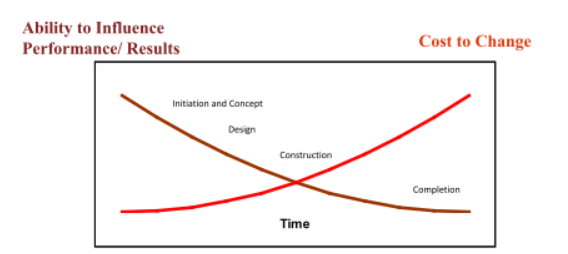

Stages of the Building Design Process

- Concept design

- Schematic design

- Developed design

- Construction documentation

Assignment, wont need to go into schematic or design documentation

Costing at Each Stage of Design

- Concept: $/m2 based on functional use

- Schematic: $/m2 based on type of construction

- Developed Design: Elemental cost estimate

- Construction Documents: Detailed BOQ and trade estimate

Rate/m2 of the type of construction you want QS data derived from historical costs (eg Rider’s Digest, Rawlinsons’)

Consultant Disciplines - Services

- Mechanical

- Electrical

- Communications

- Hydraulics

- Fire- electrical

- Fire - water

- Vertical transportation

- Specialist lighting

- Audio-visual

- Special equipment (kitchens, laundries etc)

Number of consultant you might need is staggering

- Using a valuer can assimilate at a really high level

Consultants - Non Design

- Planning & approvals

- Code compliance

- Survey

- Cost planner/ QS

- Programmer

- Valuer

- Marketing -- important to get right early on

- Taxation

- Legal

- Public/ government/ media relations

- Body corporate

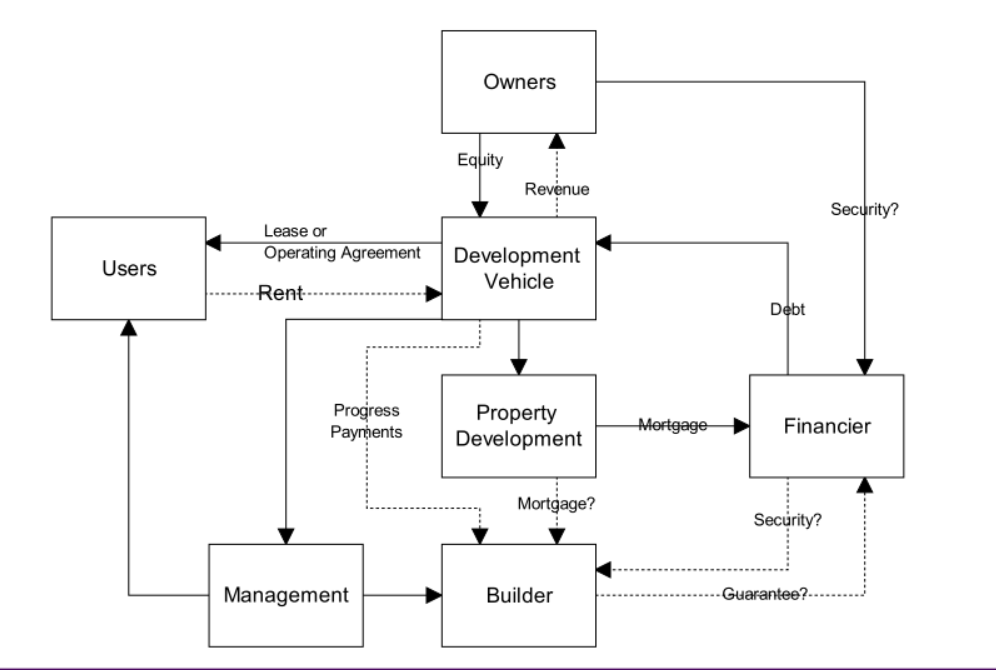

Hypothetical Development Model

Hypothetical Development Equation

- “Value of Finished Product” = land value + dev costs + finance costs + profit

- Value of Land = Value of Finished Product that is Gross Realisation – (dev costs + finance costs + profit)

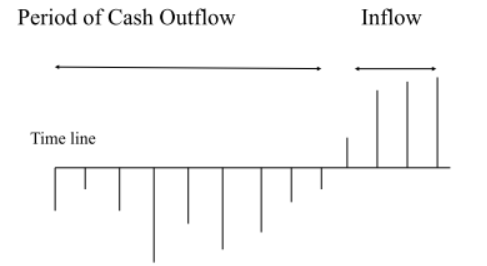

How you much pay for a land that has a simple development opportunity Done in a single period, no TVOM

no income and costs happening at the same time

- If multistage development, have to use a DCF

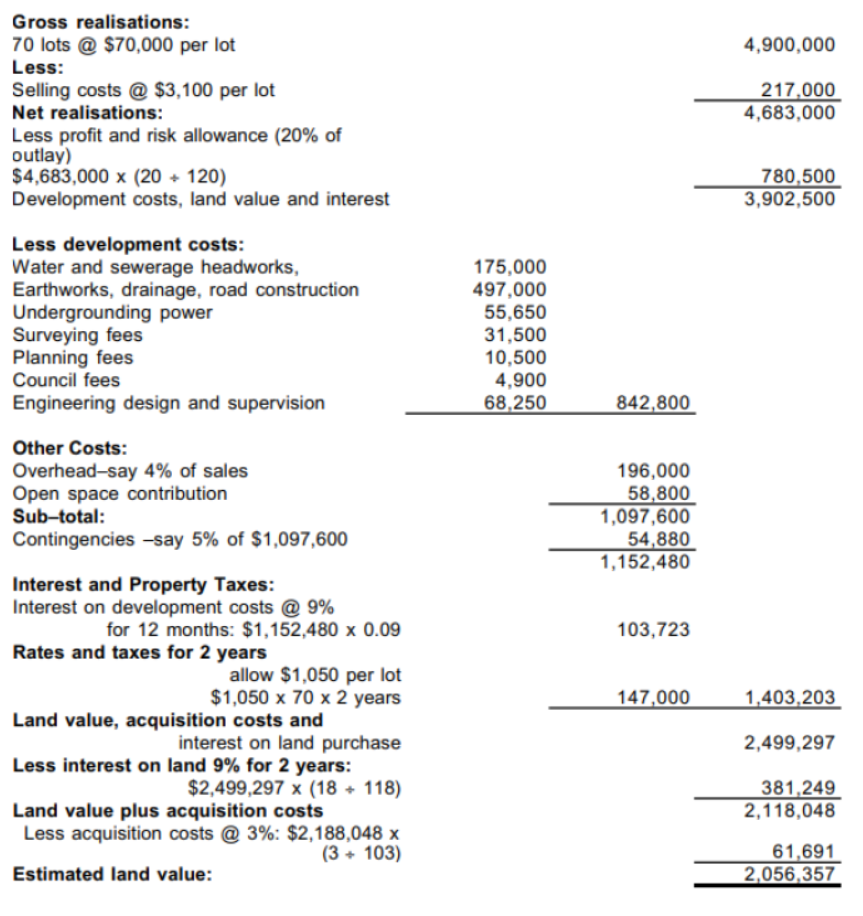

Hypothetical Development Method Example

- Gross Realisation

- Less Selling and Legal Costs

- Net Realisation

- Less Profit and Risk/Development Margin

- Less Development Costs

- Less Interest on Development

- Less Interest on Land

- Less Acquisition Costs

- LAND VALUE

Gross Realisation

- how much money I get in my pocket after I sell everything

- Standards agents' commission 2.5% development agents can be as high as 15%

- Banks want to see pre-sales covering their total debt Net Realisation

- Less selling costs and

- Called profit and risk rate because it changes depending on how risky it is

- Builders would not take on a riskier project with taking a larger margin

- larger component of risk

- 6-8% risk margin

- Want to buy a house and add value

- this is the best model, to determine the cost of all the inputs

Hypothetical Development Method

a) Step 1 - Assess Gross Realisations

- Direct comparison approach

- Local market value

- Allowances

- Internal Area

- Location

- Views

- Quality of Fit out

- Onsite Amenities

- Car Accommodation

- Number of units in development

- Aspect

Challenges of gross realisations of gross market comparisons

- product is not available - have to build, get approvals etc.

- Have to get a feel for the market in next 1.5-2 years

b) Step 2 - Assess Cost Estimates

- Ideally provided by Quantity Surveyor/Engineer including:

- Construction costs

- Council contributions

- Professional fees

- Contingency

- Rates and land tax

- Finance cost (application & interest)

- Stamp duty purchase and sale

- Agent’s commission

- GST (Margin Scheme?)

- Can breakdown to costs per toilet, window, etc.

- m2 of plaster, concrete, etc.

- can be as precise and unprecise as you would like

c) Step 3 – Estimate Sale Rate

- Presales

- Derived from other developments

- Establish demand for product in that area - will be partly determined by price

- Sales rates are often wrong

- What often happens is that you might miss business cycle and not able to sell properties

- Is there a capacity to take up more property in this market?

- are there more widgets added to this market?

- price/premium, cut the price to sell fast

d) Step 4 – Estimate Holding Costs - Interest

meant to be an opportunity cost, under assumption that you could invest elsewhere

- Makes more sense to apply interest over the total borrowings

e) Step 5 - Select Development Margin

- Factors

- Location

- Risk

- Development Approvals

- Presales

- Derived from Analysis of Sales

One of the hardest things to derive based on sales evidence

- most used an industry standard value range

- risk is y/z%

- As a developer, not constrained to select margin

Risk profiling your project

The major risks in relation to any project generally relate to the following areas:

- a)Planning

- b)Construction

- c)Sales/leasing

- d)Financial

Planning

- a)Delays

- b)Not achieving expected outcome

- c)Increased costs of imposed by planning outcomes

Construction

- a)Higher than expected costs, including escalation prior to commencement and during construction

- b)Failure of your chosen contractor during construction

- c)Demolition uncovering unforseen environmental issues

Risk profiling

Sales / leasing / marketing

- a)Rate of sale/leasing during and post construction

- b)Settlement failure of presales / pre-letting (“fallover” risk)

- c)Payment of commissions (prior to completion financial planners)

- d)Market incentives e.g. rental guarantees

- e)Marketing budgets Financial

- a)Increased cost of funds

How much detail do I need?

- Most common method of used to appraise development schemes.

- Can be as simplistic or as complex as the valuer chooses.

- Important that a valuers skill and experience is used to estimate or assume the differing variables.

- Hypothetical Development methods can be utilised to assess any type of development property.

One-pager is sufficient

Profit and Risk

- Profit and Risk factor determination - That is the profit required in relation to the risk of capital.

- Various factors are considered by purchasers and include:

- Complexity of the development, strength of the market, profit margins, interest rates, competition, size of development…

- Higher the risk / Higher the profit.

- Rates for profit and risk are best derived from market evidence in the form of actual profits made by subdividers in the market place.

- Analysis of englobo sales of comparable properties is the most reliable source of evidence.

Hypothetical Valuation

What You Need To Know

| What is the end product? | Type of Product / Size / Quality |

|---|---|

| How Many? | No of units/blocks of land etc |

| How Much? | Sales Price |

| How Fast? | Approval, Development, Sales Rates |

| How Much? | Profit/risk rate |

| What? | Interest Rate Applicable |

With all these question answered, and calculate the price of the land

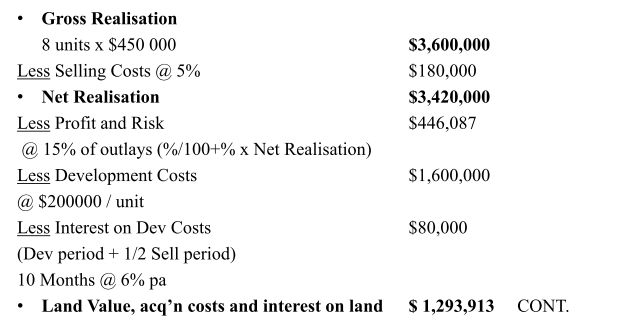

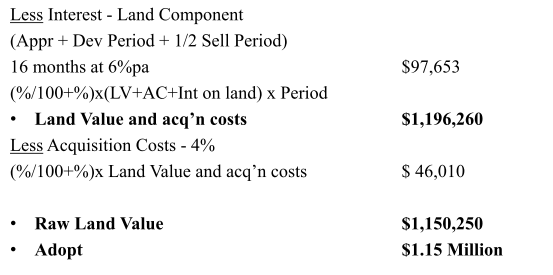

Hypothetical valuation

| What? | Medium Density Residential Units |

|---|---|

| How Many? | 8 Units |

| How Much? | $450,000/unit |

| & | $200,000/lot production |

| How Fast? | Sales rate = 2 units/month |

| & | approval period = 6 months |

| & | development period = 8 months |

| & | selling period = 4 months |

| How much profit/risk? | 15% |

| Interest Rate Applicable? | 6% |

i/(1+i) * period

hypothetical Development Methodology

Advantages

- Reflects intricacies of the site

- Reflects services and costs

- Reflection of a purchaser’s decision process Disadvantages

- Sensitive to changes in gross realisations/cost estimates, sale rates

- Difficult to establish market driven development margins

- Making future predictions which are subject to external influences

need to check that we can afford the asking price of the land

- realistic tool to determine land value

Disadvantages

- hard to define through market analysis what the costs might be

- Valuations don't do valuation in the future; contingent on market factors which exist yet