Lecture 8 - Debt and taxes

DEBT & EQUITY CAPITAL

Four Categories

- Capital Markets can be divided into four categories based on whether they are public or private markets and if the assets are traded with debt or equity.

- Public Markets - small units (“shares”) of ownership in assets are traded in public exchanges. i.e. stock market

- Public markets have a high degree of liquidity – generally possible to quickly sell units of the assets at or near the last quoted price.

- Public markets have high informational efficiency

Risks, time costs, availability

- Public equity or private equity?

Public markets

- Generally a high degree of liquidity in public markets

- High informational efficiency - equally to buyers and sellers

Private Markets

- assets are traded privately between individual buyers and sellers

- Generally less liquid than public markets

- Common for whole assets (entire company, property etc.) to be purchased

- Private markets are less informationally efficient than Public markets

Debt assets

- Debt Assets – rights to future cash flows to be paid out by borrowers on loans

- E.g. interest payments and retirement of principal on a loan

- Debt assets may provide owners with a relatively senior claim to obtaining cash than the underlying asset

- Debt cash flows provide relative security over how much and when payments will be made

Private markets

- difficult to sectionally sell components of an asset

- Generally buy the whole company

Debt asset

- bank that has lent money to somebody, asset to the bank

- Bank and someone has put money into the account, it is a liability for the bank

- Can either be unsecured or secured

- Person who owns the debt asset may receive/access an asset if the debt obligations are not met

Equity Assets

- give owners the “residual” claim in the cash flows generated by underlying asset

- Lacks seniority to debt owed on the asset/property

- Tends to be more risky than debt

- Equity owners tend to have more control over managing underlying assets & are better able to benefit from growth

- Owners need to sell the asset in order to liquidate their holding – means more volatile market

| . | Public Markets | Private Markets |

|---|---|---|

| Debt assets | Bonds, MBS (mortgage backed securities), Money instruments | Bank loans, Whole mortgages, Venture debt and LBOs |

| Equity Assets | Stocks, REITS, Mutual Funds | Real Property, Private Equity, Hedge Funds |

DEBT & EQUITY FINANCING FOR REAL ESTATE

Overview of Debt – Senior Debt

- Bank Debt

- Most liquid and flexible option, albeit bank focused on investment grade

- Can be structured as bilateral, clubs or syndicates

- The loan you get from the bank

- large loans you are probably not getting from one bank

- banks will syndicate to create the loan

Other types of senior debt

- Bonds - securitised by the government

- company, the company pays back the debt obligations

- Japanese bonds issued with negative interest rates

- Alternative Capital

- Wholesale notes: New product funded mostly by high net worth individuals

- Private placements: Funds are emerging as a new class of lender, albeit at higher cost than banks

Convertible note:

- if you default, convert debt into equity

Gearing

Development Property

- Bank funding capped 70-80% of the development cost

- Pre-sales required to cover 100% of the bank debt

Commercial Property

- LVR up to 60-65% for senior and 70-80% sub/mezzanine debt

- REITS aim for gearing of <40% to maintain investment grade rating

Banks will not lend you the full amount

- E.g. $20M to build, you will only be able to borrow 15-16M

- sell for $300k

- want to see you ahve sold 60% of the units, contracts must be enforceable and locked in to cover the costs of the debt

If you only have only 20% equity, need other forms of debt

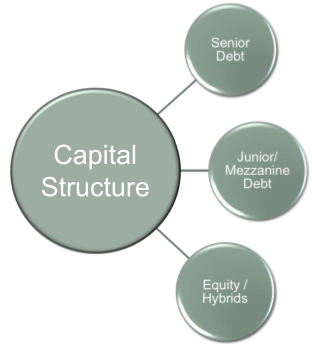

Capital Structure – Junior / Mezzanine Debt

- Globally, a growing market with a commercial prevalence of credit funds emerging with 30 – 40 of them now operating in Australia

- More expensive than senior debt due to lower guarantor / security ranking

- Primarily used to increase debt levels above senior debt capacity

- Lenders to this class of debt include:

- Super funds

- High-yield funds

- Uni-tranche funds

- Special situation funds

- Distressed funds

Mezzanine debt is a layer of debt that sits above the debt but beneath equity

- bridges the gap between equity and debt

- generally have to pay a lot more for it

- used for where something in the development project could be sold quickly and is ready within a short period of time

Capital Structure – Equity

- Space Market Investment

- Most expensive source of funding due to ranking behind all debt, with upside returns

- Can be in the form of:

- Equity shareholding (public and private)

- Some forms of hybrids/convertibles with mandatory conversion

- Institutional providers other than superfunds/fund managers can

include:

- Venture capital

- Hedge funds

- Private Equity

- Family Offices

No guarantee of getting returns

DEVELOPMENT FINANCE

Characteristics

Debt

- a loan

- contractual obligation to repay

- usually secured

- for a defined term

- interest payable

Equity

- an investment

- no surety of repayment

- unsecured

- in perpetuity

- dividends payable only from profits

Equity

- when you own equity, owned forever until you liquidate it

- right for an income stream of a loan is finite

2. Debt Finance Facilities

A. Term loans B. Bank bills C. Letters of credit (LCs)

- letter of credit

- May go into a transaction where you show that you have capital but don't want to use it

- 'Knowing there is money in the bank for you'

2A. Term Loans

- Most common type of debt

- Flexibility to match interest/ principal repayments to available cashflow

- “Construction Finance” (Short term = to around 2 -4 years)

- “Term Debt” (longer term = more than 4 years)

Setup bank to manage your cashflow to not pay to the bank until time period

- not usual to have capitalisation of interest

Construction Finance

- start the project and the builder goes broke and the construction company goes broke, you will be in trouble

- in GFC - lots of developers went broke because a lot of the financiers did not have interest/demand to sell properties and fulfil construction finance loan

- Can destroy you if you get you funding wrong

- Do a development and it starts to file, convert the construction finance into term debt

2B. Bank Bills (Bills of Exchange)

- Negotiable instruments

- Commitment to repay at fixed future date (up to 180 days)

- Can roll over (at prices then current)

- Characteristics of a post-dated cheque

- Often used where there is a guaranteed takeout

Structured a transaction to have an 80% loan e.g.

- sale of other property will give you 20% capital

- bank bill will cover 20% equity for the short period

- Bad position if you don't sell the property

2C. Letter of Credit

- Guarantee by a financier used to underwrite borrowing of client to a third party

- Allow client flexibility to shop for best interest rates

- Not favoured by banks (low margin differentials)

3. Costs of Debt finance

- A. Interest

- Interest rate = Lenders Cost of Finance + Risk Margin

- B. Establishment Fee

- C. Line Fee

- D. Reimbursables

If you are a riskier borrower and don't have a history of income, a standard bank may not give you a standard rate

- another bank with a bigger risk profile may allow it

Establishment fee

- Massive fee potentially

- Sometimes banks charge a non-refundable component of the establishment fee

Line fee

- opening up a line of credit, a fee is charged

- creating a $100M development, and spend money in credit over a period of 2 years, e.g.

- banks will secure $100M to draw down

- banks will charge to secure the line of credit, and will

Reimbursables

- lawyers, town planning reports, banks will have experts and will want them paid for

3A. Repayment Structure

- Amortisation = repayment of debt gradually over the term (incl both interest and principal) - can be uniform or structured

- Interest Only = regular interest payments, principle at settlement (most common)

- Capitalised interest = all repaid at end

Could be structured with unequal payments, might change based upon investment horizon

Interest only

- benefit of capital growth, payoff the principle at the end of the payment

- Popular form of debt financing until APRA changed the use of interest only loans

3A. Interest Options

Fixed

- Certainty about repayments

- More expensive than floating

- Up to 5 years available

- Break costs apply with early settlement

know exactly what your interest will be

- Does not happen in Australia (only for 5 years)

- In America the fixed interest rates stay for the duration of the loan

- If you borrow money from a bank and it's fixed, will see rates in the future to guess future bank rates

- Borrow money on fixed interest and rates decrease, if you want to refinance banks will charge a break cost

Floating

- Take advantage of falling rates

- Borrower exposed to interest volatility

- Referenced to a published market rate (eg bank bills)

- No real break costs

3B. Other Costs: Establishment Fee

- Covers lender’s cost of processing application and documentation of loan

- Typically 0.5%

- Payable upfront

- Payable only if application approved

3C.Other Costs: Line Fees

- Covers lender’s costs of ongoing loan administration

- Typically 1.0% pa

- Payable each year (or part year)

Covers costs of administration

4. Debt - Security

Debt can be:

- recourse (ie with security)

- non-recourse (ie with no security)

- or limited recourse Trend away from asset backed toward a cashflow and capacity to repay approach

Historically is the gearing low enough that you will get money back?

- what cash flows are associated with the development

- What other income streams do they have? Do they have the capacity to pay?

- not a simple as LVR anymore

5. Types of Security

- Mortgage over property

- Security over other physical assets

- Charges over associated companies

- Rights to future cash flows

- Guarantees

6. Security Terms

- A. Registered mortgages

- B. Charges - fixed and floating

- C. Cash on deposit, bank guarantees or letters of credit

- D. Personal and directors’ guarantees

- E. Third party guarantees

- F. Cross-collaterisation

Companies over personal property and property shares

- Bank guarantee - if you are doing a development project to pay developer, secure a bank guarantee to the builder to satisfy that you can repay debt obligations

- Might create bank guarantees on the back of previous relations

Personal and Directors Guarantees

- SPV for development, start an LLC with paid up capital of $2

- When the company goes broke, gets paid up capital

- As Shareholder, structure the capital so that only company equity is required to pay debts

- Create a personal guarantee with the Director to finance debt obligations if default

- Could be guarantee from parents

Cross-collaterisation

- Debt for the bank to yur home

- have a business also, requires debt for generating business

- Most banks will have a provision to cross-collaterise your debt, don't go to the same bank for business loans and personal home loans

6A. Registered Mortgages

- Real Property Act provides for a registered charge on land securing payment of a debt

- Banks usually insist on 1st mortgage

- 2nd mortgage risk dependent on 1st mortgagee’s conduct

6.C Cash, Bank Guarantees, LCs

- Still better to borrow than use direct cash (tax benefits)

- Banks generally lend to 100% of value

- Possible to fund development as 100% debt by effectively using these

7. Typical Development Debt

- Max loan to cost ratio ~ 70-75% of “hard” costs

- Secured by mortgage (plus guarantees?)

- Interest ~ 30 points (3%) above bank bills currently around ?%

- Interest payable progressively

- First draw-down after Building Approval

8. “Hard” vs “Soft” Costs

Hard Costs

- Construction

- Land plus all costs to BA Soft Costs exclude:

- Agent commissions, advertising/ marketing, stamp duty, bank fees

9. Refinance on Completion

Construction Finance

- construction & take-out risks

- higher interest

- capitalised interest

- high levels of security

Term Debt

- only operating risks

- lower interest

- regular interest

- less harsh security

10. Basic Finance Terms

- Loan to value ratio (LVR)

- Loan security ratio (LSR)

multiple assets for security

- Peak debt and exposure

- Amortisation

- Interest: fixed/ floating, caps/ collars, swaps

Debt Security Measures

- Loan to Value Ration (LVR) = amount borrowed / value of the property

- Loan Security Ratio (LSR) = amount borrowed / value of all securities

Bank guidelines on LVR

- Residential housing to 90%

- Income producing property to 67%

- Also look at % of “hard costs” to 75%

- Specialised properties (eg hotels) to 50%

Very expensive and rarely accessed

- Income producing property,

ASSIGNMENT: Construction loan and term loan?

- need to consider the loan structure

Loan Agreement Issues

- Principal amount

- Term - repayment schedule

- Interest rate; fixed/floating, amount

- Timing of interest

- Security; form, recourse and priority

- Performance covenants

- Default (eg increase interest 2-3%)

how are they compounding the interest

Performance covenant:

- need to have the house insured

- Will not build anything on the land that is illegal

Financial Metrics

Equity Multiple

- Very basic metric

- Doesn’t take into consideration discounting or time value of money

- Its simplicity makes it popular

The equity multiple is arrived at as follows:

- EM = Er/Ei where:

- Ei = equity invested

- Er = total cash returned (income and capital)

- EM = equity multiple

Example

- The Equity Multiple measure is at its most appealing when dealing with a very simple investment focused on capital gain.

- Assume you paid a $100,000 deposit for a house in cash that cost you $1,000,000 including all acquisition costs with an interest only loan of $900,000.

- You received no net income whilst you own the unit (ie rent covered all costs including debt payments which are interest only)

- Five years later you sold the unit for $1,650,000 and received $1,607,100 after costs of sale were paid.

- Total return $1,607,100 (income) - $900,000 (outstanding liabilities) = $707,100

- This would show an Equity Multiple of 7.07

- EM = Er/Ei

- EM = $707,100/$100,000

- EM = 7.07

Income return

Income Return

- This is the net rent or NOI received over the measurement period

divided by the value at the beginning of the period.

May have different LVR's for different projects Readings will have a good example

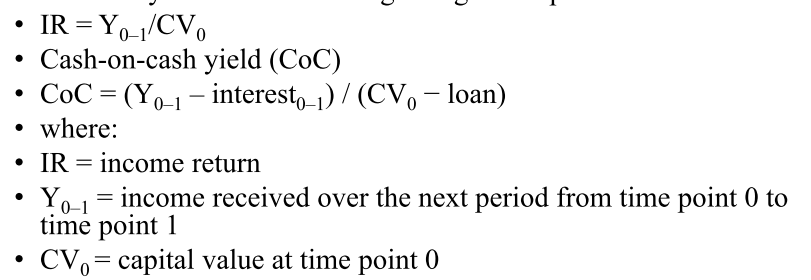

Cash On Cash Yield

- The Cash-on-Cash Yield is the Income Return that an investor receives when they use debt.

- It represents the ratio of cash flow generated by the property to the amount of cash invested.

- It is useful to differentiate between real estate assets to determine which one has the highest return for any given amount of cash (ie equity) invested.

yield for your equity

Example

- Assume that an apartment block was bought for $40,000,000.

- The investor put in $8,000,000 of equity and a major bank made a senior loan of $32,000,000 on an interest only basis.

- The passing net rent is $3,000,000 p.a.

- The interest rate on the senior debt is 7%, meaning that $2,240,000 p.a. of the rent is needed to pay interest. The investor keeps the rest of the rent.

- What is the LTV ratio?

- What is the Initial Yield?

- What is the Cash on Cash Yield?

- TVR = 80%

- initial yield = passing rent/capital value = 3/40

- cash on cash yield = (760) / 8000 = 9.5%

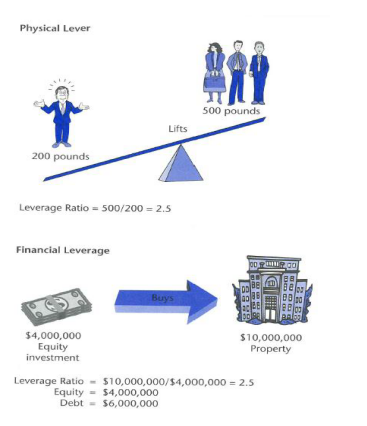

Mechanics of Leverage

- Analogy between financial and physical leverage proves helpful.

- $4m in equity can purchase $10m in property.

- Leverage Ratio = value of underlying asset divided by the value of the equity investment.

Need to understand what your leverage ratio is

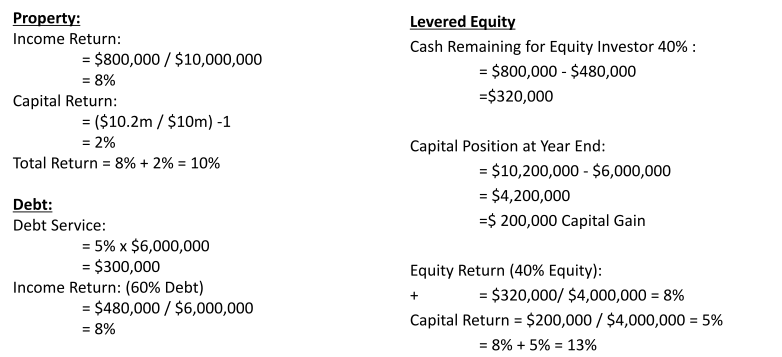

Effects of Leverage on the Expected Return

- Substantial leverage has the effect of substantially increasing the expected return.

- If an equity investor is able to borrow money at an interest rate lower than the expected return.

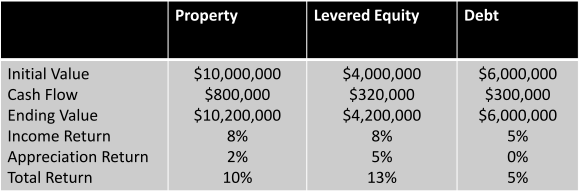

- Example:

- Purchase Price: $10,000,000

- Value Appreciates to: $10,200,000 (2%)

- Income Return: $800,000

- Interest Only Mortgage: 5%

- Loan: $6,000,000

- Equity Invested: $4,000,000

Effects of Leverage on the Expected Return

LEVERAGE

Tax

- Tax complicates things..

Negative gearing

- income less than total costs, claim tax deduction

Tax for two things

- capital gain

- Didn't always used to be taxed. In 1985 changed to be part of marginal tax rate

- Home ownership is more than 12 months, capital gains tax is halved

- income

after tax

- less incomes tax, capital gains tax

- AND GST

- If you borrow money from property, you can deduct interest from income

Why Tax Matters?

- Not all properties are taxed in the same way

- Rental income or capital gain

- Depreciation allowances

- Recapture on resale

- Not all owners are taxed in the same way

- Different rates

- Different offsets

- Different treatment of losses from properties

- Different ownership entities

- Passing through or paying tax

- have non-cash deductions in property

- depreciate fixtures over different rates

- capital improvements are not a capital deduction up front

How is Tax Payable Calculated?

Assessable income

-

- less deductions

- = Taxable income

- x marginal tax rate

- = Basic tax payable

-

- less tax offsets

- = Tax payable

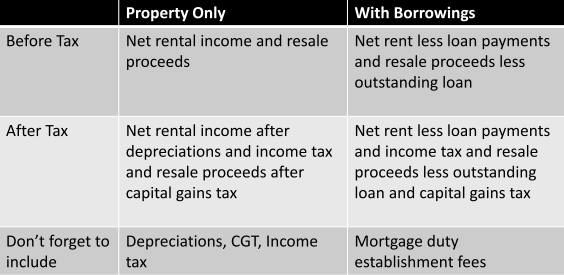

Either calculated

- By treating the property as a separate investment, or

- The difference between tax paid with and without the property

Interest is a deduction, but paying principle on your loan is not a deduction, e.g.

Rental Income

- All Rent and other recurrent lease payments

- On either cash/receipts basis or accruals basis

- Accruals may be applicable for rent paid in arrears

- And trading profits of developers and other businesses

Capital Gain

- Capital gains tax (CGT) is the tax you pay on a capital gain.

- It is not a separate tax, just part of your income tax.

- The most common way you make a capital gain (or capital loss) is by selling assets such as real estate, shares or managed fund investments.

Deductions

- Expenses incurred in producing assessable income provided they are not

capital, private or domestic

- They can be claimed when they are incurred (due to be paid) or prepaid for the following year or they must be “properly referable” to the year of claim

- The latter for businesses

- Statutory charges, insurance, fuel, management charges, etc as well as:

- Loan interest

- Repairs/maintenance

- Depreciation allowances

Deductions: Loan Interest

- Deductible provided that the money is borrowed to produce assessable income..

- In the not too distant future…

- Negative gearing generally means:

- That the loan interest exceeds net income; or that rental property deductions exceed assessable rental income

- The tax loss shelters investor’s other income from tax

- Borrowing expenses are deductible over the shorter of the loan period or five years.

Deductions: Repairs / Maintenance

- Not renewal or improvements (generally depreciable)

- Not initial repairs to enable the property to be rented

- Not payments into sinking funds until spent

- Not capital expenditure

Deductions : Depreciation and Capital Expenditure (Capex)

- Capex:

- The renewal of material different from the original: and / or

- Work that has effectively been an improvements; and / or

- Has increased the value of the asset; and / or

- Expenditures to reduce the likelihood of further repair