Risk and Uncertainty

- Risk is when you know what the outcomes could be, and can assign probabilities

- Uncertainty is when you can’t assign probabilities; or you can’t come up with a list of possible outcomes

Loss Aversion

- Losses loom greater than gains.

- Strong preference to avoid losses rather than acquiring equivalent gains.

Examples/manifestations

- Not selling a stock when your current rational analysis of the stock clearly indicates that it should be abandoned as an investment.

- Selling a stock that has gone slightly up in price just to realize a gain of any amount, when your analysis indicates that the stock should be held longer for a much larger profit [Disposition effect].

- Prevent a company from discontinuing a failing product line or from investing in a promising but uncertain venture.

Mitigate effect

- Setting predetermined selling points (stop-loss orders) to limit potential losses and remove emotional decision-making

- methods like dollar-cost averaging to mitigate the emotional impact of market fluctuations and loss aversion

- prepare clients for the inevitability of market downturns to help them avoid panic selling due to loss aversion

Risk Aversion

- A person who is risk averse prefers the expected value of a prospect to the prospect itself

- Preference for lower levels of risk and uncertainty.

- Risk-averse:

Examples/manifestations

- prefer investments with lower but more certain returns, such as bonds or index funds.

- Lead a company to retain excess cash reserves or avoid taking on debt, even when those resources could be invested profitably.

Risk Seeking

- Risk seeking describes someone who prefers a lottery to the expected value of a lottery.

Examples/manifestations

- risk-seeking individual might invest more heavily in high-risk, high-reward assets, like individual stocks or cryptocurrencies.

Lottery and Insurance

- A lottery is a prospect with a low probability of a high payoff. Many people buy lottery tickets, even with negative expected values. These same people buy insurance to protect themselves from risk.

- Normally, insurance is a hedge against a low-probability large loss. These choices are inconsistent with traditional expected utility framework but can be explained by prospect theory.

Mental Accounting

- Individuals classify money differently based on subject criteria.

Related

- integration/segregation

Fear of Regret

- Make decisions based on minimising the possibility of experiencing regret in the future, even if it means avoiding potential opportunities or taking risks.

May be a conservative investor; invest in other stock/security for fear of missing out despite obvious risks

- Similar to FOMO

Integration/segregation

- Integration - This suggests that people keep track of their gains and losses over time and use this cumulative total as their reference point

- Segregation - This refers to the idea that each new gamble is evaluated in isolation

Related

- segregation and integration, used hand-in-hand with prospect theory

Silver lining effect

- They tend to mentally combine wins but separate losses to make them feel less impactful.

House money effect

-

People tend to be more willing to gamble with money that they have won (house money) than with their initial stake or with money won in earlier rounds of betting.

-

segregation vs integration

Overconfidence

Overconfidence: unwarranted faith in one’s intuitive reasoning, judgments, and cognitive abilities.

Strains of overconfidence

Miscalibration

- tendency for people to overestimate the precision of their knowledge

Measuring Miscalibration

- Calibration tests

- how many you though you answered correctly

- Confidence interval approach

- Confidence interval: an interval that is expected to contain the parameter being estimated

Better-than-average effect Refers to the tendency for a person to rate themselves as above average.

- Many of us feel we are smarter or more skilled than average, but only 50% of us can really be better than average.

Illusion of control The tendency to think that there is more control over events than can objectively be true

- For example, gamblers may think that they can control the outcome of the dice or the cards, or people actually believe that the risk of infection is partly a function of the character of the person that they are coming into contact with.

Excessive optimism

- Reflects the feeling that things will be rosier than objective analysis suggests.

- When people’s predictions about the future are unrealistically optimistic.

- Students expect to receive higher marks than they actually receive.

- Overestimates the number of job offers that they will receive.

- People think they can accomplish more than they actually end up accomplishing.

- RELATED - miscalibration

Impacts/Implications

- Unfounded belief in own ability to identify companies as potential investments: blind to any negative information

- Excessive trading: lower returns

- Underestimating their downside risks: surprise on underperformance

- Portfolio under-diversification: taking on more risk

- overconfidence is the driving force behind both excessive trading and under-diversification

Mitigate effect

- Review trading records of past two years and then calculate the performance of your trades.

- (1) review investment holdings for potential poor performance; (2) realized how volatile the markets are

- Checks and balances: Implementing a more robust decision-making process that includes input from all team members

- This might involve regular performance reviews, risk assessments, and peer evaluations to provide balanced perspectives.

- Fostering an open culture: Creating an environment where team members feel comfortable voicing concerns and suggestions without fear of retribution is crucial. Encouraging open dialogue

- Data-driven approaches: Utilizing quantitative models and data analytics

- Performance metrics and accountability

Factors impeding learnings from overconfidence

Self-attribution Bias

- A reason impeding overconfidence

- The tendency to attribute successes to one's own abilities, while blaming failures on circumstances beyond one's control (forget our defeats)

Hindsight Bias

- Says we knew what was going to happen when we really didn’t.

Related concepts

- related to bubbles

Confirmation Bias

- the tendency to search out evidence consistent with one’s prior beliefs and to ignore conflicting data.

Self-control bias

People to fail to act in pursuit of their long-term, overarching goals because of a lack of self-discipline.

Halo Effect

Someone who likes one outstanding attribute of an individual likes everything about the individual

Heuristic (and two types of heuristics)

- Heuristics or rules-of-thumb: decision-making shortcuts.

- Type 1: Autonomic and non-cognitive, conserving on effort.

- Type 2: Cognitive & requiring effort.

Diversification Heuristic

The diversification heuristic suggests that people like to try a little bit of everything when choices are not mutually exclusive.

Ambiguity Aversion

- People are more comfortable with risk vs. uncertainty (ambiguity).

- In experiments, people are more willing to bet the colour of a ball drawn at random if they know the bag contains 50 red and 50 blue, than if they know a bag contains blue and red balls in unknown proportions.

Manifestations

- under-diversification

Endowment Effect

- What you currently have seems better than what you do not have.

- Experimental subjects valued something that they possessed (after it was given to them) more than they would have if they had to consciously go out and buy the item.

Information Overload

- better way to close a deal is to offer a small selection

- A Large selection might attract more interest but a small selection will close a deal

Representativeness

-

People frequently make the mistake of believing that two similar things or events are more closely correlated than they actually are.

-

Representativeness exists when one thinks that A should look like B. A can be the sample and B the distribution, or vice-versa.

-

Judging the likelihood of things in terms of how well they seem to represent, or match, particular prototypes.

-

Investors are prone to believe that a history of a remarkable performance of a given firm is “representative” of a general performance that the firm will continue to generate into the future.

-

People are too influenced by latest information.

Examples

- “Good companies are good stocks” thinking may lead to value advantage

Recency Effect (related to representativeness)

- Recent evidence is more compelling

Examples/manifestations

- May explain chasing winners

Salience Effect (related to representativeness)

- Dramatic evidence is more compelling.

Availability (related to representativeness)

- Freely available, easily processed information is more compelling.

Primacy Effect

Primacy effect is the tendency to reply on information that comes first when making an assessment

Conjunction Fallacy

An example of people having difficulty with probabilities is when they have no notion of the difference between simple probabilities (probability of A) and joint probabilities (probability of both A and B)

Base Rate Neglect and Bayes’ Rule

- The tendency to ignore relevant statistical information in favour of case-specific information.

Hot hand phenomenon

- Tendency to believe that a successful streak is likely to lead to further success

Related

- Illusion of Control

Gambler's Fallacy

- The gambler's fallacy is the tendency to overweight the probability of an event because it has not recently occurred

Anchoring

- Anchoring says new information is discounted. Anchored to original beliefs

Anchoring vs representativeness

- It is argued that people are “coarsely calibrated.”

- flip-flop coarsely between anchored and representative biases

Examples/manifestations

- May explain momentum and price reversal

- Positive qualities should already be embedded in price.

- Loosely speaking, good companies will already sell at high prices, and bad companies will already sell at low prices

Familiarity/Home bias

- People tend to favour local firms

Cognitive dissonance

Display cognitive dissonance when one simultaneously holds two thoughts which are psychologically inconsistent.

Home Bias

- Excessive optimism about the prospects of the domestic market.

- Comfort-seeking and familiarity.

- Institutional restrictions

Momentum-Chaser

- Trend followers with the view that investment performance in the recent past represents future performance.

Contrarian

- Purposefully goes against the prevailing market trends.

- buys stocks that have not performed well in the past

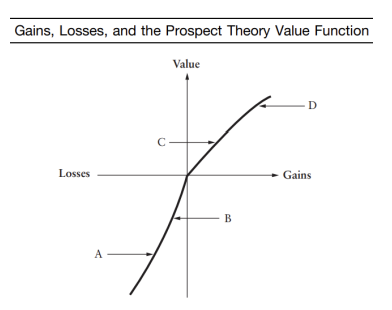

Disposition Effect

Tendency to sell winners too early and hold on to losers too long.

Explained through Prospect theory and Mental Accounting

- After a large gain (D), you have moved to the risk-averse segment of the value function. Only major reversals of fortune are likely to move you back to the origin.

- On the other hand, after a large loss (A) you have moved to the risk-seeking segment of the value function and, again, you are unlikely to move quickly back to your reference point.

- The implication is that since you are less risk-averse for losers than winners, you are more likely to hold on to them.

Explained through experimental evidence

- Experimental design was predicated on whether or not individuals have chosen

their investments.

- When no choice, you will experience disappointment

- When with choice, you will experience regret (which is stronger than disappointment)

Related concepts

- Link to prospect theory and mental accounting

Snake-bit effect

- when an investor faces big losses, it results in disappointment as well as loss of confidence on self

Momentum

- Observed tendency for rising asset prices or securities return to rise further, and falling prices to keep falling

Reversal

- past losers substantially outperforming past winners

Myopic Loss Aversion

- Implies the person also evaluates her portfolio frequently

- Intuitively, if you evaluate your position every day, there is a very good chance that by day’s end you will have lost money, so you find stocks very risky.

- But if you evaluate stocks once per decade there is a much smaller chance that you will lose money, so you will find stocks not so risky

Greater Fool Theory

Investors purchase stock in the hopes of offloading to someone else at a higher price

ADD

Illusion of knowledge

Mean reversion

Concepts

Agency Costs

- Direct costs: expenditures that benefit the managers but not the firms & costs arise from monitoring management actions

- Example: the cost of hiring outside auditors, business trips using a private jet instead of commercial flights

- Indirect costs: results from lost opportunities Example: managers of a firm that is an acquisition target may resist the takeover attempt because of concern about keeping their jobs, even if the shareholders would benefit from the merger.

EMH forms

- Weak form market efficiency prices reflect all the information contained in historical returns.

- With semi-strong form market efficiency prices reflect all publicly available information.

- Strong form market efficiency prices reflect information that is not publicly available, such as insiders’ information.

Random Walk vs Efficient Market Hypothesis

- Burton Malkiel: Yes, Random walk ➔ Efficient market hypothesis

- Richard Thaler says: No, Random walk Efficient market hypothesis

- (1) Prices generated by noise traders could be random but could be deviated from the fundamental value.

- large enough group of noise traders can form a sentiment and can influence the market

- (1) Prices are right (EMH) ➔ No free lunch (no arbitrage opportunity)

- (2) No free lunch Prices are right (EMH)

EMH and implications

Market efficiency requires that only one of the following three conditions need hold:

- Universal rationality

- Uncorrelated errors

- Unlimited arbitrage

- If the first holds, prices will be on average right and markets will be efficient.

- If the first does not hold, but the second does hold, while errors will be made, once again on average prices will be right.

- If the first two do not hold, but the third does hold, while prices have the potential to diverge from value because errors are often one-sided, arbitrageurs will notice such opportunities and swiftly take action so as to eliminate mispricing.

Limits to Arbitrage

- Fundamental Risk

- If you think a stock is underpriced you can buy it, but:

- You might be sideswiped by the market.

- Or maybe by the industry.

- Plus, there is idiosyncratic risk.

- Noise Trader risk Real world arbitrageurs cannot wait it out because as professional money managers they do not have long horizons – they are usually evaluated at least at once per year.

- Implementation costs

- In some cases, horizon is short but short-selling is:

- Expensive (commissions, spreads, price impact & fees for shorting stock)

- Difficult or even impossible (lack of availability regardless of fees; legal factors: many institutions cannot short)

Fundamental risk and noise-trader risk

- Fundamental risk arises because of the potential for rational revaluation as new information arrives and

- Noise-trader risk arises because mispricing can be more severe in the short turn. Some people may not be happy

Managerial Ease of Processing

- Conventional finance theory demonstrates that, when properly applied, NPV is optimal decision rule for capital budgeting purposes.

- Yet a number of surveys show that managers often utilise less than ideal techniques, such as the internal rate of return (IRR) and payback period

Managerial Overconfidence tendencies

- Overinvestment

- Unfounded belief in own ability to identify companies

- Overconfident managers invest more

- Higher Sensitivity of Investment to Cashflows

- Overinvestment when free cash is available

- Asymmetric information view - acting in the best interests of shareholders and noticing that the company’s shares are undervalued will not issue new shares to undertake investment projects.

- More Active in M&A

- Survey evidence documents that overconfident managers appear to be more active on the M&A front

- Too Quick to Start New Businesses

- Excessive optimism: overestimation of market demand.

- Better-than-average effect: “I will beat the odds.”

Managerial Overconfidence Positive aspects

- optimism about future cash flows leads to a belief that there will be little problem in covering interest payments

- entrepreneurial activity can provide valuable information to society. Provides valuable evolutionary purpose

Affect on Managers

- Emotion impacts capital budgeting decisions

- Kida, Moreno, and Smith experiment - participants were told that they were divisional managers deciding between two product investments

- Most chose the one with the lower NPV

Substances of emotional state

- Cognitive Antecedents

- beliefs or thoughts about a situation lead to emotional responses. For example, When another driver runs a red light and almost causes a collision, the belief that the other driver is careless and has endangered your lift triggers the emotion of anger

- Intentional Objects

- Emotions are about something specific, like a person or situation

- Physiological Arousal

- Hormonal and nervous system changes accompany emotional responses

- Physiological Expressions

- Emotions can be characterised by observable expressions that are associated with how a person functions

- Valence

- Valence is a psychological term that is used to rate feelings of pleasure and pain or happiness and unhappiness.

- Action Tendencies

- When you experience an emotion, you often feel an urge to act a certain way.

Emotion and Reasoning - Phineas Gage and Elliot

- Both men had brain damage to their frontal lobe which caused a major change in their personality/emotional processing skills, leading the scientists to have a better idea of how different parts of the human brain function, specifically regarding personality, emotions, social interaction, and the relationship between emotions and decision making

Advantages to Emotions

- Emotion pushes individuals to make some decision when making a decision is paramount.

- Often a decision has to be made

- Emotion can assist in making optimal decisions.

- Positive feelings can make it easier to access information in the brain, promote creativity, improve problem solving, enhance negotiation, and build efficient and thorough decision-making.

Value Advantage (4 reasons)

(Mistake of Judgement)

- They are committing judgment errors in extrapolating past growth rates too far into the future and are thus surprised when value stocks shine and glamour stocks disappoint. This is so-called “expectational error hypothesis”

- Because of representativeness, investors may assume that good companies are good investments

(Agency Considerations)

- Because sponsors view companies with steady earnings and buoyant growth as prudent investments, so as to appear to be following their fiduciary obligation to act prudently, institutional investors may shy away from hard-to-defend, out-of-favour value stocks.

- Also because of career concerns, institutional investors, who are evaluated over short horizons, may be nervous about tilting too far in any direction thus incurring tracking error. A value strategy would require such a tilt and may take some time to pay off, so it is in this sense risky.

Models for Momentum and Reversal

- DHS - Explains reversal - using calculations and related to overconfidence and variance terms

- GH Model - Explains momentum - using prospect theory, mental accounting and the disposition effect

- BSV Model - Explains momentum and reversal - using Anchoring and representativeness bias

BSV Model

-

Anchoring and conservative adjustment dictates that investors are slow to change views on earnings.

-

Investors, being coarsely calibrated, believe that stocks switch between two regimes.

-

Regime 1. Earnings mean-revert:

- Given a positive (negative) earnings change, there is a low probability of another positive (negative) earnings change in the next period. Underreaction.

-

Regime 2. Earnings are persistent:

- Given a positive/negative earnings change, there is a high probability of another positive/negative earnings change in the next period. Overreaction

- need more explanation

Factor Zoo

- proliferation of factors that have been identified as potentially explaining asset returns.

Equity Premium Puzzle

- Extreme Risk Aversion (Rational)

- Ambiguity Aversion (Behavioural)

- By factoring in both risk aversion and ambiguity (or uncertainty) aversion, a 5% equity premium becomes reasonable.

-

Myopic Loss Aversion (Behavioural)

Extreme Risk aversion

Rational explanation

- Coefficient of Relative Risk Aversion (CRRA) 30 compared to 1

Bubbles

A bubble occurs when prices are driven more by enthusiasm than fundamentals.

- Occurs naturally in the financial market, characterised by a rapid escalation in the market value of assets

Related

- Bubbles are identified in hindsight, leading to hindsight bias.

Learnings from Experimental Bubble Markets

- Price bubbles are more moderate and disappear faster when traders are experienced.

- Potential for short-selling leads to bubble dissipation.

- Willing to pay more for lottery asset because they become more risk taking as trading heats up

- traders may be subject to probability judgment error (overweighting small probabilities)

Excess Volatility Puzzle

It seems that often market movements are not obviously explained by new information.

Behavioral explanation

- Investors think (wrongly) that dividend growth changes are permanent rather than transitory. For this reason, they overreact

- Recency plays a role: recent high earnings growth makes people think that future growth is going to be higher than it actually turns out to be

Anomaly Attenuation

- It has been argued that a number of anomalies, once reported in the academic literature, either attenuate or disappear in the future.

Peer Group Evaluation

Becoming commonplace for managers to be evaluated relative to their size/value peer group -- relative to their style-peer group.

Style Investing

- If you believe that value is more often than not better you might tilt 60% towards value (style tilting)

- If you believe you have a predictive model that allows you to time style returns, you might be willing to toggle back and forth, 80% or 40% in value (style rotation)

Refining value Investing by using Accounting data

Joseph Piotroski

- Financial statement information can also be useful

- Developed a scoring system (F-Scores) on the level of financial soundness based on:

- Profitability

- Financial leverage/liquidity

- Operating efficiency

Refining Momentum-Investing Using Volume

- Volume as a Key Indicator - Volume predicts the magnitude and persistence of momentum

- Relationship Between Volume and Momentum

- Suggests momentum can be an overreaction and momentum and reversal are interconnected

- They found that low volume-high momentum firms yielded higher returns at 1.67% per month

Momentum Life cycle

Stocks with good past returns and high-volume exhibit patterns. Stocks peak, face bad news, and get sold at high volume. As stocks decline, volume decreases. On stock recovery, volume starts low but eventually increases as the stock gains attention.

Momentum and Reversal Study

Mark Grinblatt and Tobias Moskowitz Researchers performed a regression of returns on:

-

Past returns

-

Differentiating between winners & losers

-

And conditioning on consistency

-

Consistency matters:

- Firms with positive returns in at least 8 of the 11 (from -12 to -2) months showcase enhanced momentum.

- Firms consistently performing negatively over 8 of the 11 (from -12 to -2) months don't affect momentum.

Momentum and Value

- Simultaneous use of value and momentum is not maximally effective because:

- Value best suits low-momentum stocks.

- Momentum most effective for low-value stocks.

Multivariate approach (5 factors)

- Variables grouped into five categories: 1/risk; 2/liquidity; 3/price level; 4/growth potential; and 5/technical.

- Risk factors include such standard risk factors as beta and sensitivities to macroeconomic variables

- Illiquid stocks need to have higher returns to compensate traders who must face higher transaction costs, so such logical factors as price per share and volume were included

- Price level factors essentially capture value strategies, as this category includes share price relative to various accounting magnitudes

- Growth potential factors point to the likelihood of higher growth in earnings and dividends, with various profitability measures being used as proxies in this regard

- Idea here is that, for a given price relative to accounting measures, indicators suggesting higher future growth might point to diamonds in the rough

- Technical factors include standard momentum and reversal measures

Study results

- momentum & reversal, value and volumes are the three values that are most important

Style rotation strategies

- Necessity: Reliable predictive models are foundational for investment approaches.

- Key Macroeconomic Factors:

- Default premium

- Term structure slope

- Aggregate dividend yield

Can Behavioural Finance Enhance Portfolio Performance

- No strong evidence that behavioral investing has significant benefits.

- Issues with sample size and statistical test power; funds might provide value, but it's challenging to conclusively determine.

Home Bias and Informational Advantage

- You know more about what is close.

- Gains from being local to a company may appear in improved monitoring capability and access to private information.

Calculations to revise

CAPM, expected return and CML/SML

Expected Value, Expected Utility and certainty equivalent

Non-linear weighting function

Camerer and Lovallo experiment

Demand curve in overconfidence

Bayes Rule & Base rate neglect

REVISE CFA questions tutorial 7

REvise tutorial 8 question 3 and 4

Revise CFA questions tutorial 8

Revise CFA questions tutorial 9

DHS model

- Explaining Reversal through overconfidence

- calculations

Fama-French Three Factor Model

Consists of three factors

- Market Return:

- Value vs. growth

- Small cap vs. large cap

Myopic Loss Aversion illustration

- Revise confidence interval approach