Lecture 13

Exam Revision

- Topic 1: Intro to Behavioral Finance : Introduction to Behavioral Finance and Traditional Finance Theories

- Topic 2: Prospect Theory

- Topic 3: Challenges to Market Efficiency

- Topic 4: Overconfidence and Investors

- Topic 5: Application of Managerial Overconfidence in Corporate Finance

- Topic 6: Heuristics and Biases and Its Implications

- Topic 7: Emotional Foundations and Individual Investors

- Topic 8: Behavioural Explanations for Anomalies

- Topic 9: Behavioral Factors and Stock Market Puzzles

- Topic 10: Behavioural Investing

Topic 1: Introduction to Behavioral Finance and Traditional Finance Theories

Reference: AckertDeaves Chapters 1 & 2

[Part One – Introduction to Behavioral Finance]

- Overview of neoclassical economics

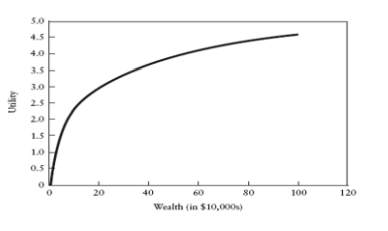

- (1) Preference Relation

- (2) Utility Function and Expected Utility Theory

- (3) Brief Introduction to Behavioural Finance

[Part Two – Foundations of Finance]

- Foundations of Finance II: Asset Pricing, Market Efficiency and Agency Relationships

- (1) Risk and Return Relationship

- (2) CAPM model and Fama and French

- (3) Market Efficiency (brief introduction = > more details in Topic 3)

- (4) Agency Relationships and Corporate Governance

Part One

Neoclassical economics (normative theory)

- Rational preferences

- Completeness

- Transitivity

- Maximise utility

- The Expected Utility Theory of Prospect

- Properties of Utility Functions

- Certainty Equivalents

- Independent decisions based on all “relevant” information

Introduction to Behavioural Finance

- Loss Aversion

- Representative

- Mental Accounting

- Fear of Regret

- Introduce neoclassical economics (traditional)

Part Two

Foundations of Finance

- Portfolio Risk & Return

- Security/Portfolio Expected Return & Standard Deviations

- Efficient Frontier & CML

- CAPM Model

- Market Efficiency (more discussed in Lecture 3)

- Agency Relationships & Corporate Governance

- Agency Costs (Direct vs Indirect)

- Some of the foundations concepts in finance

- EMH - need to know

- not in the way of other finance courses, not the same as CAPM or EMH

Topic 2: Prospect Theory, Framing and Mental Accounting

Reference: AckertDeaves Chapters 3

[Part One – Prospect Theory]

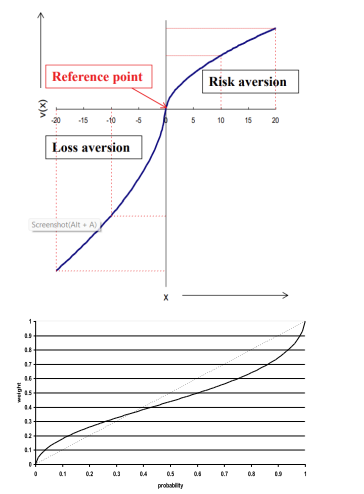

- Overview about Prospect Theory

- (1) Risk Aversion vs. Risk Seeking

- (2) Development of Prospect Theory

- Prospect Theory Value Function

- The Weighting Function

[Part Two – Mental Accounting]

- Mental Accounting

- (1) Integration vs. Segregation

- (2) Theater Ticker Problems

- (3) Opening and Closing Accounts

- utility function is upper sloping

- reference dependent

- Treat positive versus negative domain differently

Prospect Theory

- Risk aversion vs Risk seeking vs Loss aversion

- Value Function

- Reference dependent

- Risk averse in positive domain

- Risk seeking in negative domain

- Loss aversion

- Weighting Function

- Overweighting low probabilities

- Underweighting medium-high probabilities

- Certainty effect

- Framing & Mental Accounting Effect

- Segregation vs Integration (reference point)

- Silver lining effect & House money effect

- Influence our decision to be less rational

Topic 3: Challenges to Market Efficiency

Reference: AckertDeaves Chapters 4

[Part One – Efficient Market Hypothesis]

- Overview of Efficient Market Hypothesis

- Theoretical foundations and assumptions

[Part Two – Challenges to Market Efficiency]

- Rationales supporting the Efficient Market Hypothesis

- Theoretical Challenges and Empirical challenges

Market Efficiency

- 3 levels of efficiency

- Implications: Better off do passive investing

- Random Walk vs. EMH

- “Prices are right” vs “No free lunch”

- Theoretical Foundations

- Universal Rationality

- Uncorrelated Errors

- Unlimited Arbitrage

- Rationales Supporting Efficiency vs

Effective Trading Rules (Anomalies?)

- Challenges to EMH

- under EMH, universal rationality

- As long as we have unlimited arbitrage, it is ok too

- Have limits to arbitrage, however

Arbitrage

- Triangular Arbitrage

- Limits to Arbitrage

- Fundamental Risk

- Noise-trader Risk

- Implementation Costs

Topic 4: Overconfidence & Investors

Reference: AckertDeaves Chapters 6 & 9

[Part One – Overconfidence]

- Overview about Overconfidence

- Miscalibration / Other Strains of Overconfidence

- Factors Impeding Correction

[Part Two – The Impact of Overconfidence on Financial Decision-making]

- Overview: The Impact of Overconfidence on Financial Decision-making

- Overconfidence and Excessive Trading – A simple Model

- Under diversification and excessive risk taking

Overconfidence

Strains of Overconfidence

- Miscalibration

- Calibration Tests

- Confidence Interval Approach

- Better-Then-Average Effect

- Illusion of Control

- Excessive Optimism

Impact on Financial Decision-Making

- Excessive Trading

- Unfounded belief in own ability to identify companies

- Under Diversification

- Underestimating downside risks

- link with investment decision

- overconfidence - what it really is

- Different strains of overconfidence

- Miscalibrated - mean value and range tests

- Expected value you predict to have

- 95% confidence interval, giving a narrow range indicates you think your answer is correct

Any questions asking about overconfidence

- If the question is not specific about a strain - saying they are saying

- really specific strain - then be specific

- EXAM TIP - asking for more general bias, in particular 'showing' illusion of control e.g.

- Don't give extra assumptions

Impact on decision making

- underdiversification - illusion of control - maybe a bit of miscalibration

- underestimation of the risk that they may encounter

Topic 5: Application of Managerial Overconfidence

Reference: AckertDeaves Chapters 6 & 9

[Application of Managerial Overconfidence]

- Brief Introduction: Application of Managerial Overconfidence

- Capital Budgeting:

- Payback and Ease of Processing,

- Allowing Sunk Costs to Influence the Abandonment Decision,

- Allowing Affecting to Influence Choices

- Managerial Overconfidence

- Investment and Overconfidence

- Can Managerial Overconfidence have a Positive Side?

Managerial Overconfidence

Capital Budgeting

- Ease of Processing

- Loss Aversion (Abandonment)

- Sunk Costs

- Ex-Post Mistake

- Attachment/Involvement

- Affect

Managerial Overconfidence

- Overinvestment

- Unfounded belief in own ability to identify companies

- Higher Sensitivity of Investment to Cashflows

- More Active in M&A

- Too Quick to Start New Businesses

- CEO Overconfidence Not All Negative

- institutional - more knowledgable

- Still exhibit overconfidence but for different reasons

- Managers decision can be affected

- Capital budgeting

- Should act in the best interest of shareholders

- Make decision based on the best approach - may choose the other because it is easier

- Loss Aversion

- Start an investment, do not stop evaluation

- Should not continue, stop/terminate it but do not because of loss aversion

- Take into account sunk cost

- Treat it as the money that you pay

Affects will influence decision making as well

- may choose something suboptimal but may have a positive feeling

Managerial overconfidence

- Tend to overinvest

- Higher sensitivity to cashflows

- Not all overconfidence is bad

Topic 6: Heuristics & Biases

Reference: AckertDeaves Chapters 5 & 8

[Part One – Application of Heuristics and Biases]

- Brief Introduction: Application of Heuristics and Biases

- Perception, Memory and Heuristics

- Familiarity & Representatives and Related Heuristics

- Anchoring; Irrationality and Adaptions

[Part Two – Implications of Heuristics and Biases for Financial Decision-Making]

- Introduction: Implications of Heuristics and Biases for Financial Decision-Making

- Financial Behavior Stemming from Familiarity & Representativeness

- Anchoring to Available Economic Cues

Part One

-

Perception & the Frame

- Primacy vs Recency Effects

-

Heuristics (Mental Shortcuts)

- Type 1 (Autonomic)

- Type 2 (Cognitive)

- E.g. Ambiguity Aversion, Endowment Effect

-

Representativeness

- Conjunction Fallacy (Joint Probability)

- Base Rate Neglect (Bayes’ Rule)

- Hot Hand Phenomenon & Gambler’s Fallacy

- Overestimating Predictability

-

Bias Related to Representativeness

- Recency

- Salience

- Availability

-

Anchoring

- Seems contradicting with Representativeness

- Coarsely Calibrated

- perceptions will effect how we evaluate situations

- different heuristics

- not always influenced by primacy or recency effects

- Time gap in between, more effect by the latency effect

Heuristics

- Mental shortcuts

- not the same as mental biases

- Type 2 heuristics can override type 2 decision

Representativeness

- Two most important is conjunction fallacy and base rate neglect

- Conjunction

- thinking the joint has a higher probability that the base rate

- Base rate neglect

- Conditional probability - forecasting rent e.g.

- Adding new information, influenced and miscalculate the base rate

- Difficult calculations from the course

Hot hand phenomenon

- Really good past performance, high chance they are going to perform good in future

Gamblers fallacy

- complete opposite

Overestimating predictability

- Overestimating the predictability of using one to predict the other

Salience

- What information are we using to represent something else

- More dramatic, going to be in your memory more

Availability

- Easier to recall, effected by that more

Anchoring

- not adjusting

- contradicting representativeness

- Which is more influence by later information

- More effected by new information

- Can suddenly switch to representativeness

Part Two

- Home Bias

- Implied Under Diversificaiton

- Language & Culture

- Information Advantage

- Representativeness

- Good Companies vs. Good Investments

- Anchoring

- Momentum-Chaser vs. Contrarian

- tend to under-diversify our portfolio

- nationally - know language/culture, safer decision

Representatives

- Tend to think good companies are good investments

- Good management characteristics, making good products

- Should already be reflected in the price

- Good companies does not mean they are good investments

Momentum anomalies

- Look at momentum,

- see something increasing, believe it is going to decrease

Topic 7: Emotional Foundations and Individual Investors

Reference: AckertDeaves Chapters 7 & 10

[Part One – Emotional Foundations]

- Brief Introduction: Emotional Foundations

- The Substance of Emotion

- Cognitive Antecedents; Intentional Objects, Physiological Arousal; Physiological Expressions; Valence; Action Tendencies

- A Short History of Emotion Theory

- Evolutionary Theory

- The Brain / Emotion and Reasoning

[Part Two – Individual Investors and the Force of Emotion]

- Brief Introduction: Individual Investors and the Force of Emotion

- Is the Mood of Investor the Mood of the Market / Pride and Regret

- The Disposition Effect (Important)

- House Money / Affect

Emotions

-

Substance of Emotion (6 of them)

-

History of Emotion Th

- Evolutionary Theory

-

The Brain

-

Emotion & Reasoning

- Phineas Gage & Elliot

-

Emotion is not all Bad

-

Pride & Regret

-

Disposition Effect

- Tendency to sell the winners too early and hold on to losers too long

- Explain using Prospect Theory & Mental Accounting

-

Sequential Decisions

- House Money Effect (Winning)

- Snake-Bit Effect & Break-Even Theory (Losses)

-

Affect

- Six things to meet an emotion

History of emotion theory

All treated as a conscious response

Evolutionary theory treated differently

Communicate more effectively

- Can be a reaction

NOT TESTED ON BRAIN

Frontal lobe effecting emotion

Emotions help you make decisions and negotiate better as well

Pride and regret

- Linked to loss aversion

Disposition effect

- Emotional side, because of pride and regret

- tendency to sell winners early and hold onto losers

- risking seeking and risk aversion aligning with prospect theory

Sequential decisions

- contradiction with prospect theory

- Don't have a proxy to identify sequential decisions

Snake bit effect

- Loss now, dont want to lose more

Break-even

- more risk-seeking to regain the losses

Topic 8: Behavioural Explanations for Anomalies

Reference: AckertDeaves Chapters 13

[Behavioral Explanations for Anomalies]

- Brief Introduction: Behavioral Explanations for Anomalies

- Earnings Announcements and Value vs. Growth

- What is behind lagged reactions to earnings announcements

- What is behind the value advantage

- What is Behind Momentum and Reversal

- Daniel -Hirshleifer -Subrahanyam Model

- Grinblatt -Han Model and Explaining Momentum

- Barberis -Shleifer -Vishny Model and Explaining Momentum and Reversal

- Rational Explanations

- Important Risk Adjustment

- Fama-French Three Factor Models/Factor Zoo – Tutorial

Anomalies

- Value Premium

- Mistakes of Judgment

- Agency Considerations

- Momentum & Reversal

- DHS Model (Reversal)

- GH Model (Momentum)

- BSV Model (Momentum & Reversal)

- Rational Explanation

- Inappropriate Risk Adjustment

- Fama-French 3 Factors Model

- Factor Zoo Concern

- Value firms outperform growth firms

- Value firms tend to sell at a cheaper price

- How do you know they are undervalued?

- Doesn't work with traditional model

Mistakes on Judgement

- Error in expectations

- Growth stocks will perform a lot better

- representativeness

- Talking about portfolio performance in general

Agency

- growth stocks portfolio for agency issue

- easier to explain for investors

- Value stocks to realise returns takes longer

Momentum and reversal

- Momentum is the underreaction

- reversal is the overreaction

- DHS - overconfidence

- Calculations, rational investor will predict the price

- GH

- Not adjusting reference point quickly enough

- Reference point is not adjusting quick enough to fundamental value

- Underreaction, not to the fundamental because the reference point is not changing

- Do not worry about big equations, but understand how it works

BSV

- Overreaction and underreaction

- Even though share price should be random walk, cannot predict future

- Believe market is in regime 1 or 2, changing or persistent

- belief effects reaction to past earning

- In regime 1, underreact to past earning signals

- Underreact to new information

- Regime 2, overreact - positive is going to continue

Factor Zoo

- Other things included

- Include all different factors (over 300 in some model)

- Really identifying new factors,

Topic 9: Behavioural Factors & Stock Market Puzzles

Reference: AckertDeaves Chapters 14

[Behavioral Factors and Stock Market Puzzles]

- Brief Introduction: Behavioural Explanations for Stock Market Puzzles

- Equity Premium Puzzle

- The Equity Premium

- Why is the Equity Premium a Puzzle?

- What Can Explain This Puzzle?

- Real-World Bubbles

- Experiment Bubble Market

- Design of Bubbles Markets

- What can we learn from these experiments?

- Excessive Volatility / Markets in 2008

Puzzles

- Equity Premium Puzzle

- Extreme Risk Aversion (Rational)

- Ambiguity Aversion (Behavioural)

- Myopic Loss Aversion (Behavioural)

- Bubbles

- Greater Fool Theory

- Excessive Volatility

- Overreaction

- Recency Effect

- Equity earns higher returns for given risk level

- investors have to be extremely risk averse

- Behaviour averse and ambiguity averse

- Don't want to engage in something that we don't have some degree of control

- More reluctant to join

Myopic

- more frequently you evaluate, to more risky it appears

Bubbles

- False belief in fundamental stuff

- Price continue to increase - more unrealistic

- greater fool theory, people jumping in and pushing the price further away

- Investors more experienced, more motivated and can disappear quicker

- Short selling will make bubbles disappear faster as well

Excessive volatility

- Public information effects market price

- market is more volatile than what the market says

- Overreaction

- Growth rate, be only for a short period of time

- Treat that as a permanent change

- overreact to negative or positive news

Recency effects

- rely on new information too much

- Causing overreaction to current information

Topic 10: Behavioural Investing

Reference: AckertDeaves Chapters 19

- 10-1: Anomaly Attenuation, Style Peer Groups, and Style Investing

- 10-2: Refining Anomaly Capture:

- Refining Value Investing using Accounting Data

- Refining Momentum-Investing using Volume

- Momentum and Reversal (Value)

- 10-3: Multivariate Approaches

- 10-4: Style Rotation

- 10-5: Is It Possible To Enhance Portfolio Performance Using Behavioral Finance

- Early Evidence

- What is Behavioral Investing

Puzzles

-

Anomaly Attenuation

- Anomaly dissipation is expected in efficient market

-

Peer Group

-

Style Investing

- Style Tilting vs. Style Rotation

-

Refining Value Investing (Accounting Data)

-

Refining Momentum Investing (Volume)

-

Momentum & Reversal

- Term Structure & Consistency

-

Momentum & Value

-

Multivariate Approaches

-

Can Behavioural Finance Enhance Portfolio Performance?

- No Conclusion

Anomalies

- Not behaving the same as EMH

- Should use it to capture profits

Peer group Evaluation

- Based on strategies - linked to style investing

- Should still diversify

- Tilting, more general - add slightly more in value firms

- rotation, more aggressive, based on short term evaluation

Refine value investing

- Simply using accounting data with F-score

Momentum

- Capture momentum cycle, capture the timing to enter/buy stock

- Capture using volume

Momentum and reversal

Momentum and Value investing

- Do not see these effects, capturing different things, small portfolio capturing both criteria

Multivariate

- look at all the factors

- separate into five categories, found that we can outperform the market

- momentum, value and volumes are the three values that are most inportant

Does behavioural finance actually work?

- not providing strong evidence suggesting otherwise

Final Exam

- Final examination will be held centrally by the University at the specified time. The final exam will be a face to face on campus exam.

- There is NO formula sheet attached to the exam

- Reading: 10 minutes

- Duration: 120 minutes

- Format: Short answer, Short essay, Problem solving

- Task Description: The final assessment will be based on all materials covered in the course (from Topics 1-10). The exam includes short answers, short essays, and problem-solving questions. No MCQ

- need to know how to apply that in a scenario

How to Prepare for the Exam

- Go through the slides in detail (including examples)

- Practice lecture examples, tutorial questions, & practice exam and try to get a deep understanding of the examples and questions.

- Read the reference chapters of the textbook and other references (for the relevant content)

- It is more important to understand the concepts and know how to apply them, rather than simply memorising the definitions (won’t give you full marks)