Lecture 4 - Overconfidence

Information, probability and cognitive biases

- People tend not to use probabilities correctly:

- People are overconfident about themselves.

- People overstate the probability that they are right.

- People tend not to process information correctly:

- If information is boring, mundane, or commonplace, people tend to under-react to it.

- If information is exciting or dramatic, people tend to overreact to it.

- People also tend to look for information that is consistent with their view and ignore information that is inconsistent.

Does this matter in financial markets?

- We don't use probabilities correctly

- normally overconfident about ourselves

- overestimate the probability to be higher than true probability

Looking at something boring/unexciting - underreact

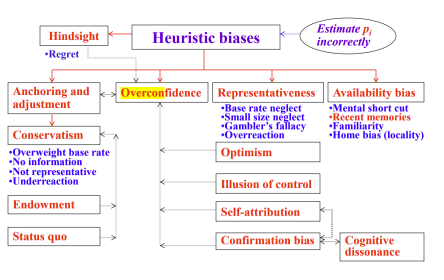

Overconfidence Overview

Overconfidence: unwarranted faith in one’s intuitive reasoning, judgments, and cognitive abilities.

- Subjects overestimate both their own predictive abilities and precision of information they have been given.

- People think that they are smarter and have better information than they actually do.

- Overconfidence: regardless of primary knowledge, secondary knowledge is overestimated. (People tend to overestimate the probability that they are right. Thus, they are surprised more often than they think.)

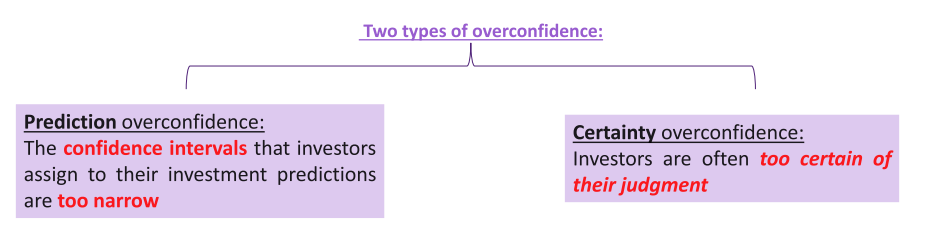

- prediction is more accurate than true abilities

- Prediction overconfidence - precision of information

- Certainty overconfidence - more linked to overconfidence of predictive abilities

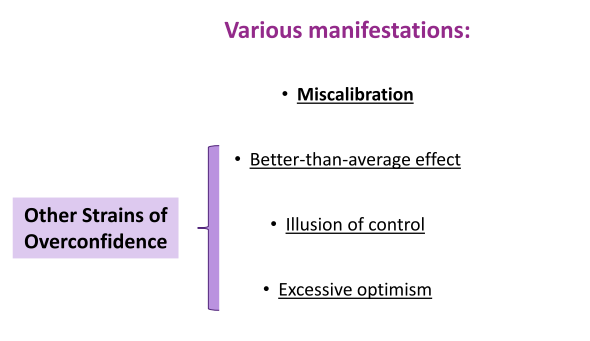

Trend of overconfidence - miscalibration

Confidence vs. overconfidence

- Confidence is all about having a positive feeling about your skills, knowledge, etc.

- But overconfidence is when you have an inflated sense of your abilities.

- More than what you should have - inflated sense of abilities

May show different traits of overconfidence

- Assignment/final exams, don't want to over-claim something

Calibration-based overconfidence

Miscalibration is the tendency for people to overestimate the precision of their knowledge.

- It normally implies thinking that your knowledge is more accurate than it really is.

- Two ways to measure

- Calibration tests e.g. You get 20 multiple choice questions in your mid-exam

- Then ask how many you answer correctly. And compare the two numbers

- If you think you got 20 right (100%) …but you only got 10 right (50%).

- You appear to be overconfident

how certain you are at something

- practise exam, ask them how you felt, and compare with what you actually got

-

Confidence interval approach Confidence interval: an interval that is expected to contain the parameter being estimated. (e.g. 95% confidence interval → 5% chance of being wrong) Suppose individuals are asked to construct 90% confidence intervals (e.g., height of Mount Everest, the level of the Dow in a month, etc.).

-

If an individual is asked a large number of questions (sampling error is reduced by asking a sufficiently large number of questions), then proper calibration implies that about 90% of their confidence intervals should contain correct answers to the questions.

-

Or, focusing on a particular question that is asked of a large number of respondents, if the group as a whole is properly calibrated, 90% of these individuals should have confidence intervals bracketing the correct answer.

Looking at the range - not a given prediction

- give a range on a question

- want to see if the correct answer is within the range or not

- ask multiple questions

- Get more than one question incorrect

- range too narrow, causing it to be incorrect

Ask height of Mt Everest:

- 90% of people should give me the correct answer

- If less than 90%, showing traits of overconfidence

- Total accuracy is less than the confidence interval that we want

The reality turns out to be quite different.

- A percentage of individuals usually markedly below x% produces intervals that bracket the true answer. The same holds at the level of the individual.

- In sum, calibration studies find that the confidence intervals that individuals provide are too narrow, resulting in correct answers lying within the confidence ranges less often than an accurate sense of one’s limitations would imply.

- Overestimating the accuracy of your judgement by giving a narrow range

Better-than-average effect

Refers to the tendency for a person to rate themselves as above average.

- Many of us feel we are smarter or more skilled than average, but only 50% of us can really be better than average.

- Evidence suggests that people pick a definition of a task that suits their purpose.

- On the cognitive side, the performance criteria that most easily come to mind are often those that you are best at.

- More ambiguity - often have tendency to think they are better than the average

Illusion of control

The tendency to think that there is more control over events than can objectively be true

- For example, gamblers may think that they can control the outcome of the dice or the cards, or people actually believe that the risk of infection is partly a function of the character of the person that they are coming into contact with.

- Doing all these different things to try and win

- People have illusion of control over things purely determined by chance

- With financial markets, think have more control to fix/change markets

- Do things to make up loss/create more revenue

Excessive optimism

- Reflects the feeling that things will be rosier than objective analysis suggests.

- When people’s predictions about the future are unrealistically optimistic.

- In essence, people assign probabilities to favourable/unfavourable outcomes that are too high/low given historical experience or reasoned analysis.

- Think future outcome if going to go better than you think

Excessive optimism and miscalibration can go hand in hand.

Suppose you purchase a stock:

- True distribution for the return on this stock over the next year entails an expected return of 10%, with a 90% confidence range of -10% to 30%

- Your (optimistic) distribution, has an expectation of 20%, with a 90% confidence range of 10% to 30%

- Stock portfolio, analysis information/consensus

- Return of stock is 10% - not guaranteed to get it

- Optimism thinks it will be 20%, overestimating the main value

Evidence on excessive optimism:

- Students expect to receive higher marks than they actually receive.

- Overestimates the number of job offers that they will receive.

- People think they can accomplish more than they actually end up accomplishing.

- Individuals assume that costs will align with initial estimates.

Subject to the planning fallacy

In reality, many of us fall short of our work goals on a regular basis, and budget overruns are a common feature of large public projects

- The Sydney Opera House, for instance, was supposed to be completed in 1963 at $7 million. Instead, it was finished 10 years later at $102 million.

- Happens to most people - irrational

- Because of planning fallacy

- Sydney opera house - normally expect projects to run overbudget and overtime

Costs of excessive optimism:

- Inability to meet one’s goals can lead to disappointment, loss of self-esteem and reduced social regard.

- And time and money can be wasted pursuing goals that are unrealistic.

- Psychological - feel bad/disappointed

- Some actual costs as well - mindful of behavioural factors

Problems with measuring overconfidence

Most people most of the time appear to be overconfident.

- But overconfidence does not seem to be universal.

- Under confidence is common on easy tasks

- Also, depending on the metric, it is possible for people to be judged overconfident using one metric but not using another.

- And there is no universally accepted way to measure overconfidence

- Human factors in real life - hard to quantify it

- Hard to provide a direct relationship with overconfidence

- Psychology - perform tests, create samples

- Different tasks/different levels of information, different levels of confidence

We are not all equally overconfident.

- Male vs Female

- On a survey men and women were asked what they expected the market return and their own portfolio return to be in the following 12 months.

- Both men and women expected their portfolios to outperform the market – but the gap was greater for men

- Education Level & Income Level

- Don't have a universally accepted way to handle overconfidence

- overconfidence levels varies by income, gender, education, etc.

Factors Impeding Correction

Why don’t we learn?

- Self-attribution bias retards the learning process by allowing us to embellish our triumphs while forgetting our defeats.

- Hindsight bias: says we knew what was going to happen when we really didn’t.

- Confirmation bias: the tendency to search out evidence consistent with one’s prior beliefs and to ignore conflicting data.

These effects suggest that overconfidence can evolve over time.

Overconfidence may not be all bad

Research has shown that predictions about the future tend to be more optimistic when:

- Goals are far off

- A course of action has been committed to

- When these conditions are met, excessive optimism may be useful in enhancing performance.

We have other biases affecting how we correct ourself

We attribute the success to our own abilities

- Fail because of things outside your control

Self attribution bias - blaming other things (you do not think the error is because of you)

- Headache, bad weather etc.

Hindsight beliefs

- Thinking we knew what was going to happen when in reality we didn't

- Looking for things supporting

- hand-in-hand with self-attribution bias - error happened because it was outside of your control

Overconfidence is not always bad

- Something you want to achieve is far away

- Course of actions committed to it

- Being overconfident can enhance the performance

- Optimistic, setting a goal for the future, can be better fort long term goals

Part Two: The Impact of Overconfidence on Financial Decision-making

Overconfidence: (Negative) Implications for (retail) investors

- Unfounded belief in own ability to identify companies as potential investments: blind to any negative information

- suggestion: review trading records of past two years and then calculate the performance of your trades.

- Excessive trading: lower returns

- suggestion: keep track of each and every investment trade and then calculate the returns.

- Underestimating their downside risks: surprise on underperformance

- suggestions: (1) review investment holdings for potential poor performance; (2) realized how volatile the markets are

- Portfolio under diversification: taking on more risk

- suggestion: recall that numerous, once-great companies have fallen; what is the optimal portfolio without current holdings?

- retail investors - individual investors

- Focus on retail investors only

- overestimating ability to identify good/bas investment

- Cause people to engage in excessive trading

Excessive trading

- Loss to overall performance

Overconfidence and excessive trading

Theoretical models indicate a relationship between overconfidence (OC) and extent of trading. To get a flavor, consider 3 investors:

- High-OC investor: HOC

- Low-OC investor: LOC

- No-OC investor (accepts whatever the market tells him): PC (Proper Calibration).

- At the level of the individual, demand will be a function of the investor’s estimate of the security’s (intrinsic) value.

- If the investor believes that the value ( ) exceeds the market price (), he/she will wish to hold more of the security than if the security was perceived to be fairly priced.

- Let equal the (neutral) number of shares that an investor would hold if price and value were

equivalent ().

- If the value exceeds the price, the investor will want to hold more than q n shares.

- If value falls short of the price, the investor will want to hold less than q n shares.

- React accordingly if you think the value of the firm is over/undervaluated

Overconfident Traders

- First assume that since there are many investors, all are price-takers. Further, we will assume that when estimating value, an investor uses two items of information, his own opinion (prior value) and the market price (which is the weighted average of all investors’ opinions), as follows:

(Equation 9.1)

Where:

- is the (posterior) estimate of value of investor ;

- is the same investor’s prior estimate of value;

- is the market price; and is the weight (i.e., level of overconfidence) investor puts on his prior relative to the market price.

The higher is, the higher is the weight an investor puts on his own opinion.

Since there is a very large number of investor views determining p, any value of more than slightly above zero suggests some overconfidence, with higher values suggesting more overconfidence than lower values.

- not a noise trader or arbitrageurs

- represents the level of overconfidence you are

- 1 indicates market price has no influence on your opinion

- Suppose that the demand curve can be written as:

Where:

- is investor i’s demand (i.e., quantity)

- is the sensitivity of demand to a divergence between the posterior value estimate and price.

Substitute (Equation 9.1)

into (Equation 9.2):

- Next take the partial derivative of with respect to p:

- The higher the investor’s level of overconfidence () the more responsive demand is to changes in price.

- As approaches one, which means market price has no influence, the closer is to

- On the other hand, as moves toward zero, the demand changes little when the price changes.

is 0, 0 change in quantity when there is a change in price

- Doesn't matter what the price changes

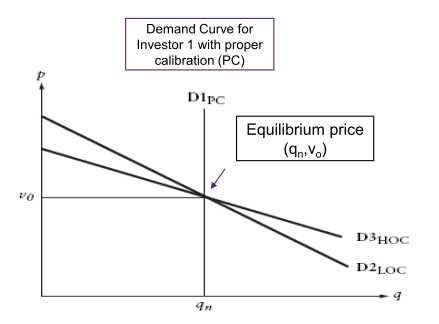

Overconfidence, excessive trading and demand curves

On this graph, their Demand curves (D) for a given security are depicted.

These are labelled D1PC, D2LOC & D3HOC, where “PC” refers to “proper calibration,” “LOC” refers to “low overconfidence,” and “HOC” refers to “high overconfidence”.

As has been discussed, a more overconfident investor in this context is one who more strongly believes in his ability to appropriately value the security. The three investors are similar in some respects. They all analyse the security in question and arrive at the same prior value estimate, which is designated as in the v 0 graph.

PC - rational investors - vertical straight line for demand curve

- doesn't matter the price, will always hold a neutral quantity

- overconfident

Difference between 3 investors:

They respond differently to prices that are different from their value estimates.

- Investor 1 (PC) slavishly maintains his holding regardless of price changes: this investor wishes to hold q n at any price.

- Other two investors have negatively-sloped demand curves, implying willingness to “march to beat of a different drummer.”

- Investor 2/3 pays some/most attention to own opinion.

Consider what happens as the price changes:

- Higher OC leads to more trading for a given value vs. price gap The more overconfident is the market the greater will be volume at level of market.

- The lower the price, the less you want to purchase

- more overconfident, the more you want to purchase

Evidence from the Field

Do people trade because of knowledge or knowledge perception?

Several related studies documented trading losses that were perhaps attributable to overconfidence.

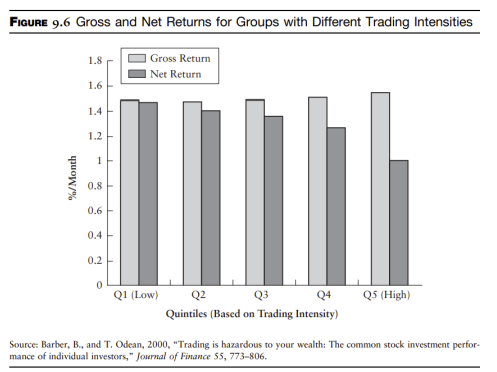

- 60,000 households during 1991-96.

- Look at gross and net transaction cost returns.

- For both raw returns and risk-adjusted returns, they find that the high quintile group have higher gross return.

- However, their net risk-adjusted return was below the market return. Those trading the most frequently earned an average annual return of 11.4% vs. the market return of 17.9% (underperformed the market).

- Greatest offenders were men.

- More trading you get into, the less return you will get

- Link to EMH

Overconfidence and excessive trading?

This evidence only indirectly links trading and overconfidence.

- How do we know that it is overconfidence that is driving excessive trading? Studies from surveys and the lab try to establish a direct relationship between overconfidence and trading activity.

Experimental evidence

In an experimental study correlation between various forms of overconfidence and trading activity was also investigated.

-

Participants first filled out questionnaires eliciting their level of overconfidence.

-

Then trading sessions were conducted:

- Subjects were endowed with cash plus stocks (with random dividends) that they could trade

- Private signals of true dividends

- Most accurate people were given the least noisy signals Point was to see if overconfidence and trading activity were correlated. Other variables were also investigated.

-

Specification (1), they found that both miscalibration and the better-than-average effect led to more trading. No significant effect was found for illusion of control.

-

Specification (2) explored additional determinants of trading activity beyond overconfidence measures. Older participants with more financial education traded less.

-

On the other hand, those with real-world trading experience felt more comfortable “pulling the trigger” and hence traded more.

- More trading, but don't find evidence for IOC; the reason why they are overtrading is because they are overestimating their abilities because they think they are better

- More skillful than average person

Different demographics

older, less frequent trader

- more performance

- more Risk averse

More educated

- engage less in excessive trading

Engaging a lot more

Under-diversification and excessive risk taking

- Rationally speaking, diversification is beneficial, and investors are better off investing in a well- diversified index fund.

- However, a study found that people under-diversify, and this under-diversification was less severe among people who were financially sophisticated.

- Diversification increased with income, wealth, and age, and those who traded the most also tended

to be the least diversified.

- Perhaps overconfidence is the driving force behind both excessive trading and under-diversification

Underdiversification

- better to hold the index fund?

Get rid of systematic risk through diversification

If you think a company if going to perform well, why would I diversify my portfolio?

- Don't spread the risk

We cannot overclaim this - we cannot prove this definitively

Research

- In one study, the portfolio composition of more than 3,000 U.S. individuals was examined.

- Most held no stocks at all. Of those households that did hold stocks (more than 600), he found that the median number of stocks in their portfolios was only one.

- And only about 5% of stock-holding households held 10 or more stocks.

- Most evidence says that to achieve a reasonable level of diversification, one has to hold more than different stocks (preferably in different sectors of the economy).

- Thus, it seems clear that many individual investors are quite under-diversified.

If you have more financial knowledge, engage in more diversification

Analysts and excessive optimism

- Research has established that analysts tend to be excessively optimistic about the companies that they are following (textbook table 9.2).

- True both in the U.S. and internationally.

- A lot more buy recommendations than sell (e.g. the US: 52%/3%, Germany: 39%/20%)

- Another interpretation: conflict of interest and desire to keep prospective issuers happy.

- Use information from financial managers to come up with financial recommendations

- undervalued, overvalued, buy/sell

Overconfidence - a lot more buy recommendations than sell

- Could also be a conflict of interest - when given the financial information of the company, want to be given a buy recommendation to boost share price

- please the issuer of the information

Conclusion

- Overconfidence: regardless of how much they know, people overestimate how well they know their limits.

- 4 manifestations: Miscalibration, better-than-average, Excessive Optimism, and Illusion of Control.

- Different biases make it hard for us to learn and correct overconfidence.

- However, overconfidence may not be all bad.

- Overconfident investors tend to engage in excessive trading and under-diversification.

- Analysts tend to show excessive optimism as well.