Lecture 5

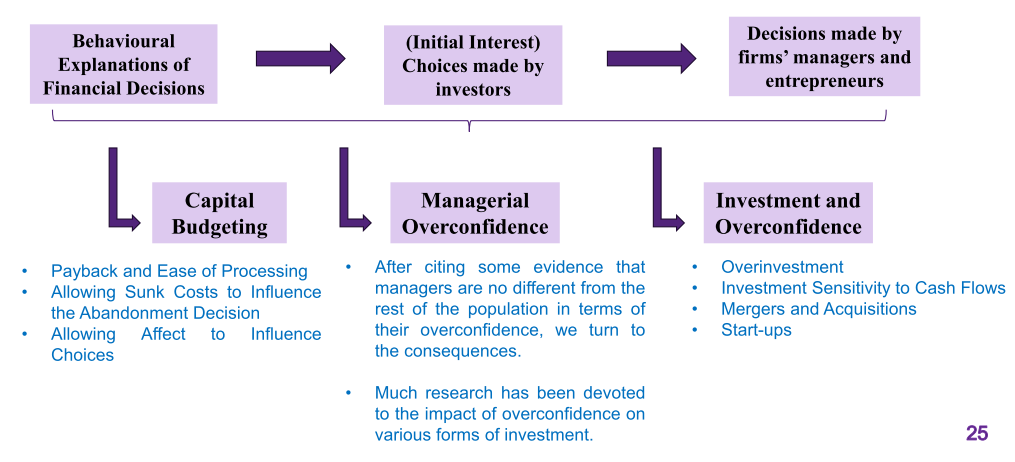

Application of Managerial Overconfidence

Capital budgeting errors:

- Ease of processing…

- May lead to inappropriate adoption rules

- Loss aversion…

- May lead to problems with abandonment

- Affect…

- May cause managers to avoid profitable investments

Specifically, we consider

- the still wide-spread use of (patently inferior) payback as a project selection technique,

- the tendency to throw good money after bad (sunk costs),

- and the proclivity to allow irrelevant information to influence project adoption.

Conduct NPV, IRR and payback period

- decision that managers have to make, comes with some errors

- Affect, psychological term

Capital budgeting and ease of processing

- Conventional finance theory demonstrates that, when properly applied, NPV is optimal decision rule for capital budgeting purposes.

- Yet a number of surveys show that managers often utilise less than ideal techniques, such as the internal rate of return (IRR) and, even worse, payback period (e.g. Graham & Harvey, 2005).

Latter two may be easier to process and more salient. For this reason, they may be compelling.

- The desirability of getting your money back quickly (as reflected in payback) is obvious to even the most unsophisticated observer, though many do not realise that any payback benchmark can only be arbitrary.

- Somewhat less intuitive is IRR, but a comparison between the project’s estimated return and its cost of capital is still quite compelling.

- NPV, which is all about value creation, is perhaps a harder concept to grasp. So, it is possible that psychology is playing a role in the sometimes-weak capital budgeting technique choices that are made.

- NPV gives you the correct value

- With unconventional cash flows, deciding on the scale of the project, IRR is not the best

- does not consider the size of the project

- NPV gives the dollar return

- Assumptions we have to make to calculate what NPV is

Capital Budgeting

- managers prefer NPV

- Pick something that is simple over something optimal

- Because of all the other judements in decision making, may not be the best but has 'other benefits'

- ease of processing

Allowing Sunk Costs to Influence the Abandonment Decision

Capital budgeting and loss aversion

- Mental accounting suggests that if an account can be kept open in the hope of eventually turning things around this will often be done.

Say prior investment has not gone well.

- Proper capital budgeting practice is to periodically assess the viability of all current investments, even proceeding with their abandonment when this is a value-enhancing course of action.

- Problem with abandonment however is that it forces recognition of an ex-post mistake.

- Because of loss aversion, it may happen that managers foolishly hang on, throwing good money after bad.

- Allowing sunk cost to influence our decisions

- Don't like to put that money into 'waste'

- feel the pain of spending money and not getting anything back

- Don't only do it at the beginning of the projects

- Operations may not be on track

- may not be positive NPV throughout project's life

- Periodically evaluate whether the investment is still good

- Rational investor will end the project

- Tendency of avoiding review, means admitting our mistakes

- keep on throwing good money after bad

- Dig deeper, start losing money, should cut it off so we can do other investments

- The market seems to sense the problem.

- One study indicates that announcements of project terminations are usually well received.

- Well-known example: Lockheed and its L-1011 airplane project (which the government ended up bailing out). When the firm eventually announced abandonment, the market pushed up its stock price by 18%.

- High personal responsibility in the original investment decision increases the resistance to project abandonment. This seems to be due to the greater regret that would be induced by “admitting defeat,” as compared to the feeling of cutting losses and getting back on track that a new manager without the same level of emotional commitment to the project would feel.

- A takeover can facilitate such fresh thinking.

- Market knows psychological bias

- Any negative news, market should react negatively

- Should start seeing the price decrease

Economic impact of ending the lockheed project would be too much

- If you were the person who initiated the project (personal involvement) is high, hard for you to terminate the project

Allowing Affect to Influence Choices

Is it possible that emotion impacts capital budgeting decisions?

Since emotion plays a role in so many other realms, financial and otherwise, it would not be surprising to see it wield influence here. Direct evidence is likely to be anecdotal at best, since it is not clear how to calibrate a manager’s emotional state.

- Hard to get a direct relationship between emotions and decision making

- Did it through a survey

Academic Example

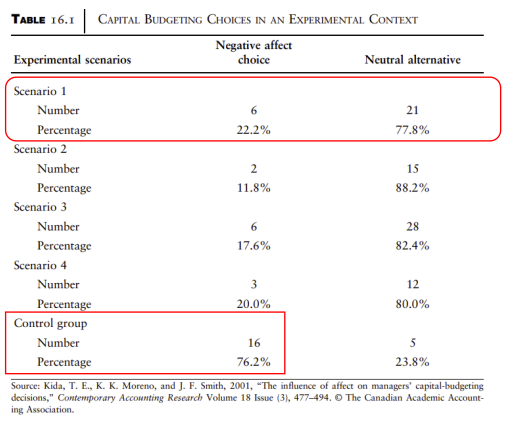

Kida, Moreno, and Smith (2001) surveyed a total of 114 managers (or individuals with similar responsibilities).

- Presented with one of five treatments where they had to make a choice between two internal investment opportunities.

- In four of the treatments the choice was between one alternative with a higher NPV and a description inducing negative affect, and a second alternative with a lower NPV but a neutral description.

For example, in scenario 1, participants were told that they were divisional managers deciding between two product investments, each of which would require working with a different sister division run by two different managers.

- Gave projects and told have to work with other managers

- who are potentially arrogant, rude, selfish, etc.

- One of the managers in question was characterised as being arrogant. Financial info of the project, if done with this individual, would generate a set of cashflows leading to a higher NPV than the other project.

- The other three negative affect scenarios were similar in their attempt to elicit a negative mood or emotion.

- The final treatment had neutral descriptions attached to both investment projects.

- While in the control group the majority of subjects chose the higher-yielding project, in all four negative treatments the opposite happened: situations associated with negative affect were avoided to the point of accepting value destruction.

- Most chose the one with lower NPV

- Should have aligned interest to increase NPV

Managerial Overconfidence

- It would be surprising if managers of corporations were markedly different from the rest of the population in terms of their overconfidence. Indeed, there is abundant evidence that managers, like investors, are egregiously overconfident.

Ben-David, Graham, and Harvey (2007) found that managers tended to predict stronger performance for their operations than actually occurred. Excessive optimism in project cost forecasts is endemic. When CFOs predict market movements, only 40% of realisations fall within 80% confidence intervals.

- Found that most of them are overconfident (predict stronger performance)

- Collaboration and confidence interval test

- The process of CEO selection and monitoring also likely rewards and encourages overconfidence.

There are two forces here. First, generous executive compensation (often only weakly related to firm performance) signals success. Greater overconfidence can result because of associated self-attribution bias. Second, the tendency for boards to be overly deferential and for investors to employ the “Wall Street rule” (sell if unhappy with management) also plays to managerial overconfidence.

- Salary compensation is not linking with performance

- Not necessarily for CEO - package is still really high

- CEO contribute salary to their own success

- Various managerial behaviours have been attributed to overconfidence.

For example, research indicates that overconfident managers tend to miss earnings targets in voluntary forecasts, and, as a result, display a greater proclivity to manage earnings.

Tendencies of overconfident managers

- Overinvestment.

- Sensitivity of investment to cashflows is higher

- More active in acquiring other companies.

- Too quick to start a new business.

- Link with how optimistic you are

Managerial Overconfidence: Overinvestment

- Ben-David, Graham, and Harvey utilised an extensive quarterly survey of CFOs over a six-year period, which, among other things, asked for 90% confidence intervals for 1-year-ahead and 10-year-ahead market returns, as well as respondents’ optimism levels for the economy and prospects for their own companies.

- The advantage of this survey is that it elicited two separate overconfidence metrics: one based on miscalibration (which they call overconfidence) and the other based on excessive optimism.

- (e.g., These researchers then acquired data on the companies for which these CFOs were employed so as to be able to correlate overconfidence metrics with firm-level behaviour.)

- It was possible to conclude that overconfident managers invest more. (In the next section, evidence is presented that the investment strategy of overconfident managers can be suboptimal.)

- overconfidence, engage in excessive trading

- not portfolio investment, but firm investment here

Ben-David, Graham, and Harvey conducted a survey

- 90% confidence interval

- miscollaborations - range

- optimism level

Overconfidence measure – Malmendier and Tate

- CEOs often receive stock and option grants as compensation.

- Overconfident managers are happy to expose themselves to own-firm-specific risk even when diversification gains are available.

- Overconfidence managers are measured as the tendency to voluntarily hold a large number of in-the-money-options.

- Optimally from the standpoint of diversification gains should be exercised, but that are still being held.

- Proxies to measure overconfidence

- Overconfident people are optimistic

- Firms under their control are undervalued

- Part of CEO's package - stock options

- exercise stock once in the money

- think the company is undervalued

- CEO option strategies to see if they are overconfident or not

- indirect proxy for confidence

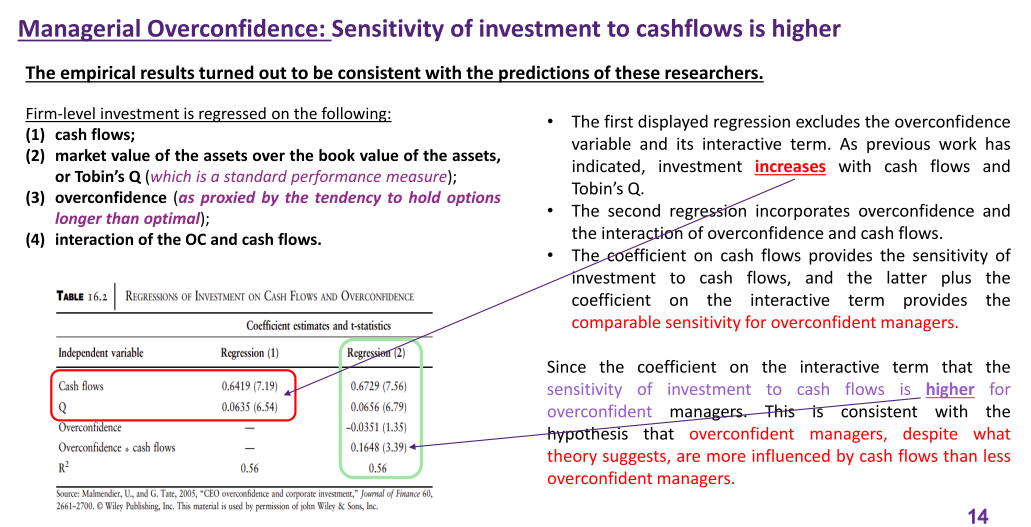

Managerial Overconfidence: Sensitivity of investment to cashflows is higher

Two traditional explanations for such investment distortions have been put forth.

- Free cash flow problem: It has been suggested that the potential misalignment of managerial and shareholder interests induces overinvestment when free cash is available, as managers are keen to empire build and provide themselves perks.

- An asymmetric information view purports that the firm’s managers, acting in the best interests of shareholders and noticing that the company’s shares are undervalued, will not issue new shares to undertake investment projects.

In both cases, investment and cash flows will be positively correlated

- relationships between investments and cash flow

- From FCF perspective, the higher the free cash, the larger investment level

- the more free cash you have, the more investments you have

Prefer to use internal cash, don't like to use new equity

- When firms want to invest, first use cash, debt and then equity

- run a regression with cash and investments

- with cash as independent variable, investment level (y)

- positive relationship, supporting argument

- With the interaction term

- How overconfidence is effecting sensitivity level

Supporting previous hypothesis - prefer to use cash, willing to forgo investments

- Once they have cash, even more investment

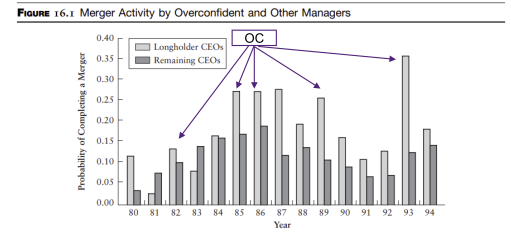

Managerial Overconfidence: Mergers and Acquisitions

- General M&A outcome: Acquiring firms don’t seem to benefit their shareholders overall. During the period 1980-2001, $220 billion was lost immediately after bid announcements.

- Survey evidence documents that overconfident managers appear to be more active on the M&A front.

- Malmendier and Tate investigate whether naturally occurring data (as opposed to survey data) support this idea, and, if so, whether this increased M&A activity leads to success for the companies.

- The impact of overconfidence on merger activity is not obvious or simple, because there are two conflicting motivations at play:

- First motivation (encourage mergers), OC managers tend to overestimate the potential synergies and their ability to handle problems that may arise. This makes them more likely to attempt M&A.

- Second motivation (discourage mergers), OC managers often believe their firms are undervalued, if a merger requires external financing, they might be reluctant to do so.

- Not really benefitting their shareholders

- have a loss in their value

- Tend to be more active in M&A activities - higher likelihood & pay a lot more money

Use option data and market for M&A deals

- can we find overconfident managers engaging in M&A (as it is good for their firms)

- First motivations

- Overconfident managers more active M&A

- Overestimate ability to handle problems in purchasing company

- Second motivation

- Believe that their firms are undervalued

- May not want to do it

-

Except for two years of their sample, all overconfident managers engage in more M&A activity.

-

Consistent with their previous study, the impact of overconfidence is greater for firms with abundant internal resources.

-

The market has a sense of the value destruction wrought by overconfident managers. While the typical market response to an announcement of a merger attempt engineered by a less overconfident manager is a drop of 12 basis points, managers subject to an inflated sense of their ability witness a (much larger) 90- basis point drop.

-

Various alternative explanations for these findings are considered. The same behavior could result from greater risk-seeking or agency (empire-building) considerations.

-

The authors, however, argue that the first is difficult to reconcile with an observed preference for cash acquisitions; and the second is not easy to tally with CEOs’ personal overinvestment.

- 12 basis points of decrease

- Finding some evidence to suggest

Managerial mistake stemming from overconfidence: Excess entry

Businesses, especially small ones, fail at an alarmingly high rate.

One possible reason for this is overconfidence.

-

Excessive optimism: overestimation of market demand.

-

Better-than-average effect: “I will beat the odds.”

-

Measuring overconfidence typically requires proxies based on track records or visibility, which many entrepreneurs lack. While industry data often suggests excessive market entry, potentially indicating overconfidence, it's challenging to compare the characteristics of entrepreneurs who enter versus those who don’t.

-

So, field tests (research conducted in a real-world setting) are problematic need an experimental setting (allows us to identify and separate key influential elements)

-

Camerer & Lovallo (1999) performed an experiment, where subjects had to choose, over multiple rounds (periods), whether or not to enter markets.

- Businesses fail when they enter into the market

- Excessive optimism

- New industry entering into the market

- Overestimating need for the product

Measurement for overconfidence

- Test overconfidence and experiment setting

- Keep factors you think are important

Excess entry: Experimental evidence

-

Experiment setting:

- An appearance fee was received by all participants. Suppose this value is $10.

- In the event of non-entry into the market, participants keep the fee.

- Entry, on the other hand, risks losing some of (or all of) this fee.

- At the same time, a positive profit is possible as a result of entry.

- An appearance fee was received by all participants. Suppose this value is $10.

-

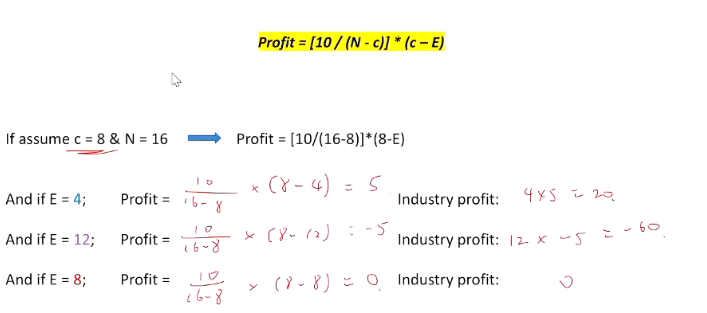

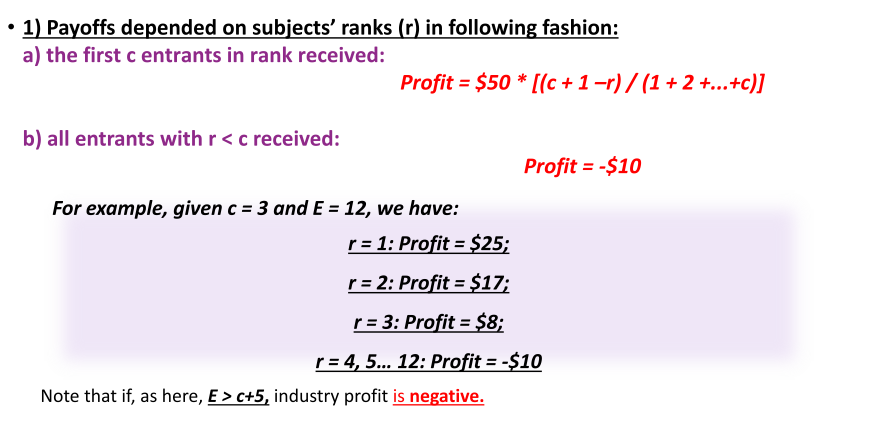

Profit function was specified as:

Where:

- N = no. of players choosing whether or not to enter a market in a given round

- c = market capacity

- E = number of actual entrants Typically, what happened was that E was close to c, implying familiar zero-profit condition of microeconomics. In other words, no excess entry

- Can lose some or all of it

- In a competitive market, economic profit should be 0, more entrants to market

- Profit -10, player's fee

- order of entering market determines profit

- Overall entrants are 2, overall industry profits are 25 + 17

- maximum profit in the industry is $50

- Can afford having another 5 people entering into the market without occurring any loss

Excess entry: Experimental evidence cont. ii.

- Subjects’ ranks depended on either a random device or skill, where skill was assessed after completion of experiment using either brain teasers or trivia quizzes (involving current events and sports).

- Subjects in some experiments (but not all) were told in advance that the experiment depended on skill.

- Subjects forecast the number of entrants in each period.

- Entry decisions were made in two rounds of 12 periods each, with ranking being skill-based in one round and random in the other.

- Market capacity was as follows: c = 2, 4, 6, and 8.

- Add ranking into components

- Ranking is random, have to decide whether you want to enter into the market

Experimental evidence – Key Issue

Are players more likely to enter when one’s profit is determined by perceived skill?

If people have true picture of their skill relative to the skill of others, there should be no impact:

- While those more skillful (and in knowledge of this) would be more likely to enter…

- Those less skillful (and in knowledge of this) would be less likely to enter…

- So, on balance these tendencies should cancel out

- People who are more skillful will enter into the market more often

Results

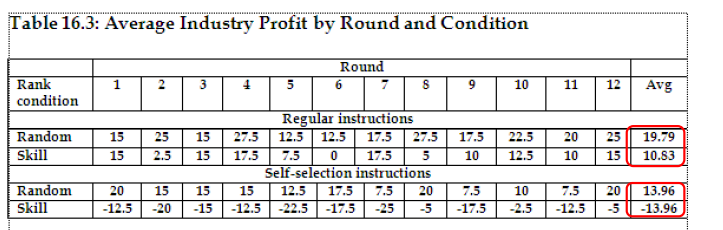

Looking at the average column (far right)

- When regular instructions were used, random vs. skilled differential profit was 8.96 (19.79 – 10.83).

- Suggesting additional entry when the payoff was to be determined by skill

- Differential was even greater when self -selection instructions were used [27.92 (13.96 – ( -13.96)].

- Consistent with reference group neglect effect

- If you know rank is randomised, profit is higher

- Maximum people enter into the market

- Ranking is based on skill, more people are joining the market

Self-selected

- told you were to join because of your skill

- A lot more people joining the market

- All other people are just as skillful

Can Managerial Overconfidence have a Positive Side?

- Aside from obvious potential impacts on investment, capital structure may also be affected. Hackbarth (2007) has formulated a model where otherwise rational managers are not only excessively optimistic about their firm’s prospects, but also overly sure about their views.

- This model suggests that managerial overconfidence is positively correlated with debt issuance, because optimism about future cash flows leads to a belief that there will be little problem in covering interest payments.

- Ironically, the natural tendency to shy away from debt because of job concerns (which is value-destroying because the benefits of debt are not exhausted) is counteracted by overconfidence.

- It has even been suggested that overconfidence among entrepreneurs, even if personally deleterious, might be socially beneficial, because entrepreneurial activity can provide valuable information to society (unlike herders, who provide no information). In this sense, it serves a valuable evolutionary purpose.

- Less risky individuals shy away from debt

- If they prefer not to use debt, wealth destroying

- Overconfident investors are more willing to take on debt

- Tendency to increase leverage

- Overconfident investors prefer short term debt

Conclusion

- Because of ease of processing, inappropriate capital budgeting techniques may be favored. Because of loss aversion, managers may throw good money after bad. And because of affect, emotion sometimes gets in the way of optimal managerial decision-making.

- There are many markers (measures) of managerial overconfidence. One is the tendency to hold on to in-the-money options too long.

- Managerial overconfidence likely leads to various forms of investment distortions or overinvestment.

- Aside from too much capital spending, overinvestment manifests itself in tendencies toward excessive M&A activity and to be too quick to undertake start-ups.

- An example of an investment distortion is allowing the availability of internal funds to dictate whether investment should go ahead.

- Overconfidence may have a bright side, though, in particular because it “corrects” excessive managerial risk aversion.

- Manager overconfidence

- tendency to hold in the money options

- overinvest, hypersensitivity to cash and investment

Add something to the bottom