Lecture 9

Emotional Foundations and Individual Investors

- Define what emotions are

- Emotion theories and evolutionary theories

- Second part, financial decision making

Introduction: Emotional Foundations

- We really do not know that much about how emotions interact with behavioural influences and other emotions to produce human actions and decisions.

- Even less is known about how the interactions of innately emotional people produce market outcomes.

- How do you measure?

- Hard to make a direct relationship to you decision making

- Affects everyday lives

- Know that we know what emotions are, where do they come from?

Examples of Emotions

- Despite the lack of a unified theory of emotion, there is some agreement on what emotions exist.

- Some mental states are clearly emotions: anger, hatred, guilt, pride, regret, elation, fear, joy, and love.

- Emotion is worth considering because it can cause one to make bad financial decisions.

- Anger, pride regret are important in decision making

- Can make both good and bad decisions

- Will be effected about how we fell in the future

- Past experience will effect emotions

Emotions about Emotions

- Agents may make decisions because they have emotions about possible future emotions.

- Specifically, fear of a negative emotion, or hope for a positive emotion, may influence behaviour.

- Fear of regret is argued to drive certain financial decisions. An investor might regret having made a bad investment.

Excessive Emotional Turbulence

- A study looked at 80-day traders.

- Tracked their daily emotional state.

- And their trading profits and losses.

- Those whose emotional reaction to gains and losses was most intense had the worst trading performance.

- Suggests need for balanced emotions.

- Intense emotion (of either side) led to the worst performance

Substance of emotion

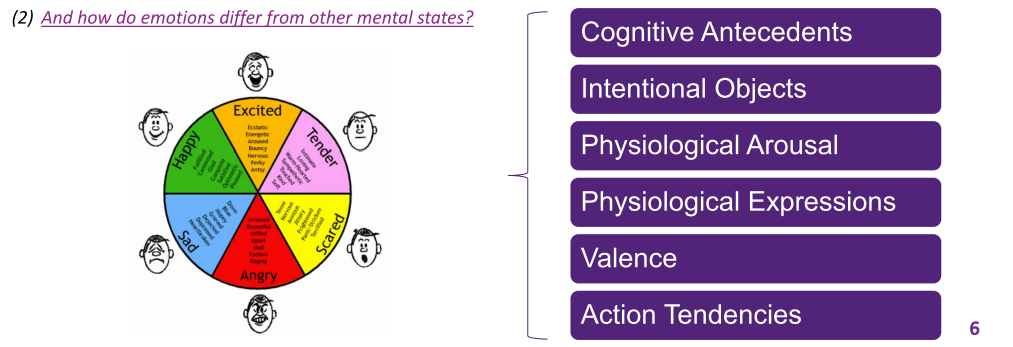

- Psychologists generally agree that such states as happiness, sadness, anger, interest, contempt, disgust, pride, fear, surprise, and regret are emotions. We can each create our own list of emotions, but we begin by asking: (1) What exactly is an emotion? (2) And how do emotions differ from other mental states?

- Can't unify the theory for emotions

- Have some basic emotions

- How do you define an emotion?

- How do you discern from other mental states?

- Can be classified only if you meet all six

1. Cognitive Antecedents

In most cases, our beliefs or thoughts about a situation lead to emotional responses. For example, When another driver runs a red light and almost causes a collision, the belief that the other driver is careless and has endangered your lift triggers the emotion of anger. Different to a bodily state (like hunger).

- Triggered by beliefs of thoughts rather than something that you feel

2. Intentional Objects

Emotions are about something specific, like a person or situation. For example, you are angry with the driver who ran the light. An emotion is about something, whereas a mood is a general feeling that does not focus on anything in particular.

- Should have a target - something specific

- 'angry' at the driver, not road, lights etc.

3. Physiological Arousal

Hormonal and nervous system changes accompany emotional responses. Your body actually goes through hormonal changes when you experience an emotion. For example, during the near collision, you might feel your blood pressure rising.

- Experiencing emotion - experience hormonal changes

- Simply in a bad or good mood, would generally not experience any hormonal changes

- After some time, won't feel that emotion anymore

- More intense, last for longer

4. Physiological Expressions

Emotions can be characterised by observable expressions that are associated with how a person functions. For example, You may express your anger at the other driver by raising your voice or shaking your fist in his direction. Some expressions are functions, but others simply result from the situation. For example, an angry person’s red face results from increased blood flow, but does not necessarily assist the person in resolving the problem.

- Linked to evolutionary theory

- Should be characterised by some observable expression

- raise voice, speak louder

- Not all expressions are functional - red face, blood pressure increasing e.g.

- Some of the emotions share similar expressions

5. Valence

Emotions can be rated on a scale with a neutral point in the centre and positive and negative feelings on the endpoints. Valence is a psychological term that is used to rate feelings of pleasure and pain or happiness and unhappiness.

- How we scale emotions

- We should be able to put it on a scale

6. Action Tendencies

Emotions are linked to action tendencies. When you experience an emotion, you often feel an urge to act a certain way. In some cases, you might even feel compelled to take action. For example, you might decide against chasing the reckless driver and telling him exactly what you think of him because you realise that others will see a seemingly out-of-control response.

- Experience some type of emotions

- Clearly identify emotions

Mood and Affect

- An emotion is about something, whereas a mood is a general feeling that does not focus on anything in particular.

- Affect is how a person experiences a feeling.

- Somebody’s affective assessment is an experience they have in response to a stimulus.

- Affect is evaluative in that a person can say whether a stimulus is good or bad, positive or negative

- Affect, just saying how you feel

- In capital budgeting, how you feel about your manager will cause you to select the project or not

- Affect is not necessarily a bad thing

- Optimise the critical stuff

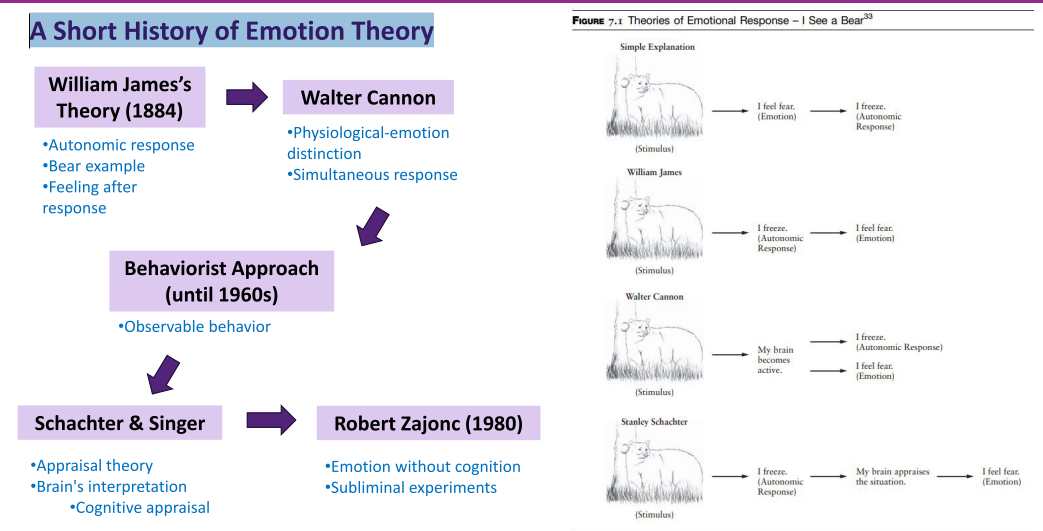

A Short History of Emotion Theory

- simple explanation on RHS

- Driver is emotions, response is to freeze

Walter Cannon

- response before feeling

- Emotion is conscious, brain will process and then realise it

Behaviourist approach

- Brain is active to stimulus

Until late 1960's

- Using emotions to link with behvaiour

- Appraisal Theory

- Body react first, brain react

Robert

- Emotions can be triggered without cognition

- People will preference without knowing why

- Positive associated with patterns you already have

The History of Emotion Theory

- Emotions influence our decisions (including financial decisions).

- Emotions aren’t just irrational responses; they include cognitive, physiological, and behavioural elements.

Cognitive Psychologists:

- Focus on mental processes: thinking, speaking, problem solving, and learning.

- Earlier theories tied emotions directly to cognitive processes.

William James’s Theory (1884):

- Emotions arise after our autonomic response.

- Example: Seeing a bear leads to an autonomic response first (e.g., freezing), followed by the feeling of fear.

Quote: “We feel sorry because we cry... not that we cry... because we are sorry.”

Walter Cannon’s Counter Argument:

- Physiological responses can occur without emotions, and similar physiological responses can be seen with different emotions.

- Our brains respond to a stimulus before their body takes action.

- Emotions and autonomic response at the same time: Seeing a bear triggers both the feeling of fear and freezing concurrently.

Behaviourist Approach (Till 1960s):

- Emotions described behaviour.

- Focused on observable behaviour over mental processes.

Stanley Schachter and Jerome Singer’s Perspective:

- Emotions are the brain's interpretation of situations.

- Both cognitive appraisal and autonomic responses are important.

- The body responds to a stimulus → The brain appraises the situation → Leading to an emotion.

Robert Zajonc’s Insight (1980):

- Emotions can occur without cognitive recognition.

- Through subliminal experiments, it’s found that people can feel emotions towards patterns they can't consciously recognise.

- Indicates that emotions can sometimes be independent of cognition.

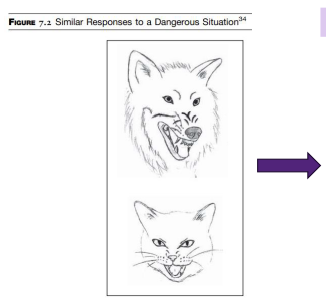

Evolutionary Theory

Traits that contribute to the survival of a species become characteristics of the species in the long run.

- Evolutionary theorists argue that our basic emotions have evolved to promote the survival of the species.

- Emotions have adaptive value because they lead to action and also communicate to others.

Example: danger leads to fear, which leads to flight and communication: “get away.”

Figure 7.2 highlights the evolutionary significance of emotions in promoting species survival.

- Evolutionary Role of Emotions: Emotions evolved to enhance species survival.

- Rapid Response: Emotions allow for quick reactions, often bypassing complex deliberation.

- Cats and Dogs Example:

- Both species display similar fearful expressions when threatened.

- Facial reactions are alike despite being different species.

- Hair stands on end in dangerous situations.

- Dual Purpose:

- Emotions drive immediate protective actions.

- They communicate clear warnings to others without verbal cues

- Less cognition, more inn

- Emotions are there to increase survival rate

- Theory are not there to describe how we feel

- How we treat and think about emotion

NOT TESTED

The Brain

Tools for mapping the brain:

- PET (positron emission tomography)

- fMRI (functional magnetic resonance imaging)

Main parts of brain:

- Brain stem structures

- Limbic system (seat of emotion)

- Forebrain (seat of cognition)

All parts of the brain continuously “communicate” with each other.

- And efficient communication (as brain injury evidence suggests) is essential

- Larger part of forebrain, planning and thinking

- logical functions controlled by left brain

- Need to have efficient communications between our brain

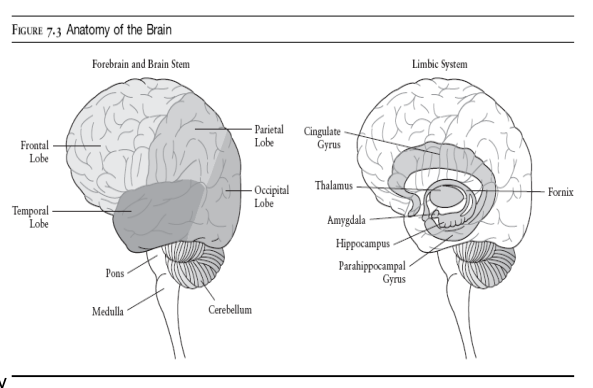

Figure 7.3 depicts the anatomy of the brain, emphasizing the brain stem structures. The medulla oversees unconscious functions like breathing, while the pons manages eye movements and sleep, and the cerebellum is crucial for movement coordination and balance.

Brain stem Structures:

Medulla:

- Connects brain to spinal cord.

- Regulates unconscious functions: breathing, blood pressure, circulation. Pons:

- Links brain stem and medulla.

- Controls eye movements, sleep, and dreaming. Cerebellum:

- Coordinates movements.

- Essential for physical balance.

Emotion and Reasoning

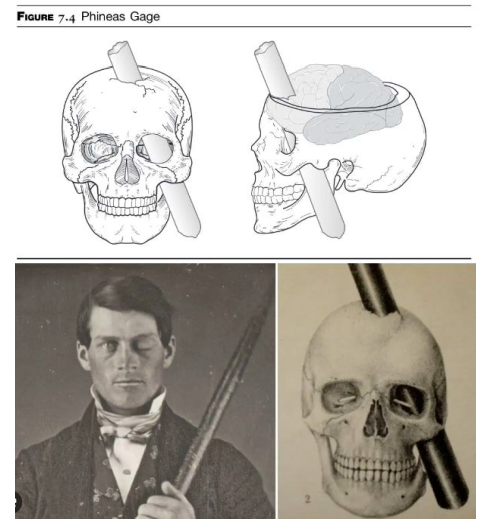

- Phineas Gage: The man who began neuroscience (1848)

- Elliot (late 1900’s)

- Both men had brain damage to their frontal lobe which caused a major change in their personality/emotional processing skills, leading the scientists to have a better idea of how different parts of the human brain function, specifically regarding personality, emotions, social interaction, and the relationship between emotions and decision making

- 1848 - Man who began neuroscience

- All in his frontal lobe

- Survived, fully conscious in hospital and regain all motor function, speech and memory

- Realised brain had regions

- Make decision purely on logic, it shoudl make it better

- Reason why - no emotion processing skills

- Things that used to give him an emotional reactions no longer did

- If your emotion is impaired, so is your decision making

Emotion Is Not All Bad

It can improve decision-making in two respects:

- Emotion pushes individuals to make some decision when making a decision is paramount.

- Often a decision has to be made

- Emotion can assist in making optimal decisions.

- Positive feelings can make it easier to access information in the brain, promote creativity, improve problem solving, enhance negotiation, and build efficient and thorough decision-making.

It really comes down to emotional balance: Emotional Intelligence.

- Helps you make optimal decision

- Easier to access information, negotiation, improve skills, problem solving

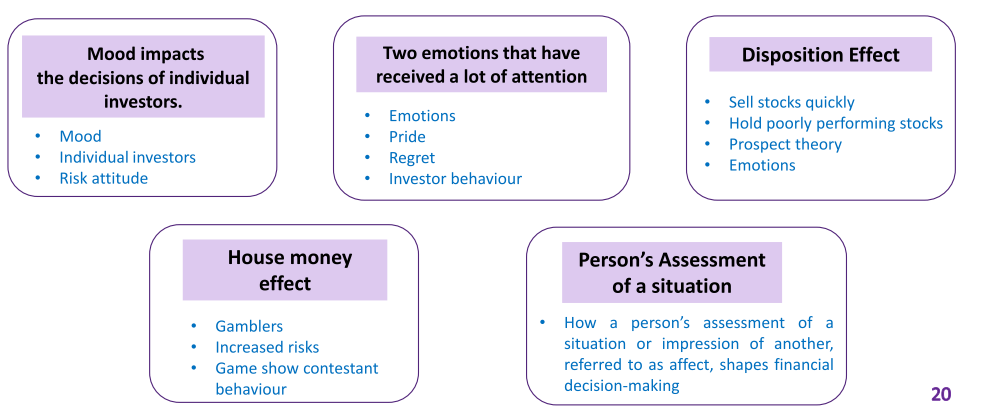

Preview of the Impact of Emotion on Financial Decision-Making

- May be behind disposition effect: the tendency to sell winners too early and hold on to losers too long.

- Fear of regret may be the driver

- May favour investment in some firms or industries but not others.

- Emotion induced by the stimulus of considering a given industry is highly correlated with the probability a participant would choose to invest in that industry

- May lead to people taking on more or less risk being affected by such non-market items such as weather and World Cup success.

- Such phenomena may even be mapped on to the level of the market.

Individual Investors and the Force of Emotion

- Regret and pride

Does Mood Move Markets?

- One study using data from 26 international stock exchanges shows good moods resulting from morning sunshine led to higher stock returns.

- Other researchers report that stock markets fall when traders’ sleep patterns are disrupted due to clock changes due to daylight savings time.

- A third study suggests that World Cup outcomes are strongly correlated with the mood of investors.

- After a loss in an elimination game, significant market declines were reported in the losing country’s market

- 26 international markets,

- daylight saving time - sleep patterns are disrupted

- market falls

- Sport event - after a loss, market also falls as well

Mood and Risk Attitude

- There is no clear or simple way to characterise the relationship between mood and risk attitude.

- When someone is in a poor mood does he take more risks or fewer?

- Answer probably depends on context and the individual’s personality

- Some research suggests happier people are more optimistic and assign higher probabilities to positive events.

- But at the same time, other decision -making research indicates that even though people may be more optimistic about their likelihood of winning a gamble when they are happy, the same people are much less willing to actually take the gamble.

- In other words, they are more risk-averse when they are happy.

- Most people tend to agree that a bad mood means more risky

- Cannot say for sure that if you are in bad mood - more risk taking

- Other research, more risk-averse when someone is happy

- Ongoing research

Pride and Regret

Regret is obviously a negative emotion.

- You might regret a bad investment decision and wish you had made a different choice

- Your negative feelings are only amplified if you have to report a loss to someone

- Pride is the flip side of regret.

- You probably would not mind too much if it just slipped out in conversation that you made a good profit on a trade

- Stronger - amplified

- Some sort of achievement

Disposition Effect

- One puzzle in finance is disposition effect: tendency to sell winners too early and hold on to losers too long. If anything, because of tax reasons, you should be quicker to take losses. This may be driven by regret: if you cash in a loser you have to face fact that you made a mistake.

Have you ever heard someone express a sentiment such as, “This stock has really shot up, so I better sell now and realise the gain?” Or, can you imagine yourself thinking, “I have lost a lot of money on this stock already, but I can’t sell it now because it has to turn around some day?” The tendency to sell winners and hold losers is called the disposition effect.

- Should sell the loser stock quicker

- Can keep residual value

- Can deduct benefits to realise the loss

- Sell it and realise the loss, have to face the fact it was a bad decision

Empirical Evidence on Disposition Effect (Odean, 1998)

- To distinguish between winners and losers a reference point is needed.

- The purchase price of a security is a natural reference point More precisely, appropriate to focus on the frequency of winner/loser sales relative to opportunities for winner/loser sales. = > Specifically, proportion of gains realised (PGR) is:

= > And proportion of losses realised is:

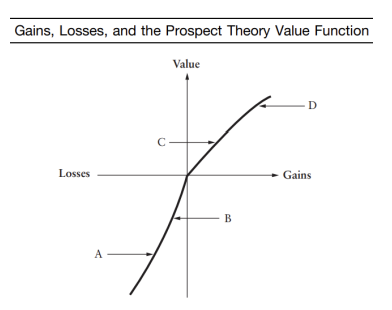

Disposition Effect, Prospect Theory, and Mental Accounting

- Another view: some explain the disposition effect by prospect theory and mental accounting.

- If a security has made money from the original date of purchase it moves up along the prospect theory value function (to points C and D)

- While, if a security has lost money, it moves down along the same function (to A and B).

- Stocks A and B have suffered losses, while C and D have experienced gains. How would these gains and losses affect your behaviour as an investor?

- After a large gain (D), you have moved to the risk-averse segment of the value function. Only major reversals of fortune are likely to move you back to the origin.

- On the other hand, after a large loss (A) you have moved to the risk-seeking segment of the value function and, again, you are unlikely to move quickly back to your reference point.

- The implication is that since you are less risk-averse for losers than winners, you are more likely to hold on to them.

- More risk averse, don't want to take the risk in gambling

- Less risk averse in a positive domain

- The farther you are away from the risk-seeking domain, the less likely it is that a particular gamble will be partly influenced by risk-seeking.

- So, risk aversion is higher for gambles beginning

at

- D vs. C, or C vs. B, or B vs. A.

- Demand will be higher/lower for securities that have suffered capital losses/gains.

Experimental Evidence (Summers and Duxbury, 2007)

- Experimental evidence favours emotions over prospect theory in explaining disposition effect.

- Experimental design was predicated on whether or not individuals have chosen their investments.

- When no choice, you will experience disappointment

- When with choice, you will experience regret (which is stronger than disappointment)

- So disposition effect should be stronger with choice – which turned out to be true.

- value of a share decreases, demand is higher

- When the price is increasing, we think it is the high point, wait until the price increases

- Low point, get into the market

House Money Effect

- Successful investment can cause elation (great happiness).

And bad investments can cause distress.

It is argued that result is that prior gains and losses can cause changes in risk taking.

e.g., Say you are at a casino. You do really well at blackjack, and you are up $200.

- you play more or less aggressively?

- With recent gains, increase risk taking, play more aggresively

Conflicting Effects

- Mood maintenance: “I am feeling good. I should walk away and enjoy this feeling.”

- House money: “This is the house’s money. Let’s have some fun and really make some money.” Likely many people are influenced by both impulses. Though evidence is that house money dominates. Or we can think in terms of prospect theory and mental accounting again.

- Walk away and stop playing

- both rationales effecting your decision

House Money

- Evidence of a House Money Effect on a Large Scale:

- "Deal or No Deal?" game show examined to understand high-stakes decisions.

- Contestants make decisions based on previously revealed suitcase values.

- Opening low-value suitcases leads to more risk (House Money Effect).

- Opening high-value ones pushes contestants to riskier decisions to break even.

- Significant changes in expected wealth regardless of the sign lead to more risk-taking.

- Based on deal or no deal

- treat it as a win, tend to be more risky

- High value suitcase, still risk taking, break-even

- Regardless of win or lose, become more risk taking

- Prospect Theory and Sequential Decisions:

- Some behaviours challenge the standard prospect theory, especially in sequential gambles.

- After significant gains, individuals may show decreased risk aversion (House Money Effect) [or increased risk taking].

- Emotions and past experiences influence sequential decision-making.

- Financial theories are now integrating these behavioural aspects, suggesting stock market volatility after significant price changes. (see Barberis, Huang and Santo, 2001 QJE)

- Further research is essential to better understand market dynamics, especially concerning individual behaviours.

- Prospect theory designed for one off game

- House money - sequential games. Prior gains or losses to alter behaviour

- Emotions or past experiences can affect decision later

- don't have a clear picutre of evidence suggesting how this works

- More decisions, more complicated

- next minute, decisions for different reasons

- need more research

House Money (Winning) vs. Value Function of Prospect Theory (Segregation vs. Integration)

- House money effect suggests reduce risk aversion after their initial gain.

- However, the prospect theory does not make such prediction.

- Problem with prospect theory is that it was set up to deal with one-shot gamble – but what if there have been prior gains or losses?

- Do we go back to zero (segregation), or move along curve (integration)?

- Integration: After gains you are less likely to face loss-

aversion kink

- This is on assumption that you do not segregate gambles by moving back to the 0 reference point

- very unlikely only play one game

- House money effect related to prior games

- Prospect theory, integration perspective

- It is because the more games you have, integrate together, move along the line

- concave

- When we have sequential decisions, you become less risk averse

- Move away from the loss-averse 'kink'

- Move away from loss aversion, will become more risk taking

What About After Losses?

- Symmetry might suggest you should become more risk-averse after losses.

- This is the snake-bit effect: “I have lost a lot from risky investments so now I am moving towards a much less risky portfolio”

- However, some evidence (e.g., “Deal or No Deal” research) suggests greater risk-taking after losses. This shows support for the break-even theory. People try to get even by taking a risky gamble to recoup their initial losses.

- Consistent with prospect theory and still being distant from loss aversion kink

- When we lose, should become more risk averse

- Don't want to experience that again

- From empirical evidence, more risk taking after a loss

- More dominant from break-even theory

- Moving away from loss aversion

Affect and Financial Decision-Making

- Affect in Decision-Making: Emotions and immediate sentiments, termed as "affect," play a vital role in decision-making processes. This is observed in scenarios where personal feelings towards stimuli (e.g., a negotiator) might influence outcomes.

- Affective Reactions: Such reactions, based on positive or negative feelings from experiences, guide attractions or aversions to stimuli, providing an efficient decision-making shortcut.

- Future Research: Affective reactions can sometimes override cognitive evaluations in financial decisions, yet a complete understanding of their interplay and dominance remains a topic of ongoing research.

- Positive affect is a “warm and fuzzy feeling.”

- One study looked at the relationship between the image of a market and the behaviour of investors.

- The better an industry makes you feel, the more likely you are to put your money into it!

- Still need a lot more design and data

- If you have a positive affect about an industry, you tend to put a lot more money in it

- Other explanation, other things to try and say you would invest in it

- Influence but how you feel

Conclusion

- Emotions, like anger and happiness, are crucial for cognition and decision-making.

- Distinguished by features like physiological arousal and intentional objects.

- Evolutionary significance: they enhance communication across species.

- Human brain, especially the cerebrum, central to advanced emotional responses.

- Emotions are vital for prompt and quality decision-making.

- Case of Phineas Gage highlights the role of emotions in decisions.

- Balance of emotional and cognitive intelligence is key to success.

- Emotions and cognition are deeply intertwined.

- We can regulate the intensity of our emotions.