Tutorial 9 - Topic 8 Behavioural Explanations for Anomalies

1*. Differentiate the following terms/concepts:

a. Momentum and reversal

- Momentum is positive correlation in returns, exist empirically over the medium term

- Reversal is a negative correlation in returns, the latter over the long term

- Should be no overvalued or undervalued stocks

b. Mean-reversion and continuation scenarios in the Barberis-Shleifer-Vishny (BSV) model

- Investors expect positive/negative surprised to be followed by negative/positive surprises

- Under continuation, investors expect a positive/negative surprises to be followed by positive/negative surprises

c. Size factor and book-to-market factor

- In Fama french thee factor model, size and book-to-market are risk factors

- Two risk factors still being incorporated into the model

- Come up with more factors that could influence stock returns

d. Risk-based and behavioural explanations (for anomalies)

- A risk-based (rational) explanation would argue that value stocks do better on average because they are riskier, as in the Fama-French model.

- On the other hand, a behavioural model would say that anomalies exist because of investor error and limits to arbitrage. The models in the chapter amount to behavioural explanations of anomalies.

- Arbitrage exists because of the limits to arbitrage

2*. In the context of the BSV model, explain intuitively (nontechnically) why two consecutive earnings changes in the same direction make investors less likely to think that they are in regime 1 (mean-reversion) vs. the case of two earnings changes in alternate directions

Investors, however, being coarsely calibrated, believe that stocks switch between two regimes.

- Under regime 1, it is believed that earnings mean-revert. This means that a positive/negative earnings change is likely to be followed by a negative/positive earnings change in the next period. More formally, given a positive/negative earnings change, there is a low probability (pr L ) of another positive/negative earnings change in the next period.

- Under regime 2, given a positive/negative earnings change, there is a high probability (pr H ) of another positive/negative earnings change in the next period. In other words, it is believed that there is a continuation in earnings. Note that pr H > pr L .

Two consecutive earnings changes in the same direction make it appear that Regime 2 is in effect (and Regime 1 is not in effect) since this is what we would expect in Regime 2.

5*. Momentum is the anomaly that gives those subscribing to efficient markets the most trouble. Explain.

- Fama French three-factor model has a role for size and value but not momentum

- Some research related momentum to business cycle and the state of the market

- non-diversifiable macroeconomic instruments account for a large portion of momentum profits

- time-varying CAPM with beta uncertainty can contribute to an explanation of momentum

6*. A series of Questions related to Factor Zoos:

(a) What is Factor Zoo?

- The “Factor Zoo” is a term used in the context of asset pricing to describe the proliferation of factors that have been identified as potentially explaining asset returns.

- As research in this field has evolved, numerous factors have been proposed, tested, and debated, leading to a veritable “zoo” of factors.

(b) What is the development of academic research related to the “Factor Zoo”?

- landscape of asset pricing factors is complex, hundred of proposed factors

- leading researching have raised concerns about legitimacy

- Use data minings and find and explain anomalies

CFA question

- home bias may influence investor behaviour

- Rather than doing thorough analysis, they might anchor to other analysis

- Moderately risk averse, risk averse bias

- Use the tax return to do travel, etc.

- Bad situations, mental accounting bias

- For the investor, mental accounting bias

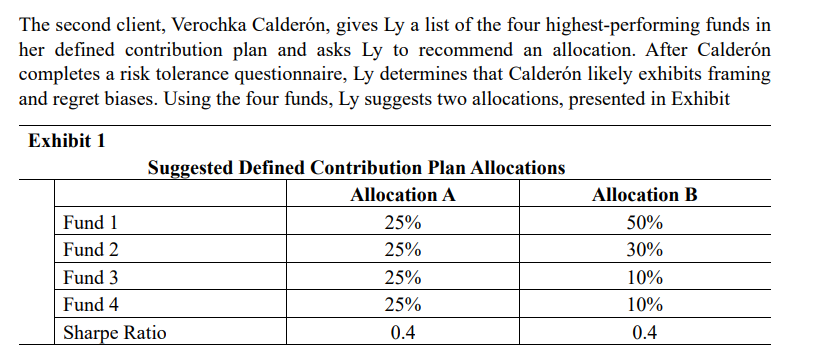

Portfolio 2 has the same returns and sharpe ratios

Mental account bias

- most likely select portfolio 2

- Suggests that he wants to compartmentalize his portfolio into discrete layers of low-risk assets verses risky assets without regards to the correlations among the assets

- some clients will view allocation 1 as the more profitable 1

- Prefer allocation 1, anything happens to

- Result of framing bias, likely to choose an allocation based on a 1/n naive diversification strategy

- As a result of regret bias, likely to coose a conditional 1/n strategy to minimise any potential future regret from one of her funds outperforming another

- Would most likely select AllocationA

- Ly believe that Calderon exhibits framing and regret biases