Tutorial 2

1.1 Lottery and Insurance

- A lottery is a prospect with a low probability of a high payoff. Many people buy lottery tickets, even with negative expected values. These same people buy insurance to protect themselves from risk.

- Normally, insurance is a hedge against a low-probability large loss. These choices are inconsistent with traditional expected utility framework but can be explained by prospect theory.

1.b Segregation and integration

- Integration occurs when positions are lumped together

- Segregation occurs when situations are viewed one at a time

- reference point is the starting point from which people make decisions about gains and losses.

- The value of an object is determined by the change in value between an object under consideration and that reference point

- valuations of prospects depends on gains/losses relative to a reference point

1.c Risk aversion and loss aversion

- A person who is risk averse prefers the expected value of a prospect to the prospect itself,

- For a person who is loss averse, losses loom larger than gains.

1.d Weighting function and event probability

- Event probability is simply the subjective view on how likely the event is

- The weighting function is associated with the probability of an outcome, but is not strictly the same as the probability as in expected utility theory

Key Aspects:

- People sometimes exhibit risk aversion and sometimes risk seeking, depending on the nature of the prospect

- Valuations of prospects depend on gains and losses relative to a reference point

- People are averse to losses because losses loom larger tha gains

2*. Give an example of a decision where loss aversion could lead an investor to make an irrational choice. How could this situation be mitigated?

- An investor might be hesitant to sell an underperforming stock due to loss aversion - the fear of realising a loss is psychologically impactful

- Holding onto the stock could lead to greater losses

- This could be mitigated through setting predetermined selling points (stop-loss orders) to limit potential losses and remove emotional decision-making

3*. Consider an individual who is risk averse. How might this person behave differently in investment scenarios compared to a risk-seeking individual?

A risk-averse individual would prefer investments with lower but more certain returns, such as bonds or index funds. On the other hand, a risk-seeking individual might invest more heavily in high-risk, high-reward assets, like individual stocks or cryptocurrencies.

4. In your own words, explain how loss aversion and risk aversion might influence a company's financial decision-making.

Both loss aversion and risk aversion can lead a company to conservative financial decision-making.

- Loss aversion might prevent a company from discontinuing a failing product line or from investing in a promising but uncertain venture.

- Risk aversion might lead a company to retain excess cash reserves or avoid taking on debt, even when those resources could be invested profitably.

5. Can a person be both risk-averse and loss-averse? Give a practical example of how these two characteristics might interact.

Yes, a person can be both risk-averse and loss-averse. For example, an investor might choose a low-risk investment portfolio to avoid the potential for large losses (risk aversion) but might also hold onto an underperforming stock to avoid realizing a loss (loss aversion).

6*. How might an understanding of loss aversion and risk aversion influence the strategies of a financial advisor when advising clients?

- A financial advisor, understanding these principles might recommend diversified portfolios to risk-averse clients to spread their risk.

- and might use methods like dollar-cost averaging to mitigate the emotional impact of market fluctuations and loss aversion

- The advisor might also prepare clients for the inevitability of market downturns to help them avoid panic selling due to loss aversion

- Dollar cost averaging: by investing in smaller set amounts over time, will buy both when prices are low and high. Smoothes out average purchase price. Can be especially powerful in recessions and bear markets.

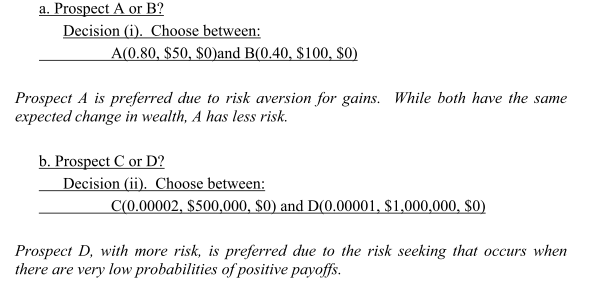

7*. According to prospect theory, which is preferred?

c. Are these choices consistent with expected utility theory? Why or why not? Violation of EU theory because preferences are inconsistent. The same sort of Allais paradox proof from Chapter 1 can be used. It is also necessary to make the assumption of preference homogeneity, which means that if D is preferred to C, it will also be true that D* is preferred to C* where these are:

8*. Consider a person with the following value function under prospect theory:

when w > 0

when w < 0

a. Is this individual loss-averse? Explain.

This person is loss averse. Losses are felt twice as much as gains of equal magnitude.

b. Assume that this individual weights values by probabilities, instead of using a prospect theory weighting function. Which of the following prospects would be preferred?

Q10.

- Payment decoupling is encouraged with fixe prix

- You only face the loss of money once rather than multiple times

Agency Theory

Q11.

Shareholders can do the following:

- Ensure that employees are paid with company stock and/or stock options

- Ensure that underperforming managers are fired

- Write several contracts that ensure that the interest of the managers and shareholders are closely aligned

- Set up a monitoring mechanism (such as boards) to ensure that managers work in the best interest of the shareholders

- Performance based pay: Tie a significant portion of executive compensation to the company's growth, profitability, or total shreholder return (TSR) Transparency clause: Ensure transparency in financial reporting

Q12

- separation between management and ownership

- issues that arise from the separation

- One the one hand, managers do not usually have direct ownership, manage and control the firm

- On the other hand, the shareholder, who are the owners, are not involved in the management of the firm

- This creates a clear conflict of interest between the investors and shareholder of the firm

Q13

- Main roles of the board is to monitor the management to reduce agency costs and to ensure that the managers work in the best interest of the shareholders

- Board also provides guidance and support to the CEO and the management of the firm

- Role in setting the main vision and strategy of the company. REsponsible for approving and keeping track of the firm's strategy as well as annual budgets and investment programs established in the action plan prepared by the executive officers

Q16

Two counterarguments:

- there is no reason to expect a simple relation between ownership and performance. Many dimensions to corporate governance system

- Some studies have shown a non-linear relationship between firm valuation and ownership, specififcaly that increasing ownership is good at first, but that in a certain range, managers can use their ownership level to partially block efforts to constrain them

- increasing ownership can reduce performance

Q17

- Ignore the shareholder, which will result in either the shareholder going away or launching a proxy fight

- Negotiate with the dissident shareholder to come to a solution on which